What a Warsh Fed means for markets

When Kevin Warsh takes over the Federal Reserve, the shift will go well beyond personalities. The new Fed chair will likely redefine how policy is delivered and communicated and, crucially, how markets are expected to respond.

At its core, a Warsh-led Fed would probably look more disciplined, less reactive and more tolerant of market discomfort.

That matters, because for years, investors have operated under a framework where the central bank ultimately leans against financial stress. Under Warsh, that assumption could start to fade.

A Fed more focused on credibility rather than cushioning

The first defining feature of a Warsh Fed would likely be a stronger emphasis on policy credibility over short-term stabilisation.

This implies:

- Less urgency to cut rates at the first sign of growth weakness

- Greater willingness to keep policy restrictive for longer

- A clearer prioritisation of inflation risks, even late in the cycle

In practical terms, the reaction function shifts. The bar for easing rises, and the tolerance for tighter financial conditions increases.

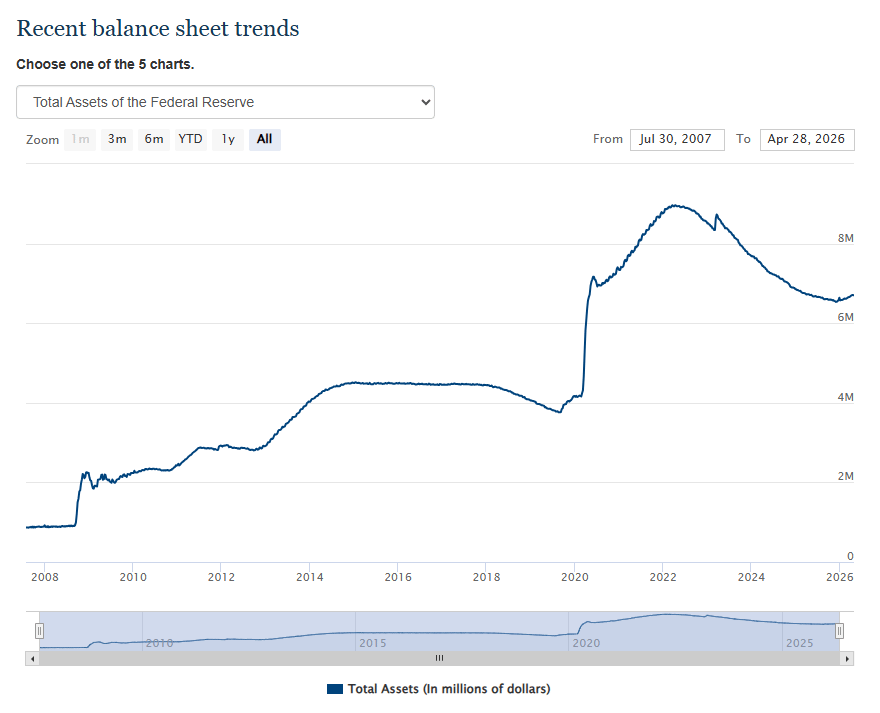

The balance sheet moves to centre stage

One area where a Warsh Fed could look materially different is the treatment of the balance sheet.

In recent years, the Fed’s asset holdings have often been seen as a secondary tool, clearly outweighed by interest-rate adjustments and operating quietly in the background through quantitative tightening or reinvestment policies. Under Warsh, that hierarchy could change.

The balance sheet could become a more active and visible instrument of policy. That means:

- A stronger commitment to reducing excess liquidity over time

- Less reliance on rapid balance sheet expansion during market stress

- A clearer separation between monetary policy and market stabilisation

From a market perspective, this approach is key. Liquidity has been one of the dominant drivers of asset prices over the past decade. A Fed that is more deliberate, and potentially more restrictive, in managing its balance sheet introduces a structural headwind for risk assets and reinforces tighter financial conditions even without aggressive rate hikes. This would be bad news for equities, crypto and currencies highly reactive to changes in money supply.

Communication: Fewer reassurances, more uncertainty

A second key shift would likely come through communication.

A Warsh Fed may:

- Offer less forward guidance

- Avoid signalling a “policy path” too explicitly

- Push back against the idea of a predictable easing cycle

That would remove one of the anchors markets have relied on in recent years.

The result is not necessarily tighter policy at all times but less visibility around it. And that alone can tighten financial conditions and also lead to more surprises.

The end of the “Fed put”?

Perhaps the most important implication is the potential erosion of the so-called “Fed put”. That does not mean indifference to markets, but it does suggest a Fed that is less inclined to step in quickly to stabilise them.

Under a Warsh framework:

- Equity market drawdowns may not trigger immediate policy support

- Financial volatility could be seen as part of the transmission mechanism

- Asset prices would carry more two-way risk

What Warsh has actually said

Warsh’s message over the years has been remarkably consistent, and markets would do well to pay attention.

In essence, his thinking can be distilled into a few core ideas:

- Central banks risk overstaying their welcome when policy remains too loose for too long.

- Expanding the balance sheet is not neutral; it shapes markets and distorts price signals.

- Credibility is hard-earned and easily lost, especially once inflation takes hold.

- Monetary policy should not be the first line of defence for every market disruption.

Taken together, this points to a framework that is less activist, more restrained, and far more conscious of long-term side effects.

FX implications: a structurally firmer Dollar

For FX, the consequences are relatively clear. A more disciplined and less reactive Fed tends to:

- Support higher real yields over time

- Reinforce the US Dollar’s policy premium

- Reduce the probability of aggressive easing cycles

In that environment, the US Dollar is less about short-term rate differentials and more about institutional credibility and policy asymmetry. That is typically a supportive backdrop for the Greenback, particularly against low-yielding currencies and those sensitive to global liquidity.

To sum up

A Warsh-led Fed would not necessarily mean permanently tighter policy. But it would likely mean a central bank that is harder to second-guess, less willing to reassure markets, and more focused on long-term credibility than short-term stability.

And crucially, one that treats the balance sheet as a core policy lever, not a side tool.

For markets that are used to abundant liquidity and clear guidance, this represents a completely different regime.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.