US Dollar Weekly Forecast: Fed’s Independence concerns weigh on outlook

- The US Dollar Index saw its recovery curtailed this week.

- President Trump nominates Stephen Miran for FOMC Governor.

- Politics threatens to undermine the Fed’s independence.

The week that was

The US Dollar surrendered last week’s hard-won advances, with the US Dollar Index (DXY) sliding back toward the 98.00 neighbourhood after failing to hold ground above the psychological 100.00 mark in the past few days.

On the monthly chart, August has begun on the back foot, erasing a chunk of July’s rebound and nudging the year’s broader downtrend back into gear. So far, the index has found solid support near 96.40 — the multi-year low it touched on July 1.

Big picture drivers are once again steering the market: trade tensions have re-emerged, and fresh questions about the Fed’s independence are colouring sentiment and price action alike.

Interestingly, while US Treasury yields have been grinding higher, the Greenback itself has moved the other way, underscoring the market’s uneasy mood.

Let's return to the realm of politics!

President Donald Trump has revived concerns about a politicised Federal Reserve (Fed).

First came his abrupt firing of the Bureau of Labor Statistics (BLS) commissioner after he alleged — without evidence — that jobs data were being “rigged”, a charge that followed hefty downward revisions to payroll figures.

Then he resumed his public broadsides against Fed Chair Jerome Powell and tapped Stephen Miran, now head of the Council of Economic Advisors, to fill the seat vacated by FOMC Governor Adriana Kugler.

Adding to the intrigue, FOMC Governor Christopher Waller — widely viewed as a policy dove—has reportedly vaulted near the top of Trump’s shortlist to succeed Powell. Taken together, the moves point toward a Fed that could be both more politically-driven and more inclined to slash rates, echoing Trump’s long-standing demand for “much lower” interest rates.

Shrinking hopes of trade agreements ahead of August 12

Darkening the mood, Trump’s “reciprocal” tariffs took effect on August 7, slapping imports from 69 trading partners with levies of 10%–41% almost overnight and hinting at even harsher penalties for Russia if the war in Ukraine drags on.

The deadline of August 12 looms just ahead: unless the President renews the fragile truce with Beijing, duties will snap back into triple-digit territory, risking a fresh, full-blown trade war.

Tensions over tariffs are flaring on the trans-Atlantic front as well. Europe has greeted the new US-EU trade pact with a cool reception: Paris has flatly condemned the deal, while German Chancellor Friedrich Merz warns it will hurt exporters and sap growth. Billed as a breakthrough, the accord has done little to lift market spirits, which see scant near-term relief for the Eurozone.

When considered collectively, the events of this week highlight a growing divide between Washington's trade agenda and its major allies, escalating the risks on multiple fronts, both economically and diplomatically.

Tariffs: An expensive fix for a stubborn trade gap?

While tariffs continue to be popular in Washington, their political appeal may come with a steep long-term cost. Currently, consumers have managed to avoid significant price increases, but if these levies persist, they will gradually impact daily life, increasing the cost of essentials, tightening household budgets, and slowing overall growth. Should inflation flare up again, that sluggish backdrop would leave the Fed in an awkward bind.

There are indications that policymakers could tolerate a weaker US Dollar, with the expectation that it would boost exports and reduce the trade deficit. Reshoring manufacturing is a worthy goal, but rebuilding America’s industrial base will demand time, hefty investment and a smarter tariff framework.

While duties may play a role, they are not a panacea for the underlying imbalances in global trade.

Fed mandate vs. data

The Fed kept rates on hold on Wednesday, July 30, choosing caution — and revealing little about when, or even whether, cuts might arrive. The fed funds rate target remains at 4.25%–4.50% for a fifth consecutive meeting as officials steer between stubborn inflation and a cooling economy.

“Unemployment is still low and labour market conditions are solid, but inflation remains elevated,” the post-meeting statement noted.

The decision was not unanimous. Vice-Chair for Supervision Michelle Bowman and Governor Christopher Waller — both Trump appointees — voted for an immediate 25 bps cut, arguing policy is already too restrictive.

At his press conference, Chair Jerome Powell called the labour market “effectively at full employment,” satisfying one half of the Fed’s dual mandate. Inflation, however, is still above target and clouded by tariff effects, leaving the Fed short of its price-stability goal. Given that mix, Powell said keeping policy “modestly restrictive” remains the prudent course.

This week, Fed officials maintained a cautiously dovish tone, yet they presented the debate in slightly different ways.

St. Louis Fed president Alberto Musalem acknowledged on Friday that policymakers now have to juggle two‐sided risks: inflation has yet to be fully tamed, yet cracks are beginning to show in the labour market. He argued that the committee must first determine the severity of each threat before concluding that rate cuts are necessary.

Speaking to a business audience in Florida on Thursday, Atlanta Fed chief Raphael Bostic said the June payrolls report had pushed job market risks higher than before. Even so, he still envisages just one 25-basis-point reduction this year. He stressed that the Fed will receive “a lot of data” on prices and employment before the next meeting, and that those numbers will shape his final call.

Addressing the outlook on Wednesday, San Francisco Fed President Mary Daly reported that firms have not halted capital spending despite fresh policy uncertainty over tariffs, but they are no longer moving forward at full speed. In her view, businesses are waiting for clearer policy signals before committing to larger projects.

Rounding out the chorus, Minneapolis Fed President Neel Kashkari told CNBC that the economy is losing momentum and that beginning to ease policy “in the near term” could be prudent. Two quarter-point cuts by year-end, he said, “seems reasonable.”

Taken together, the remarks suggest the FOMC is inching toward an easing bias, yet officials remain divided over how quickly — and how far — to move as they weigh stubborn inflation against an increasingly fragile job market and hesitant business investment.

What’s next for the US Dollar?

Next week’s calendar is led by the Inflation Rate report, giving markets their latest read on the Consumer Price Index (CPI). Producer Prices prints and the weekly Initial Jobless Claims figures will follow close behind, while a steady stream of Fed commentary should keep investors alert throughout the week.

What about techs?

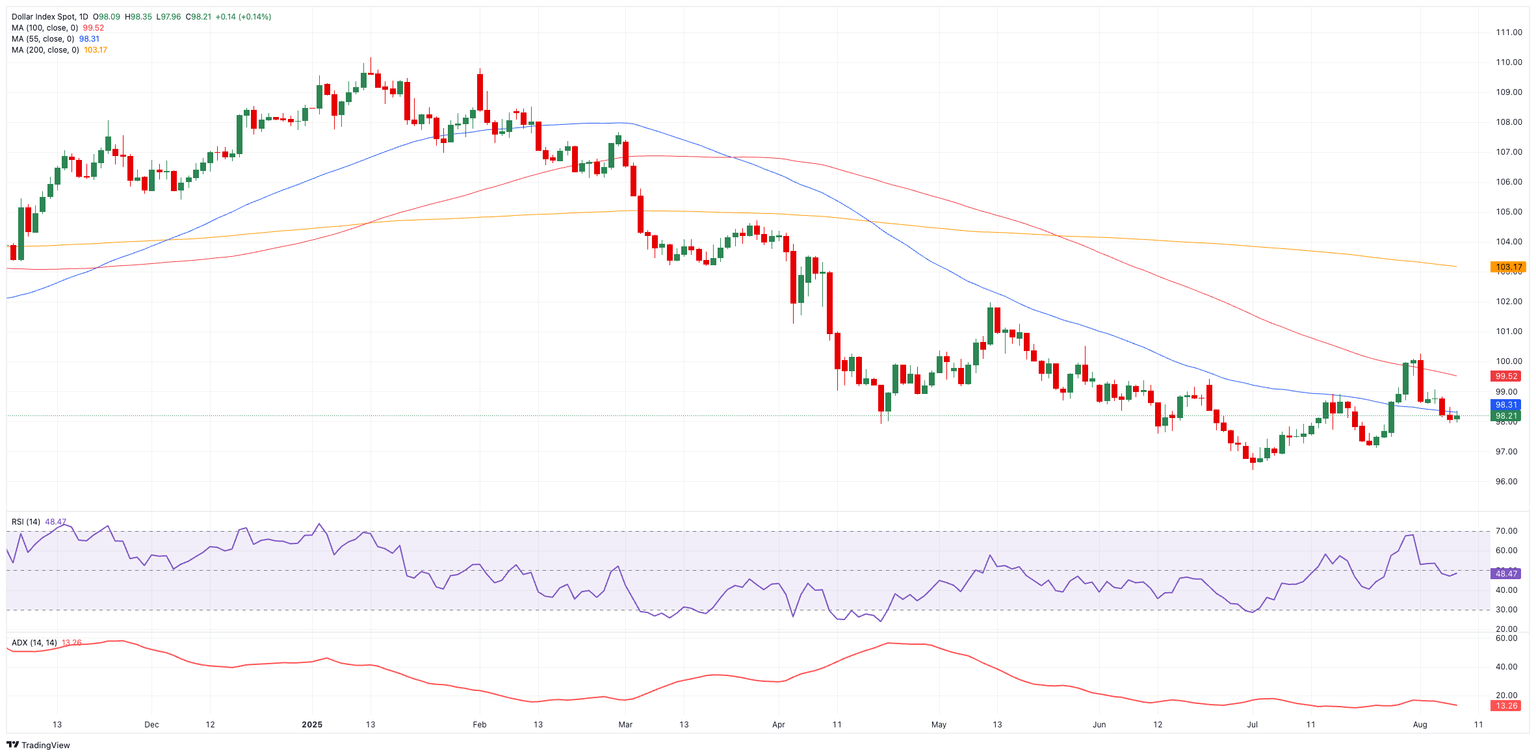

Should DXY slip beneath its multi-year trough at 96.37 (July 1), the next safety nets line up at 95.13 (February 4) and 94.62 (January 14).

Conversely, the initial barrier resides at the August ceiling of 100.25 (August 1). A clean break there could invite a run toward 100.54 (May 29) and, beyond that, the May summit at 101.97 (May 12).

For the time being, the index stays below the 200-day and 200-week SMAs, trading at 103.15 and 103.11, respectively, favouring further weakness.

The momentum is also diminishing: the Relative Strength Index (RSI) has dropped to approximately 48, and the Average Directional Index (ADX) is hovering around 13, suggesting that the recent upward trend is waning.

US Dollar Index daily chart

All in all

The US Dollar’s recent stumbles trace back to Washington as much as to Wall Street. Traders say President Trump’s seesaw tariff threats, his public skirmishes with the Fed Chair Jerome Powell, and an ever-swelling national debt have all pushed up the “term premium” investors demand to hold long-dated Treasuries. In plain English: keeping money in US assets feels riskier, so the compensation has to be higher.

Even on days when the Greenback exhibits brief moments of strength, these gains are rarely sustained. Trade policy still changes on a tweet, and Trump’s splashy “Big and Beautiful Bill” has only widened worries about fiscal discipline. With little visibility on future deficits, markets hesitate to price in a sustained dollar rebound.

For its part, the Fed remains cautious. Policymakers insist any move hinges on the data, so the next rate decision could just as easily give the currency a quick boost as knock it lower again. That data dependency keeps traders on edge, but it also means the dollar lacks a clear upward catalyst.

For now, most strategists see more downside than upside. An enduring trade gap, political incentives for a weaker currency, and lingering doubts over the Fed’s independence all point toward a softer DXY in the months ahead.

A Reuters poll this week put it bluntly: without a decisive turn in policy or the economy, the dollar is likely to drift lower as 2025 unfolds.

US Dollar FAQs

The US Dollar (USD) is the official currency of the United States of America, and the ‘de facto’ currency of a significant number of other countries where it is found in circulation alongside local notes. It is the most heavily traded currency in the world, accounting for over 88% of all global foreign exchange turnover, or an average of $6.6 trillion in transactions per day, according to data from 2022. Following the second world war, the USD took over from the British Pound as the world’s reserve currency. For most of its history, the US Dollar was backed by Gold, until the Bretton Woods Agreement in 1971 when the Gold Standard went away.

The most important single factor impacting on the value of the US Dollar is monetary policy, which is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability (control inflation) and foster full employment. Its primary tool to achieve these two goals is by adjusting interest rates. When prices are rising too quickly and inflation is above the Fed’s 2% target, the Fed will raise rates, which helps the USD value. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates, which weighs on the Greenback.

In extreme situations, the Federal Reserve can also print more Dollars and enact quantitative easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system. It is a non-standard policy measure used when credit has dried up because banks will not lend to each other (out of the fear of counterparty default). It is a last resort when simply lowering interest rates is unlikely to achieve the necessary result. It was the Fed’s weapon of choice to combat the credit crunch that occurred during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy US government bonds predominantly from financial institutions. QE usually leads to a weaker US Dollar.

Quantitative tightening (QT) is the reverse process whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing in new purchases. It is usually positive for the US Dollar.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.