US Dollar Weekly Forecast: Warsh's impossible job

- The US Dollar ended the week with marginal losses.

- Investors continue to look into the details of the potential US-Iran deal.

- Fed officials maintained their hawkish tilt in their latest comments.

The week that was

Another apathetic week saw the US Dollar (USD) retreat modestly, although not by much. Geopolitics remained firmly at the centre of market attention, particularly toward the end of the week after reports emerged that the US and Iran had reportedly reached an agreement aimed at extending the current 60-day ceasefire.

The deal, which still requires formal ratification, would reportedly pave the way for the reopening of the Strait of Hormuz and the gradual normalisation of global shipping flows. For markets, that represents a potentially important shift after weeks of concerns over energy supplies, trade disruptions and the inflationary consequences of elevated Oil prices.

Against that backdrop, the US Dollar Index (DXY) remained anchored near the upper end of its recent range around the 99.00 region, while US Treasury yields drifted lower across most maturities as investors reassessed geopolitical risks and pared back some of the more aggressive tightening expectations that had emerged earlier in the month.

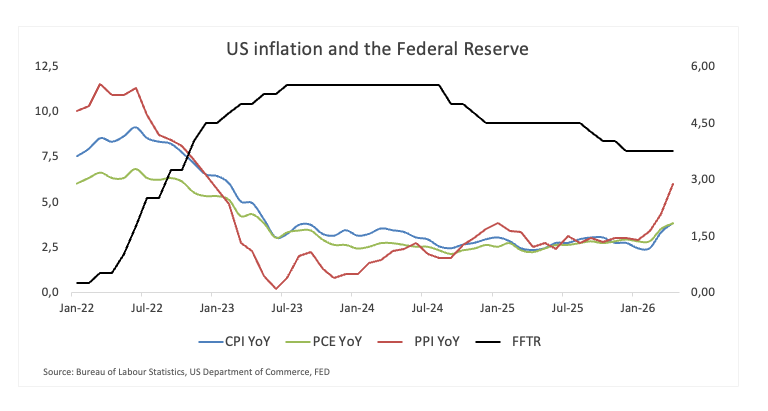

On the data front, inflation remained the dominant theme. The Personal Consumption Expenditures (PCE) Price Index, the Federal Reserve's preferred inflation gauge, surged to 3.8% YoY in April, heightening fears that the march towards the Fed’s 2% target remains frustratingly slow. Meanwhile, the second estimate of Q1 Gross Domestic Product (GDP) showed the US economy expanding at an annualised pace of 1.6%, missing expectations and adding another layer of complexity to the policy outlook.

The broader picture remains largely unchanged. Growth continues, inflation remains elevated and policymakers remain caught between upside inflation risks and signs of a gradual cooling in activity. That dilemma was once again reflected in the comments from Federal Reserve (Fed) officials throughout the week.

The Fed Warsh may inherit

Fed speakers repeatedly stressed that inflation remains the primary concern. Neel Kashkari (Minneapolis) warned that inflation risks now outweigh labour market risks. Philip Jefferson (Governor) said risks to inflation remain tilted to the upside. John Williams (New York) reiterated that inflation remains too high and that anchoring expectations remains critical. Alberto Musalem (St. Louis) openly acknowledged that there are scenarios in which rates may need to move higher if inflation fails to improve. Jeffrey Schmid (Kansas City) described inflation as "too hot", while Michelle Bowman (Governor) and Anna Paulson (Philadelphia) both argued that progress on inflation has stalled.

Different officials expressed different degrees of concern, but the message was remarkably consistent.

Inflation remains too high.

The labour market remains broadly stable.

And the Fed remains in no rush to ease policy.

That consensus matters because it raises an increasingly important question for investors.

What exactly should markets expect from a Fed under Kevin Warsh?

The Good, the Bad and the Ugly

For much of this year, investors have treated Kevin Warsh's expected arrival at the Fed as a potentially dovish development.

That assumption may prove premature.

Warsh has often criticised modern central banking, but not necessarily for the reasons many investors assume. While markets tend to focus on the prospect of lower interest rates, Warsh has frequently directed his criticism toward the Fed’s balance sheet, the expansion of excess reserves and the growing role of central banks in financial markets.

In other words, he has often worried less about where rates are and more about how much influence central banks have accumulated since the Global Financial Crisis (GFC).

That distinction matters.

The good is that the White House may get the Fed Chair it wants.

Warsh is widely respected across both policy and financial circles. He understands markets, has extensive central banking experience and has long argued that the Federal Reserve should return to a more focused and disciplined framework. For an administration increasingly frustrated with current policy, he offers both credibility and a fresh approach.

The bad is that investors may not get the dovish Fed they expect.

This week's Fed commentary highlighted a central bank still deeply concerned about inflation, inflation expectations and policy credibility. Those concerns are not particularly different from many of Warsh's own long-standing views. If inflation remains stubborn and growth remains resilient, there is little in his record to suggest he would be eager to sacrifice credibility simply to deliver lower rates.

The ugly is that satisfying everyone may prove impossible.

Trump wants lower rates. Investors want lower rates and abundant liquidity. Many Fed officials remain focused on inflation and preserving the institution's credibility. Those objectives may not always align.

A future Warsh Fed could therefore find itself pulled in three different directions at the same time.

The White House may want faster easing.

Markets may want both lower rates and plentiful liquidity.

Policymakers may continue worrying about inflation that remains stuck well above target.

That leaves Warsh facing the same challenge confronting today's Federal Reserve: balancing political pressure, market expectations and price stability.

Someone is likely to end up disappointed.

Possibly everyone.

Employment FAQs

Labor market conditions are a key element to assess the health of an economy and thus a key driver for currency valuation. High employment, or low unemployment, has positive implications for consumer spending and thus economic growth, boosting the value of the local currency. Moreover, a very tight labor market – a situation in which there is a shortage of workers to fill open positions – can also have implications on inflation levels and thus monetary policy as low labor supply and high demand leads to higher wages.

The pace at which salaries are growing in an economy is key for policymakers. High wage growth means that households have more money to spend, usually leading to price increases in consumer goods. In contrast to more volatile sources of inflation such as energy prices, wage growth is seen as a key component of underlying and persisting inflation as salary increases are unlikely to be undone. Central banks around the world pay close attention to wage growth data when deciding on monetary policy.

The weight that each central bank assigns to labor market conditions depends on its objectives. Some central banks explicitly have mandates related to the labor market beyond controlling inflation levels. The US Federal Reserve (Fed), for example, has the dual mandate of promoting maximum employment and stable prices. Meanwhile, the European Central Bank’s (ECB) sole mandate is to keep inflation under control. Still, and despite whatever mandates they have, labor market conditions are an important factor for policymakers given its significance as a gauge of the health of the economy and their direct relationship to inflation.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.