Monitoring Hungary: Is it time to be optimistic again?

In our latest update, we explore the impact of the recent positive data flow and what the 'stop-and-go' cycles of geopolitical tensions mean for Hungary's economic outlook. In short, we believe the time may be right to be optimistic again.

Hungary: At a glance

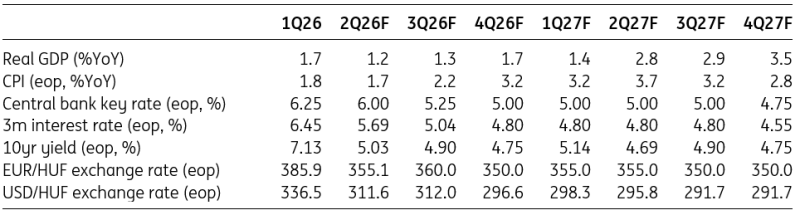

- The outlook for Hungary's GDP growth is improving based on positive surprises in the latest high-frequency data. We can clearly see an upside risk to our full-year forecast of 1.5% for 2026.

- Both retail sales and industrial production have maintained their positive momentum since the beginning of the year, despite the looming geopolitical uncertainty.

- Labour market trends have turned positive, except for one: worsening demographics will continue to put pressure on the supply side, generating pipeline price pressure.

- The external surplus has deteriorated significantly year-on-year, which will eventually result in a current account deficit in 2026.

- Inflation has slowed again, driven by the strength of the forint. Low price pressure is now expected throughout the year, with an average of 2.1% in 2026.

- Investors fell in love with Hungarian assets, driven by a change in power that created space for the central bank to begin cutting rates in June. We have lowered our terminal rate forecast to 4.75–5.00% in 2026.

- The budget deficit has improved for two months, but it will deteriorate again as the absorption of EU funds requires substantial pre-financing. Nevertheless, we believe that the accrual deficit will be better than the government’s recent nowcast.

- EUR/HUF should remain in the 350–360 range as lower volatility and still-attractive carry offset National Bank of Hungary rate cuts and weaker global sentiment.

- Lower inflation, dovish NBH pricing and strong Hungarian government bond demand keep the rally alive, with further curve steepening and spread compression likely.

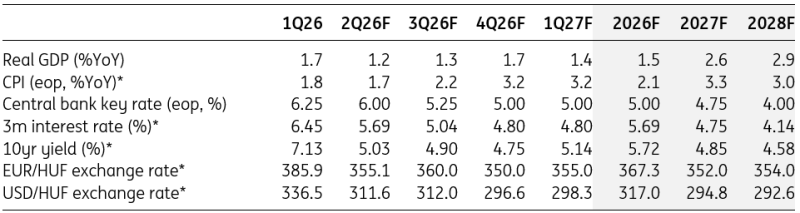

Quarterly forecasts

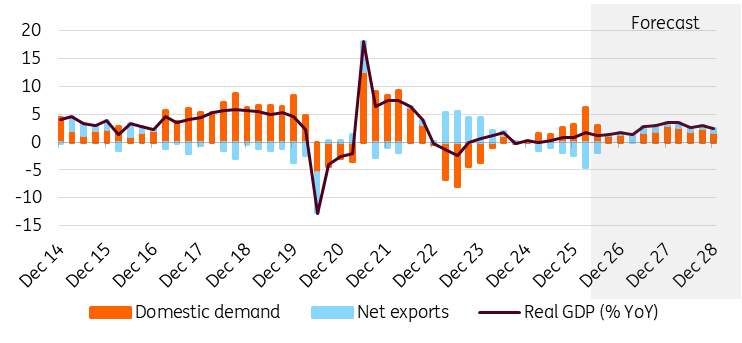

Growth outlook is getting a bit brighter

Although Hungary’s growth picked up in the first quarter, much of this appears to be driven by temporary, pre-election factors rather than a clear, sustained recovery.

Our latest GDP forecast projects a 1.5% increase in 2026. However, this generally gloomy outlook is now accompanied by a clear upside risk, given the latest positive surprises in high-frequency economic activity data. Consumption is expected to drive Hungarian growth this year. While investment may only grow modestly, there are some positive signs in net exports. Nevertheless, we believe that this will hinder GDP expansion. The Finance Ministry expects GDP growth to be in the range of 1.6-2.0% this year, based on the initial projection. This is consistent with broader market expectations.

Real GDP (% YoY) and contributions (ppt)

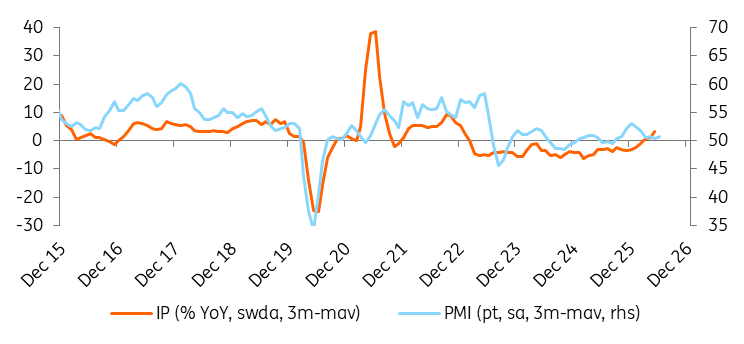

Industry is clawing its way up

Following the April correction, Hungarian industry has continued its upward trajectory, extending the growth trend that began in late 2025. In May, production increased by 2.3% month-on-month, which came as a positive surprise. Production volume declined on a yearly basis in most manufacturing subsectors. However, expansion is happening in two key sectors: electronics and automotive manufacturing.

Although the surge in new export capacity could substantially improve the industrial outlook, current data does not suggest a broad-based recovery. Hungarian industry could achieve an average growth rate of around 4% in 2026. In other words, after three years of industrial recession, the sector could contribute positively to the overall performance of the Hungarian economy once again.

Industrial production (IP) and Purchasing Managers Index (PMI)

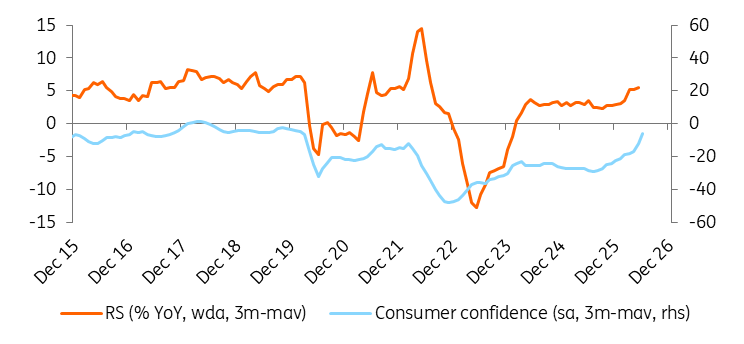

Retail Sales are growing across a wide range of segments

Hungarian retail sales data for May largely met market expectations. Sales volume increased by 0.7% MoM, resulting in a 4.8% YoY rise in the calendar-adjusted index. Retail sales volume now exceeds the monthly average for 2021 by 6.8%. While sales at grocery stores and fuel sales moderated in May, non-food stores performed strongly. Overall, individual retail subsectors continue to be characterised by significant volatility. But growth is fundamentally broad-based, in contrast to industry.

Consumer confidence is approaching historical highs, with persistently low inflation and strong wage growth providing a favourable foundation for sustained growth in the retail sector, and consequently in consumption. We anticipate retail sales growth of around 5-6%, so household consumption will remain the main driver of the economy in 2026.

Retail Sales (RS) and consumer confidence

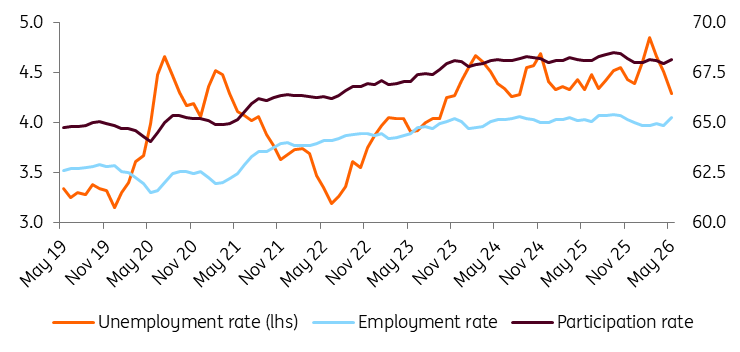

The labour market still flashing strength

Recent labour market figures were better than expected. The official unemployment rate fell to 4.3% in May, which is the lowest rate this year. Labour market participation and employment increased, and the worsening demographic situation also helped improve the ratios. Whether this turnaround will last remains to be seen. Providing greater clarity on domestic economic policy changes could boost business confidence and prevent a negative labour market turnaround.

In the absence of any demographic shift, a significant proportion of companies are likely to continue to hoard labour, keeping the market tight. As the end of the year approaches, the issue of next year's wages is becoming increasingly pressing. The three-year minimum wage agreement is entering its final year in 2027 and will certainly need to be revised. The expected overhaul of the personal income tax system may also create a new challenge.

Historical trends in the Hungarian labour market (%)

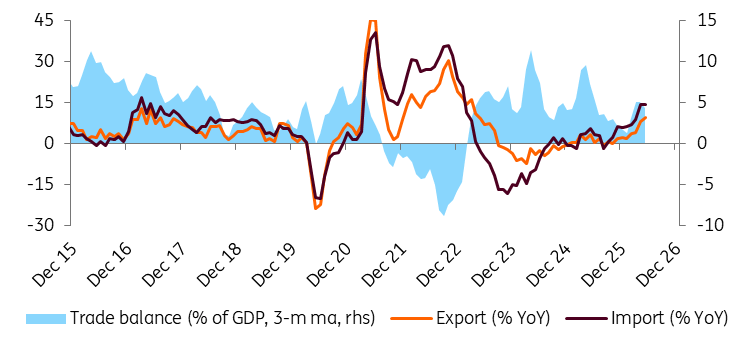

Trade balance and current account surpluses continue to narrow

The goods trade surplus came in at €799m in May 2026. The year-to-date balance deteriorated by €1.2bn year-on-year, showing a positive balance of €3.74bn in May. The volume of exports was 4.5% lower and the volume of imports was 6.4% higher on a yearly basis in the first five months of 2026. Large FDI projects in manufacturing have had an impact on both sides.

On the one hand, machinery and inventory imports are worsening the external balance, while the gradual ramping up of production is boosting export activity. However, limited external demand is keeping exports in check, especially given geopolitical uncertainty. Rising domestic demand will also negatively impact net exports. Regarding the balance of payments, we see the current account turning negative in 2026 following an improvement driven by export capacity in the years ahead.

Trade balance (three-month moving average)

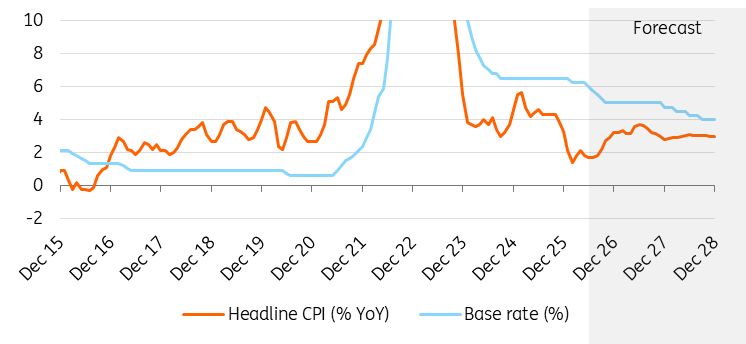

Inflation stays cool during the heatwave

The price level in June 2026 was the same as the previous month. As a fairly low inflation rate had already been expected, this comes as no great surprise. The annual rate of price increases was 1.7%, a decline of 0.1ppt from the previous month. Thus, despite the global energy price shock, Hungarian inflation has not only failed to accelerate, but has actually slowed further over the past two months.

The stronger forint has helped to curb not just food inflation, but also the prices of durable goods. Inflation in the services sector remains the main contributor to overall price pressure, accounting for around two-thirds of total inflation. Thanks to moderating price pressures, households' inflation expectations are approaching a level that could be labelled anchored expectations around the inflation target, and headline inflation may not reach 3% until the end of the year.

Consequently, we are now projecting an average inflation rate of just 2.1% for this year. This could rise to 3.3% in 2027 and 3.0% in 2028.

Inflation and policy rate

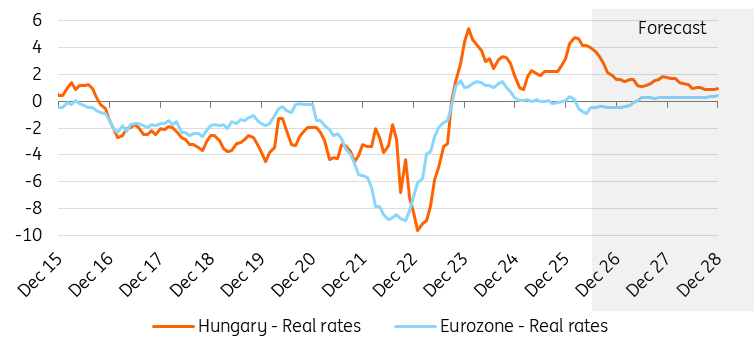

‘Mini’ cutting cycle set to size up

As expected, the Monetary Council voted to reduce the base rate by 25bp to 6.00% on 23 June. Governor Varga also stated that this marks the beginning of a 'mini rate cut cycle' until September. In its latest inflation report, the National Bank of Hungary lowered the expected inflation trajectory significantly and increased the forecasted GDP growth.

Positive geopolitical changes, near record-high levels of consumer confidence and a strengthening forint made it possible for the central bank to start cutting rates and commit to doing so. Looking ahead, if the external environment remains supportive and local politics deliver on previous commitments regarding the euro adoption plan, EU funding developments and long-term fiscal adjustments, the risk premium for Hungarian assets could persistently remain low. In this case, we forecast a 'mini' rate cut cycle involving four or five further cuts following June's move. Our terminal rate for this year is 4.75–5.00%.

Real rates (%)

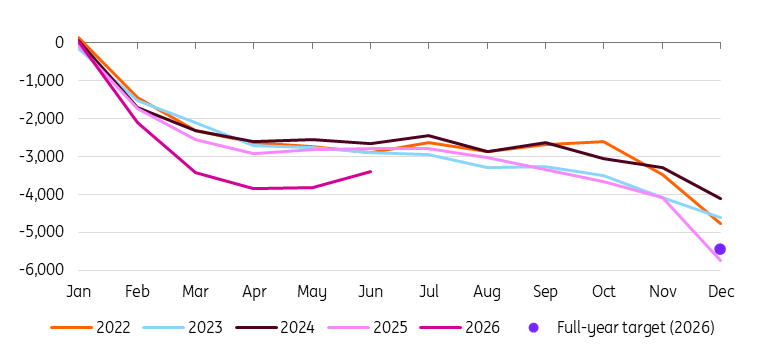

The budget can improve even this year

By the end of June, the central government sector had recorded a deficit of HUF 3,382bn. Thanks to monthly surpluses in May and June, the latter of which was a particularly positive surprise, the 12-month rolling deficit finally turned around. However, due to the pre-financing requirements for the full utilisation of EU funds, the situation will start to deteriorate soon.

According to a review conducted by the new government, the accrual deficit would have amounted to 8.3% of GDP had there been no change in government. Due to the government's actions to date and the agreement with the EU, the projected deficit for this year (without additional measures) has been reduced to 7.5% of GDP. The government will amend the 2026 budget and set a new deficit target by the end of August, so the 7.5% figure is merely a starting point for planning. We think that the actual data will be around 6.5%. By the end of October, the Ministry of Finance will submit the 2027 budget and prepare the medium-term budget plan in line with the sub-3% deficit target by 2030.

Budget performance in cash-flow perspective (year-to-date, HUFbn)

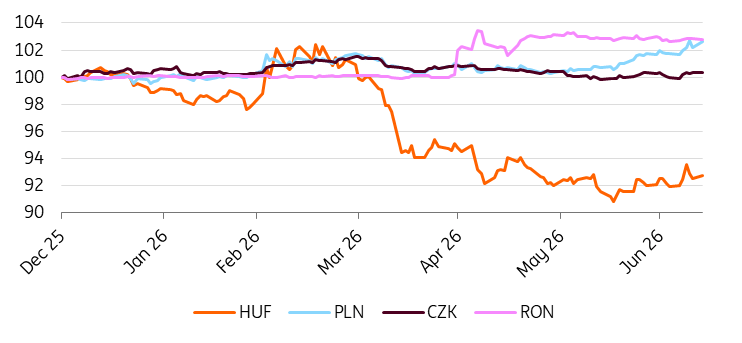

Carry still pays as EUR/HUF stays locked in the range

EUR/HUF rebounded from the June low near 350 and has since settled into a 350–360 range. Implied volatility has fallen but remains above CEE peers. Since the April general election, EUR/HUF has traded in a largely self-contained environment, with global factors having less influence than elsewhere in the region. Even with the NBH signalling a rate-cut cycle and interest rate differentials tightening meaningfully, the currency has shown limited sensitivity.

Looking ahead, we expect EUR/HUF to remain stable, with the second half of 2026 likely dominated by range trading within 350–360 and a further decline in volatility. While markets may price additional rate cuts from current levels, rates appear to have a limited impact on FX for now. Recent Middle East-related headlines and weaker global sentiment have done little damage to the forint, with any softness quickly absorbed by the market. Despite NBH rate cuts, FX carry remains attractive within EM, and the positive local story could draw further carry demand over the summer, particularly if volatility keeps falling.

CEE FX performance vs EUR (31 Dec 2025 = 100%)

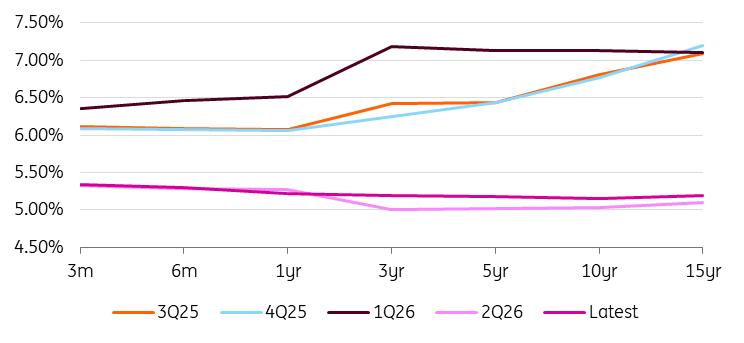

Rally has further to run as NBH pricing and demand stay supportive

Since the general election, almost every inflation print and NBH meeting has given rates and bonds a reason to rally. After June inflation came in below the NBH forecast, market pricing has stabilised around a 4.50% terminal rate over the two-year horizon. Compared with our forecast and the market’s 2024 lows, we still see room for a further rally. In early 2024, markets priced a 4.25% terminal rate despite a much less favourable backdrop for the central bank. We therefore expect the curve to move lower, with a continued steepening bias and further spread compression versus core and CEE markets.

Hungarian sovereign yield curve (end of period)

In bonds, the debt agency has seen strong demand for Hungarian government bonds since the start of the year, with momentum accelerating after the April general election. The uncertain fiscal outlook makes this year’s funding need difficult to estimate. But under the old plan based on a 5% ESA deficit, around 80% of issuance has already been covered, including switches and next year’s pre-funding.

After the latest euro-denominated deal, the debt agency also indicated that FX issuance is complete for this year. This leaves HGBs as the main funding tool, while the agency is likely to keep taking advantage of strong demand. That supports further curve steepening, although the long end should continue to benefit from euro adoption expectations and EU funds inflows.

Forecast summary

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.