Banks and inflation face a crucial test as Wall Street eyes the next leg higher

Wall Street faces one of its busiest sessions of the earnings season today, with investors navigating a powerful combination of inflation data, big-bank earnings and the first Congressional testimony from Federal Reserve Chair Kevin Warsh.

Before the opening bell, JPMorgan Chase, Bank of America, Goldman Sachs, Citigroup and Wells Fargo are all scheduled to report second-quarter earnings. Just thirty minutes later, June’s Consumer Price Index (CPI) will provide the latest reading on inflation before markets open, with Warsh taking to Capitol Hill shortly after the opening bell.

It is a rare convergence of macroeconomic and corporate catalysts that will determine whether equities can extend their rally or whether expectations have simply become too optimistic.

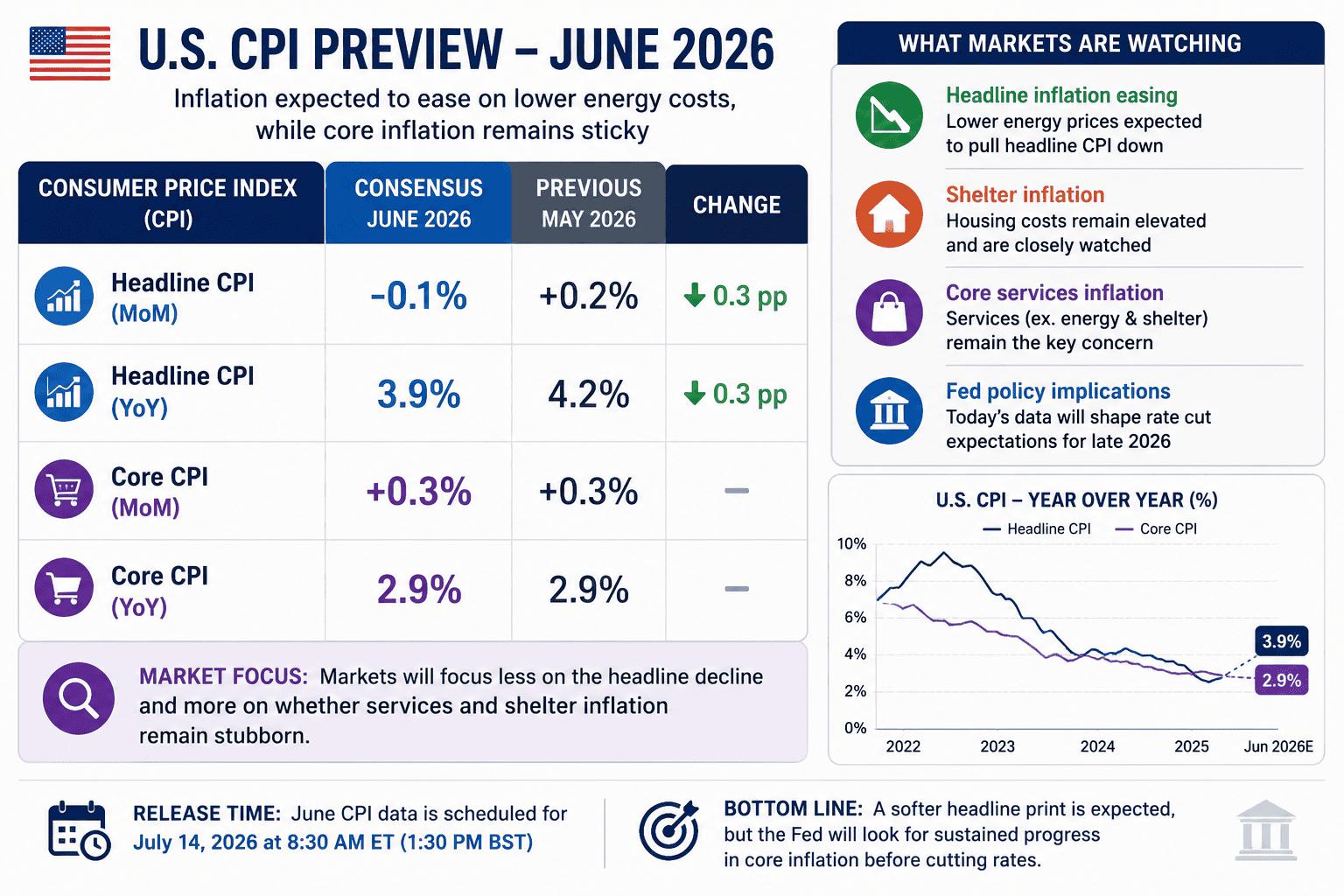

Inflation: Headline relief, but core pressures remain

Markets expect June’s CPI report to show a noticeable improvement in headline inflation, largely thanks to lower energy prices during the month.

Consensus forecasts point towards:

- Headline CPI: -0.1% month-on-month, easing annual inflation towards 3.9%.

- Core CPI: +0.3% month-on-month, holding near 2.9% year-on-year.

While a softer headline number would be welcomed by investors, markets are likely to pay closer attention to the composition of inflation rather than the headline itself.

Housing, insurance and services inflation have remained sticky throughout the year, and policymakers have repeatedly stressed that underlying inflation—not temporary swings in energy—will determine the future path of interest rates.

That means even an encouraging CPI print may not significantly alter expectations if core inflation remains stubborn.

Banks begin earnings season

Today’s bank earnings represent much more than individual company results—they provide one of the clearest snapshots of the health of the US economy.

Unlike previous quarters, expectations heading into earnings remain relatively optimistic.

Analysts broadly expect year-on-year earnings growth across the major banks, supported by resilient consumer spending, improving investment banking activity and solid trading revenues following elevated market volatility.

However, the market has already priced in much of that optimism.

Investors are likely to focus less on whether earnings beat consensus estimates and more on management commentary surrounding:

- Consumer credit quality.

- Loan demand.

- Net interest income.

- Commercial lending activity.

- Corporate confidence.

- Outlooks for the second half of the year.

Strong trading revenues can help produce earnings beats, but sustainable loan growth and healthy consumer balance sheets would provide far stronger evidence that economic momentum remains intact.

Jamie Dimon’s comments at JPMorgan are once again expected to set the tone for the sector, while Goldman Sachs will offer insight into whether capital markets activity continues to recover. Bank of America remains one of the clearest gauges of consumer strength through its lending business, while Citigroup’s restructuring progress and Wells Fargo’s turnaround efforts round out a comprehensive view of the financial sector.

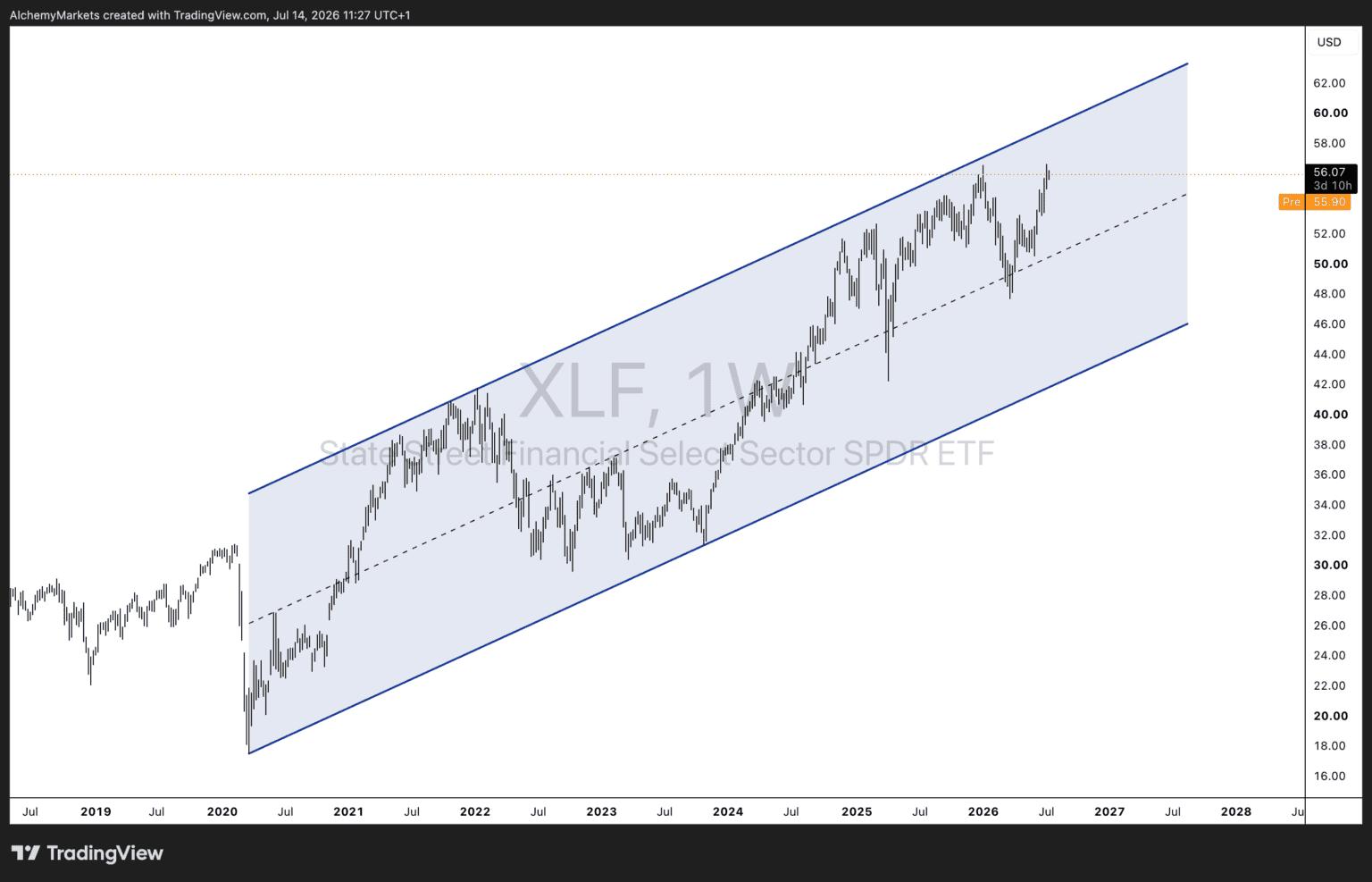

A high bar for the financial sector

Financial stocks have already enjoyed a strong run this year, leaving little room for disappointment.

The Financial Select Sector SPDR ETF (XLF) continues to trade within a well-defined long-term ascending channel, with prices approaching the upper boundary of that trend.

The technical picture remains constructive, but the sector is now approaching an area that has historically acted as resistance rather than a launching point.

If today’s earnings demonstrate continued loan growth, resilient credit quality and confident guidance, investors could view that upper channel as a target rather than a ceiling.

However, should management teams signal slowing lending activity, rising credit costs or more cautious business investment, the current rally may struggle to justify further gains without a period of consolidation.

Oil returns to the inflation conversation

Although June’s CPI is expected to benefit from weaker energy prices, markets must also contend with what comes next.

West Texas Intermediate (WTI) crude has staged a sharp recovery over recent weeks and is now approaching an important technical resistance area near $85 per barrel.

That level carries significance beyond the oil market itself.

A sustained move above $85 would risk reigniting inflation concerns during the second half of the year, potentially complicating the Federal Reserve’s policy outlook even if today’s inflation report proves encouraging.

For investors, this creates an important distinction between today’s data and tomorrow’s inflation expectations.

A favourable June CPI reading may provide short-term relief, but renewed strength in energy markets could quickly challenge the notion that inflation has been fully contained.

Looking ahead

Today’s session presents investors with a compressed sequence of market-moving events.

Strong bank earnings accompanied by healthy guidance and softer-than-expected inflation would likely reinforce confidence that the US economy continues to navigate higher interest rates remarkably well.

However, expectations have risen alongside equity markets.

Should bank executives adopt a more cautious tone, or if core inflation proves stickier than anticipated, investors may begin questioning whether recent gains—particularly across financials—have already priced in much of the good news.

With inflation, earnings and the Federal Reserve all taking centre stage within the space of just a few hours, today’s opening bell could prove one of the most consequential of the quarter.

Author

Zorrays Junaid

Alchemy Markets

Zorrays Junaid has extensive combined experience in the financial markets as a portfolio manager and trading coach. More recently, he is an Analyst with Alchemy Markets, and has contributed to DailyFX and Elliott Wave Forecast in the past.