US Dollar Weekly Forecast: Investors will closely follow US CPI and Retail Sales

- US Dollar Index (DXY) bounced off multi-month lows.

- Focus remains on potential developments around the Yen.

- Fears around a potential US recession have dissipated for now.

Decent contention emerged near 102.00

Following Monday’s pronounced drop to seven-month lows in the 102.20-102.15 band, it's been all the way up for the US Dollar Index (DXY) since then.

However, that bullish move appears to have run out of steam near 103.50 in tandem with further recovery in global stock markets after recent turbulence, a normalized performance of the Japanese Yen, and somewhat more stable volatility.

All in all, the index ended the week barely changing from the previous one, maybe leaving the door open to continuation of the weekly rebound in the upcoming week.

Recession fears could threaten the Fed’s divergence in monetary policy

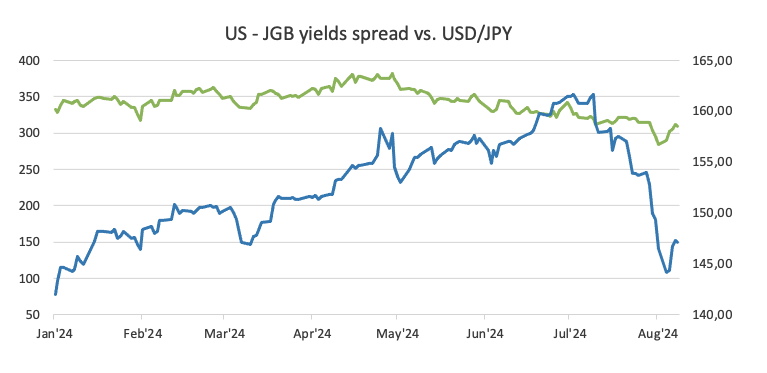

Quite a chaotic week for risk-related assets was the result of the Bank of Japan’s (BoJ) unexpected decision to hike rates by 15 bps to 0.25%, a move that caught markets off guard and triggered a strong unwind of the most famous carry trade.

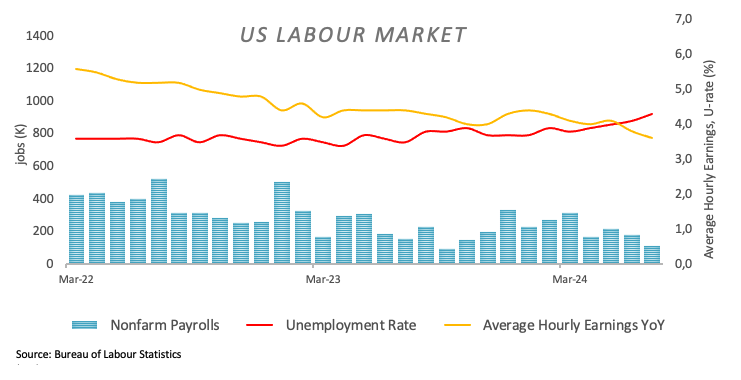

Additionally, July’s lower-than-expected job creation in the US economy, as per Nonfarm Payrolls (+144K jobs), sparked renewed concerns that the US economy might tip into recession, a view that was reinforced by further weakness in the manufacturing sector.

That powerful cocktail reignited strong speculation that the Federal Reserve (Fed) might call an emergency meeting and anticipate a rate cut, a move that, despite being highly unlikely, sent the US Dollar to multi-month lows along with prospects of more and deeper interest rate cuts. That scenario, of course, did not materialize, and it did not come even close to it.

What it indeed did was accelerate the probability of a 50 bps rate cut by the Fed at its September 18 meeting, which, according to CME Group’s FedWatch Tool, now stands near 55% (from around 70% just a couple of days ago).

Now, about those recession concerns, are markets really of the idea that US economic activity could face such a slowdown?. A couple of Fed officials were in charge of clearing the skies of such dark clouds at the beginning of the week.

In fact, Chicago Fed President Austan Goolsbee argued earlier in the week that the US economy is not in recession despite weaker-than-expected job data. He emphasized the need for policymakers to monitor changes in the environment to avoid being too restrictive with interest rates. His colleague, San Francisco Federal Reserve Bank President Mary Daly, emphasized the importance of the central bank to avert a downturn in the labour market and expressed confidence that domestic inflation is moving toward the bank’s 2% goal, despite the labour market slowing.

Meanwhile, the European Monetary Union (EMU), Japan, Switzerland, and the United Kingdom are all experiencing growing disinflationary pressures. In response, the European Central Bank (ECB) lowered rates by 25 bps in June and maintained a dovish approach in July, with policymakers suggesting the possibility of another rate cut later in the year (September maybe?). Similarly, the Swiss National Bank (SNB) unexpectedly cut rates by 25 bps on June 20, and the Bank of England (BoE) reduced its policy rate by a quarter-point on August 1. On the other hand, the Reserve Bank of Australia (RBA) delivered a hawkish hold at its event on August 6, and investors anticipate that the bank could begin its easing cycle in the first quarter of 2025. In contrast, the Bank of Japan (BoJ) surprised markets on July 31 by delivering a hawkish message and raising rates by 15 bps to 0.25%.

Rate cuts are still coming

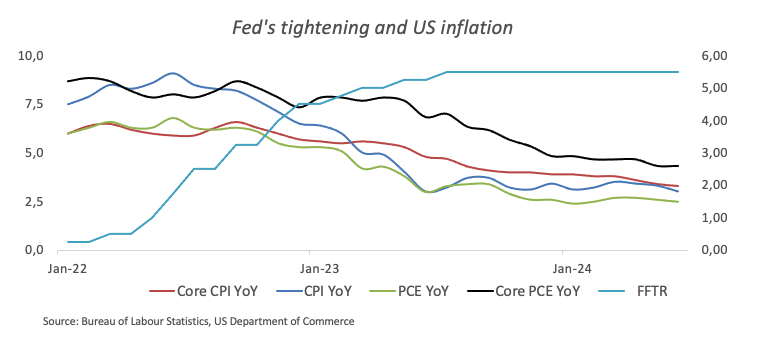

Growing market speculation about an earlier start to the Fed's easing cycle has been fuelled by the ongoing decline in domestic inflation, along with a gradual slowdown in key sectors like the labour market and manufacturing.

It's important to recall that at the Fed’s most recent meeting on July 31, Chair Jerome Powell highlighted the need for greater confidence in managing inflation, pointing to Q2 inflation data as supportive evidence. He indicated that the Fed is moving closer to considering a potential rate cut. Powell mentioned that if inflation continues to fall, economic growth stays strong, and the labour market remains stable, a rate cut could be on the table, possibly as early as September.

In the longer term, the growing possibility of another Trump administration and the potential reimplementation of tariffs could disrupt or even reverse the current disinflationary trend in the US economy, which might shorten the planned Fed easing cycle.

US yields showed signs of life

Over the past week, the US money market showed an accelerated rebound in yields, which managed to regain some upside traction after hitting multi-week lows across various maturity periods.

Upcoming key events

The publication of US inflation figures tracked by the Consumer Price Index (CPI) will take centre stage next week. In the same line of relevance will be the release of Retail Sales, which is expected to shed further light on recent recession fears.

Techs on the US Dollar Index

The DXY has decisively broken below the key 200-day SMA around 104.20, maintaining the open door to potential weakness, at least in the near term. As long as it remains below this crucial level, the outlook for the Greenback is expected to stay bearish.

Should sellers regain control, the US Dollar Index (DXY) may initially decline to its August low of 102.16 (August 5), followed by the December 2023 low of 100.61 (December 28), and the psychological barrier of 100.00.

On the upside, the DXY faces immediate resistance at the key 200-day SMA of 104.20, prior to the weekly high of 104.79 (July 30). If this region is cleared, DXY could potentially advance toward the June peak of 106.13 (June 26), ahead of the 2024 high of 106.51 (April 16).

Economic Indicator

Consumer Price Index (YoY)

Inflationary or deflationary tendencies are measured by periodically summing the prices of a basket of representative goods and services and presenting the data as The Consumer Price Index (CPI). CPI data is compiled on a monthly basis and released by the US Department of Labor Statistics. The YoY reading compares the prices of goods in the reference month to the same month a year earlier.The CPI is a key indicator to measure inflation and changes in purchasing trends. Generally speaking, a high reading is seen as bullish for the US Dollar (USD), while a low reading is seen as bearish.

Read more.Next release: Wed Aug 14, 2024 12:30

Frequency: Monthly

Consensus: 2.9%

Previous: 3%

Source: US Bureau of Labor Statistics

The US Federal Reserve has a dual mandate of maintaining price stability and maximum employment. According to such mandate, inflation should be at around 2% YoY and has become the weakest pillar of the central bank’s directive ever since the world suffered a pandemic, which extends to these days. Price pressures keep rising amid supply-chain issues and bottlenecks, with the Consumer Price Index (CPI) hanging at multi-decade highs. The Fed has already taken measures to tame inflation and is expected to maintain an aggressive stance in the foreseeable future.

US Dollar PRICE Today

The table below shows the percentage change of US Dollar (USD) against listed major currencies today. US Dollar was the strongest against the Australian Dollar.

| USD | EUR | GBP | JPY | CAD | AUD | NZD | CHF | |

|---|---|---|---|---|---|---|---|---|

| USD | -0.04% | -0.12% | -0.44% | -0.03% | 0.16% | -0.08% | -0.24% | |

| EUR | 0.04% | -0.06% | -0.32% | 0.00% | 0.18% | -0.05% | -0.20% | |

| GBP | 0.12% | 0.06% | -0.26% | 0.05% | 0.26% | 0.01% | -0.13% | |

| JPY | 0.44% | 0.32% | 0.26% | 0.32% | 0.55% | 0.28% | 0.17% | |

| CAD | 0.03% | -0.01% | -0.05% | -0.32% | 0.19% | -0.05% | -0.19% | |

| AUD | -0.16% | -0.18% | -0.26% | -0.55% | -0.19% | -0.25% | -0.39% | |

| NZD | 0.08% | 0.05% | -0.01% | -0.28% | 0.05% | 0.25% | -0.14% | |

| CHF | 0.24% | 0.20% | 0.13% | -0.17% | 0.19% | 0.39% | 0.14% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the US Dollar from the left column and move along the horizontal line to the Japanese Yen, the percentage change displayed in the box will represent USD (base)/JPY (quote).

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.