US Dollar forecast: 25bps cut drags USD to further downside [Video]

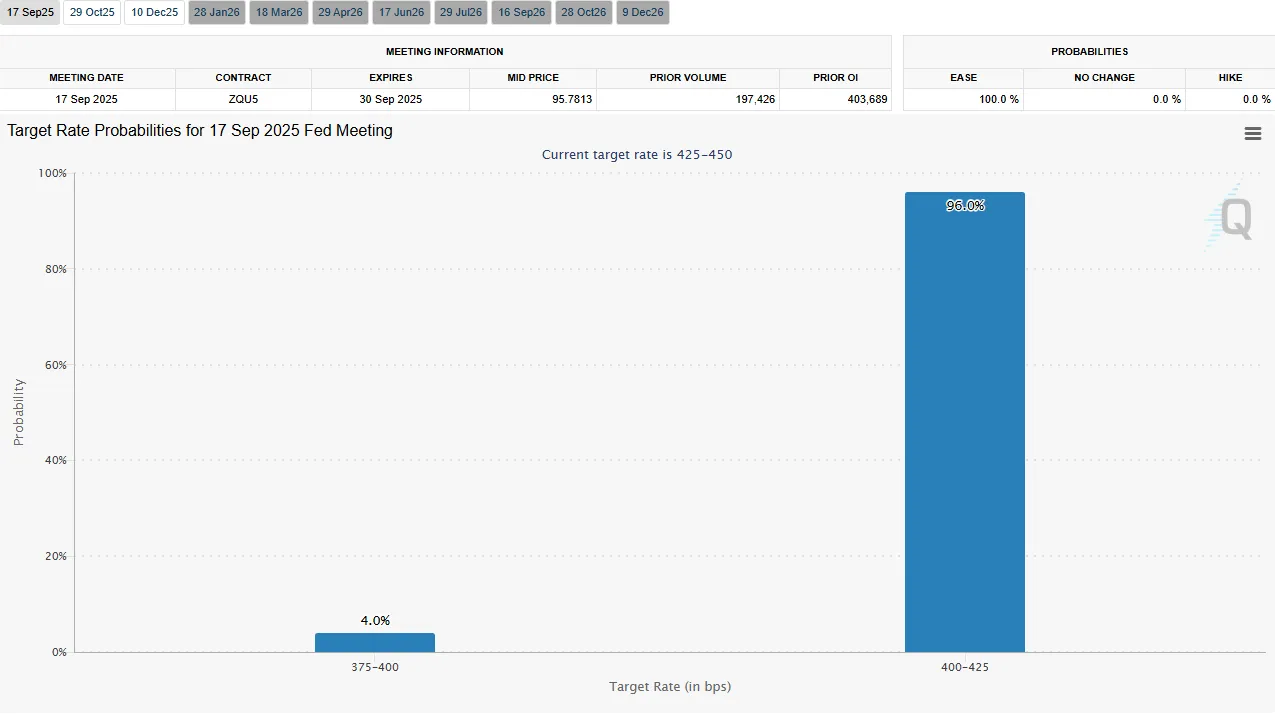

- Dollar slides into FOMC week as traders price a September cut and a potential easing path into year-end.

- Sticky CPI but softer producer inflation keeps real yields heavy; August CPI rose 0.4% m/m, 2.9% y/y, while PPI momentum eased.

- Near-term bearish USD bias below 97.80 on DXY, with 97.00 as the key pivot ahead of the Fed.

![US Dollar forecast: 25bps cut drags USD to further downside [Video]](https://editorial.fxsstatic.com/images/i/USD_Neutral-Tendency-2.png)

USD narrative: “Cuts are coming – But how fast?”

The U.S. dollar enters this FOMC week on the back foot. Positioning has rotated out of the greenback as markets lean into a first 25 bp cut in September and a series of trims into early 2026, a stance reinforced by a visibly softer labor backdrop and easing producer inflation. As rate-cut odds firm, Treasury yields have edged lower and the dollar has slipped to multi-week lows versus the euro and multi-month lows versus high-beta FX.

On inflation, headline CPI for August printed 0.4% m/m and 2.9% y/y, with core at 3.1% y/y—still above target but drifting in the right direction. PPI cooled on a trend basis, signaling weaker pipeline pressure. This mix—not too hot, not too cold—lets the Fed pivot without declaring victory on inflation. The result is a “dovish, but cautious” setup into Wednesday’s policy decision.

The consumer remains the swing factor. August retail sales land today and are expected to slow to around 0.2% m/m, a step down from mid-year resilience. A soft print would validate the easing path and keep the dollar heavy; a beat risks a “dovish-cut, hawkish-guidance” read that could spark a brief USD short-squeeze.

Why the Fed is cutting rates this week

The Fed’s basis for a September rate cut rests on three pillars:

- Labor market weakness

- August nonfarm payrolls added just ~22k jobs, with unemployment climbing to 4.3%, the highest since late 2020.

- Job openings data (JOLTS) and revisions to earlier payrolls show a labor market losing steam, easing wage pressures and lowering inflation risk.

- Inflation convergence

- Headline CPI has slowed from 3.4% in June to 2.9% in August, and core inflation is following the same path.

- Producer prices (PPI) have softened, suggesting pipeline pressures are not feeding into consumer inflation as aggressively as before.

- Financial conditions and growth risks

- Equity markets are at all-time highs, but credit markets reflect a cautious outlook with flattening yields and rising stress in commercial real estate.

- Consumer spending, while resilient, is showing cracks—retail sales growth has slowed, and sentiment surveys point to weakening demand into Q4.

In short, the Fed is cutting rates not because inflation is fully defeated, but because the risk of overtightening now outweighs the risk of lingering price pressures. The cut is framed as insurance against stagnation, giving the Fed breathing room to adjust policy while keeping longer-term credibility intact.

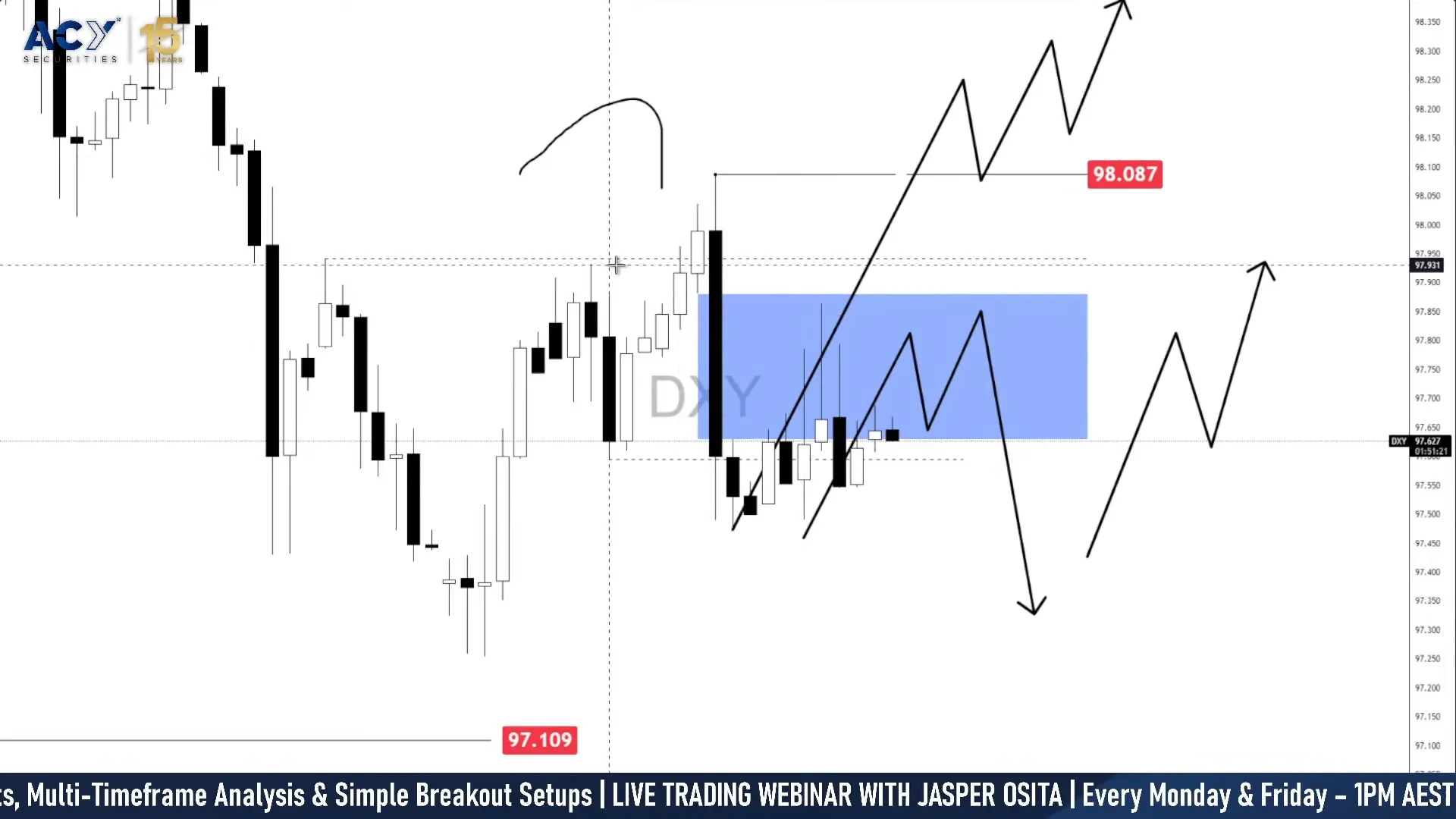

Technical outlook (DXY)

Before vs after price action

The Dollar Index (DXY) has respected the broader bearish structure, sliding from the blue supply/FVG zone (97.80–98.00) into the 97.20 region, confirming the earlier forecast of a rejection lower.

This shift validates the downside momentum ahead of the Fed decision but leaves room for tactical rebounds if buyers defend near-term liquidity pools.

Technical outlook: DXY after hitting the 97 zone

The chart shows that the Dollar Index (DXY) has already tapped into the 97.20–97.10 liquidity pool, which we highlighted earlier as a key downside target. This reaction leaves two possible paths: either the level acts as a springboard for a corrective recovery rally, or sellers press further to break below 97.00 and extend the downtrend. The drawn projections illustrate these alternative outcomes—one pointing to a bounce toward 97.50–97.80, the other showing a continuation leg lower into fresh lows.

Bullish scenario: Short-term recovery rally

After sweeping 97.20–97.10, price could stabilize and stage a corrective bounce.

- Upside targets: 97.40–97.50 intraday resistance, followed by 97.70–97.80.

- Break and close above 97.80 unlocks 98.00–98.10, setting up a pre-FOMC squeeze.

- Invalidation: Failure to defend 97.00 negates the bullish case.

Bearish scenario: Continuation through support

Sellers remain in control with lower-highs intact.

- Breakdown below 97.10/97.00 confirms continuation toward 96.80, with scope for 96.50 if dovish Fed tone persists.

- Intraday rallies into 97.40–97.50 may act as distribution zones before another leg lower.

- Invalidation: Daily close above 97.80 would weaken bearish momentum.

Author

Jasper Osita

Independent Analyst

Jasper has been in the markets since 2019 trading currencies, indices and commodities like Gold. His approach in the market is heavily accompanied by technical analysis, trading Smart Money Concepts (SMC) with fundamentals in mind.