US Data To Close Out An Active Week In The Market

A steady stream of economic data will make its way through the markets on Friday, giving investors key insight into the US and Eurozone economies. The North American session will be especially active, with reports on consumer spending and industrial production set to make headlines.

The data wire begins at 10:00 GMT with a report on Eurozone trade. The Eurozone’s non-adjusted trade surplus is forecast to drop to €21.4 billion in July from €26.6 billion the previous month.

One hour later, the Bank of England (BOE) will issue its Quarterly Bulletin, which provides regular commentary on market developments in the British economy. The BOE left interest rates on hold Thursday but sent a strong signal that changes are afoot.

Several high-profile releases headline the North American session, beginning at 12:30 GMT with retail sales. Receipts at retail stores are forecast to rise 0.1% in August after climbing 0.6% the month before. Excluding automobiles, sales are projected to rise 0.5%.

At the same time, the New York Federal Reserve Bank will release the monthly Empire State manufacturing index, which gauges business conditions for regional manufacturers.

Factory data will be front and centre at 13:15 GMT when the Fed reports on industrial production for the month of August. Output is forecast to rise 0.1% from July, following an increase of 0.2% the month before. The capacity utilization rate is expected to edge up slightly to 76.8%.

The University of Michigan will unveil its closely-watched consumer sentiment index at 14:00 GMT. The preliminary September report is expected to show a decline in consumer confidence.

The Commerce Department will report on business inventories at 14:00 GMT. Three hours later, Baker Hughes Inc. will release its weekly rig-count data.

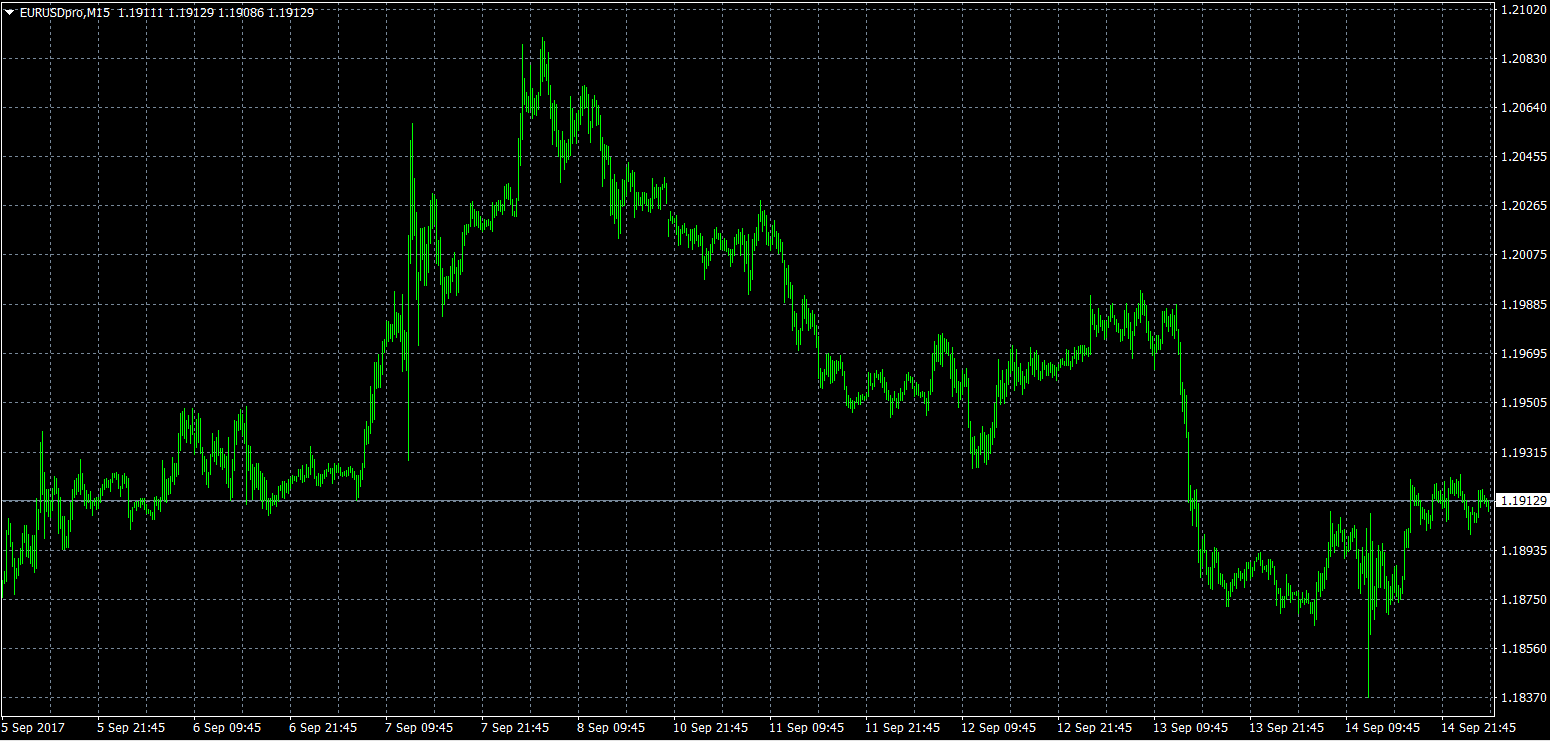

EUR/USD

The euro stabilized on Thursday after a series of sharp declines pulled prices away from new multiyear highs. The EUR/USD exchange rate was last seen trading at 1.1911, where it was little changed. The EUR/USD remains well supported, as traders continue to buy on the dips. This is likely to continue in the short term.

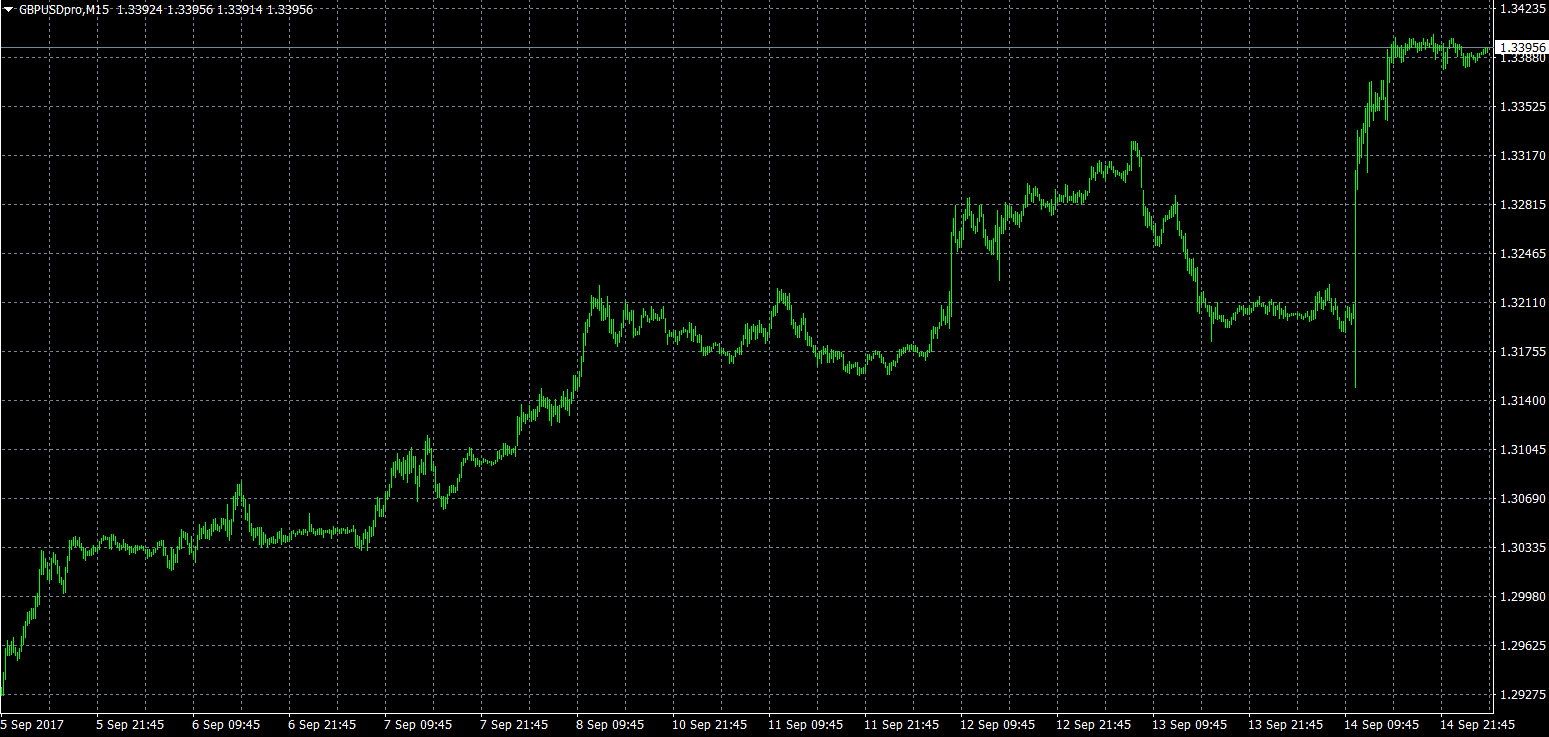

GBP/USD

The British pound put up a massive rally on Thursday after the BOE said a rate hike could be warranted in the coming months. The GBP/USD gained nearly 200 pips for the day. Cable is now eyeing the 6 September 2016 high of 1.3447 as the next target. Immediate support is located in the mid-1.31 region, which corresponds with the low from 8 September.

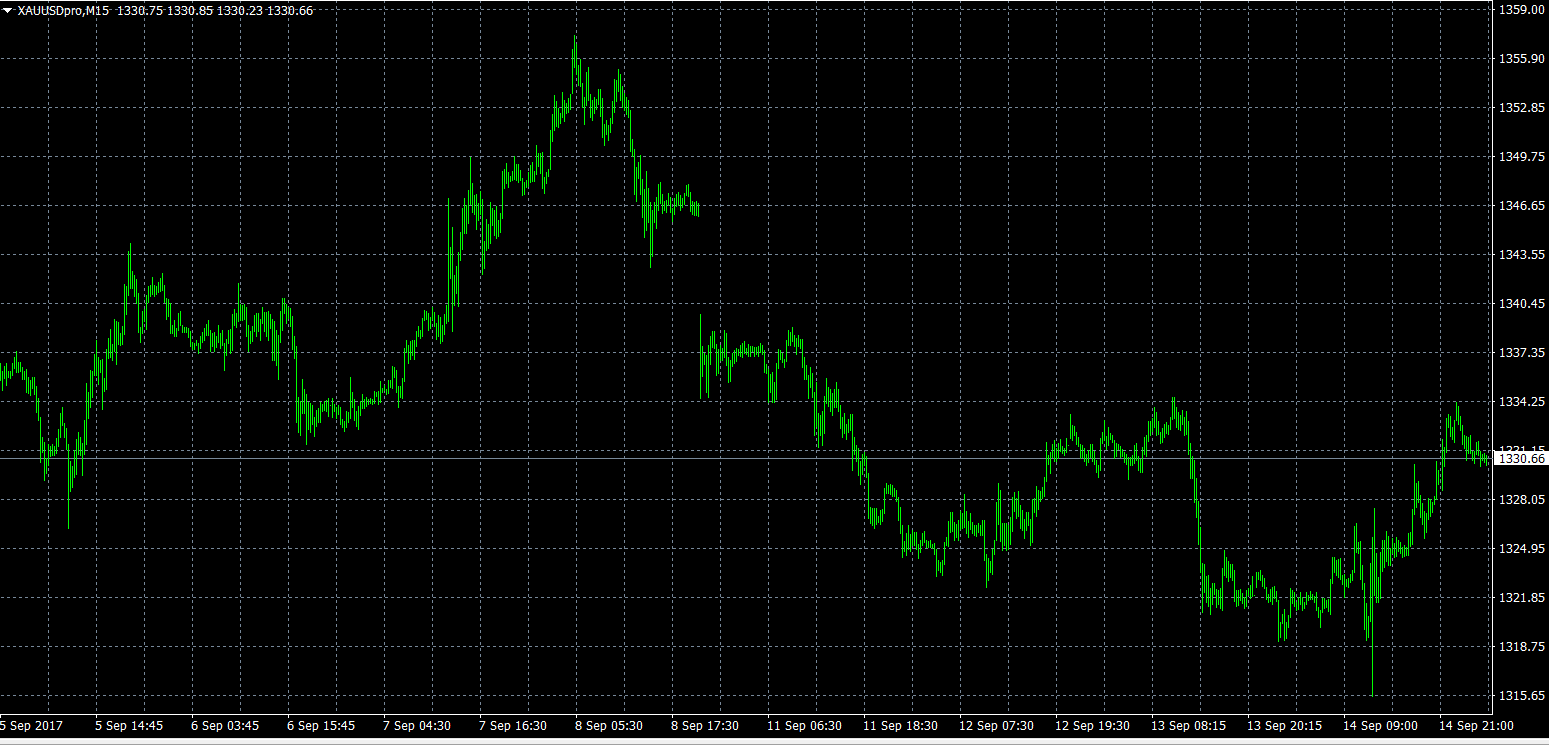

GOLD

Gold prices are on track for a large weekly decline, as the US dollar stabilized and risk appetite returned to the financial markets. Spot gold was last seen trading around $1,331.00 a troy ounce. Bullion maintains a bullish outlook after a convincing rally pushed prices north of $1,300.00 – a level that had proven difficult to penetrate all year long.

Author

OctaFx Analyst Team

OctaFX

OctaFX is a market-leading forex broker, providing personalised forex brokerage services to customers in over 100 countries worldwide.