US Consumer Price Index: The pandemic inflation decline reverses

- Core and headline rates expected to be flat in May, up from April deflation.

- West Texas Intermediate rises 88% in May after falling 56% in March and April.

- Payrolls suggest returning consumption may help support prices.

- Retail sales predicted to climb 7% in May following April's 16.4% decline.

- Dollar is back to pre-pandemic levels in the major pairs.

The April drop in consumer prices was driven by two factors-the economic shutdown induced collapse in consumption and the plunge in oil price-both have been reversed in May.

As large sectors of the US economy closed in April and a quarter of the workforce was thrown onto unemployment retail sales fell 16.4% and personal consumption dropped 13.6%, each the largest monthly decrease on record.

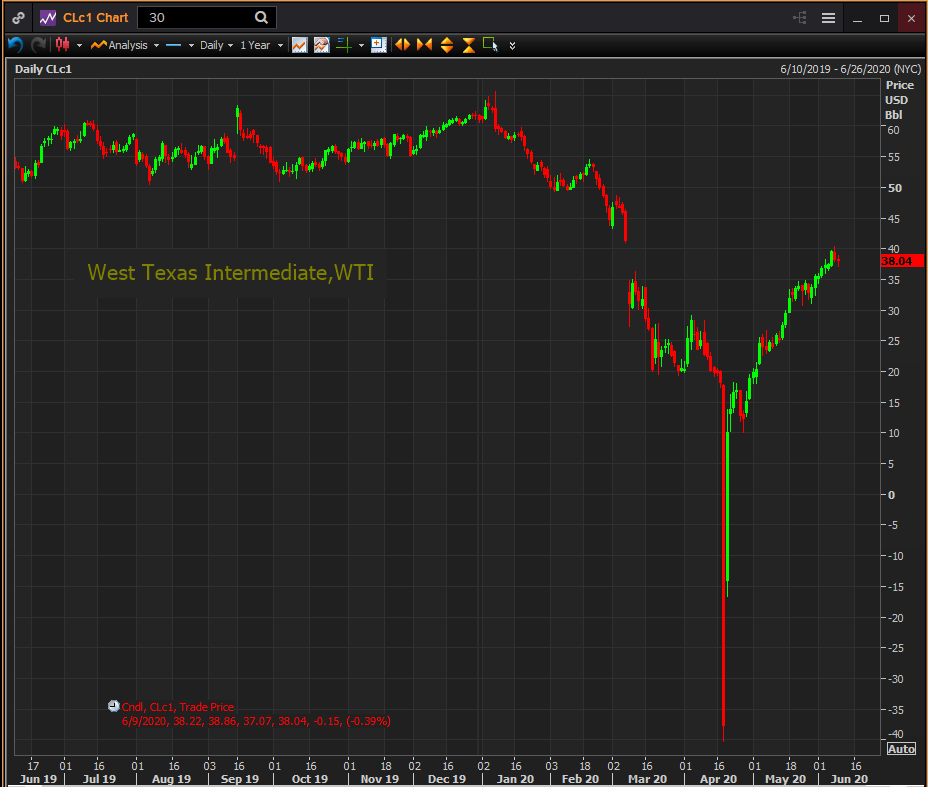

April also produced the historic if brief inversion in the West Texas Intermediate (WTI) May futures contract which closed at -$37.63 on April 20. From March 1 to the end of April the WTI barrel price dropped57%. The average price of $16.67 in April was the lowest in 21 years.

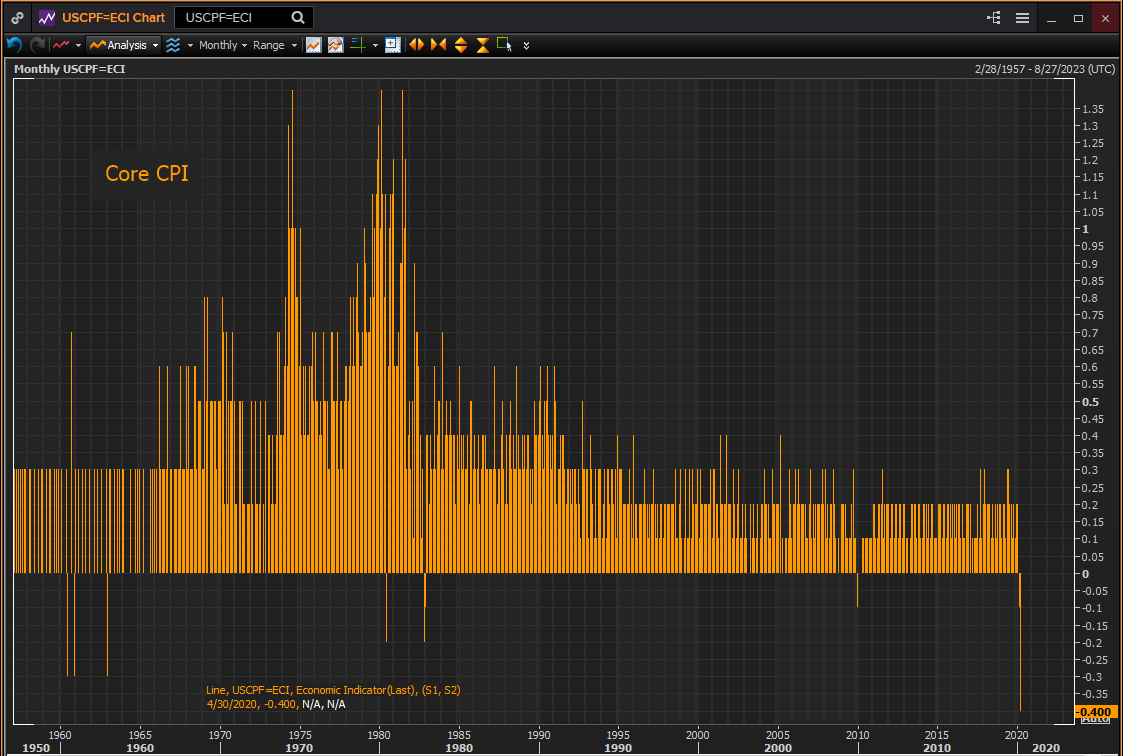

The combination produced the largest one month decline in core CPI, 0.4%, in the 63 years history of the statistic and the fourth largest, 0.8%, in the 73 year record of the overall index. The annual core rate was 1.4% in April and the overall rate was 0.3%.

Outright declines in the core index are very rare. April was only the eighth instance of a drop in the monthly core CPI rate in the 747 months of the series back to February 1957. Declines in the overall rate are much more common with over sixty in the 73 years of the index.

Consumer Price Index, consumption and payrolls

The consumer price index is expected to rise to 0.0% in May from -0.8% in April and-0.4% in March. The annual rate is forecast to slip to 0.2% from 0.3%. The core rate is projected to be flat in May from March’s -0.4% and April’s -0.1%.

As with the March and April CPI declines due to the plunge in consumption, the end of business closures in much of the country in May, the jump in non-farm payrolls and the expected May 7% gain in retail sales, (3.8% in the control group, April -15.3%) should halt the price cutting forced on retailers in March and April by the desperate effort to clear inventory.

Non-farm payrolls added 2.5 million workers in May after 20.5 million were forced out of their jobs in April.

That wholly unexpected increase, analysts had forecast a drop of 9 million, suggests that the economic reopening which started in Georgia in late April followed by Texas and Florida and now covers the entire nation to a greater or lesser degree has returned far more workers to employment than anticipated.

Even New York City the epicenter of the US pandemic has permitted many businesses in city a limited reopening, though large commercial sections of Manhattan remain empty of pedestrians and office workers, with stores boarded and many gutted by the recent riots.

WTI

The 57% drop in oil prices in March in April (CLc1, open 3/2 $43.70, close 4/30 $18.84) largely reversed in May with the month’s finish at $35.49 just 19% below the March open and 88% above the April close.

Reuters

With reported consumption in China on the rise, OPEC+ extending their production cuts to the end of July and the US and Europe restarting their economies, oil looks to be supported at these levels with a bias higher if the globe recovers faster than anticipated.

Fed, CPI and PCE

The consumer price index is the lead for the Federal Reserve’s preferred inflation indicator the core personal consumption price index (core PCE), -0.4% in April, at the end of the month. The two move in close association though the CPI gauge tends to produce higher reading.

The Fed’s ostensible 2% core PCE target has been mostly ignored in policy and missed in practice since the financial crisis. Chairman Powell and the governors routinely mention it as a goal, and the current liquidity provisions though directed at the economic crash from the pandemic are exactly what the bank would prescribe for chronically weak prices.

New economic and rate projections will be issued on Wednesday. The bank did not release its March estimates as the scheduled FOMC meeting was superseded by the two emergency rate cuts on March 3 and 15.

Mr. Powell may mention inflation and the projections will no doubt show it moving higher over time but price changes will remain, as they have been for a decade, the backwaters of Fed policy.

Policy is very unlikely to change in the near future as the bank waits for the recovery to take hold.

Conclusion and the dollar

The precipitous drop in consumer prices in March and April was a direct consequence of the lockdown induced plunge in consumption. The incipient recovery will return both to their normal positive aspect though the amount of the rise in price is largely dependent on the strength of the consumption gain.

The Dollar has given up all of its risk-premium in all of the major pairs though it has not moved very far into the pre-pandemic ranges. Its current weakness is not a trend and is due to the waning momentum of its recent decline but with inflation concerns on the far back-burner at the Fed no result for CPI is likely to impact the greenback.

Competitive economic comparison is next on the currency agenda but it may take several weeks until sufficient data is accumulated to determine whether the US, Europe, Japan or elsewhere are recovering the fastest.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.