US Conference Board Consumer Confidence: From stability to improvement?

- Confidence edges higher in May after six-year low in second sign of consumer stability.

- Economy headed for two consecutive negative quarters.

- Equities rally sharply, Treasury yields rose and the dollar fell on vaccine hopes.

- New home sales tick higher April, belying predictions for a collapse.

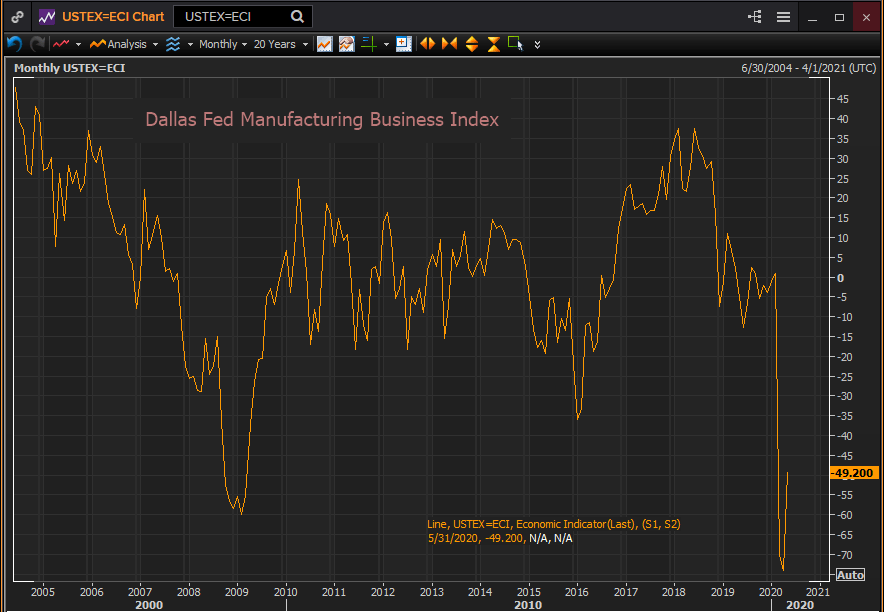

- Dallas Fed manufacturing index rises from record low.

- Dollar risk premium subsides as market panic fades.

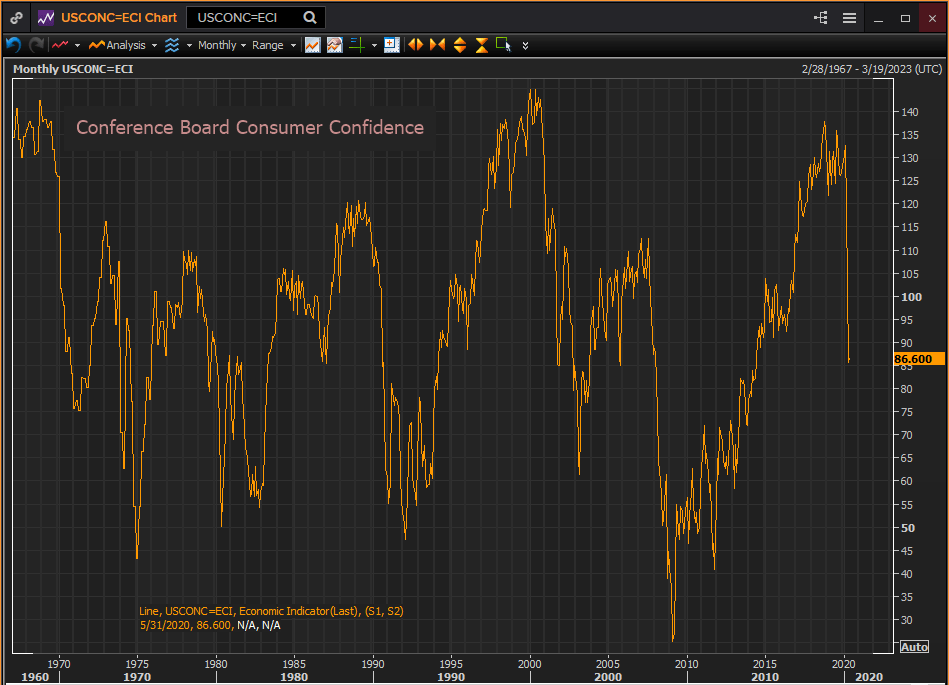

American consumer confidence stabilized in May after plunging for two months as the forced layoff of nearly a quarter of the workforce and widespread business closures have thrown the economy into chaos and recession.

The Conference Board reported its long-running confidence index edged higher to 86.6 in May from April’s 85.7 score. The index which has been tracking US consumer attitudes since 1967 had fallen from 132.6 in February, the sharpest decline the series history.

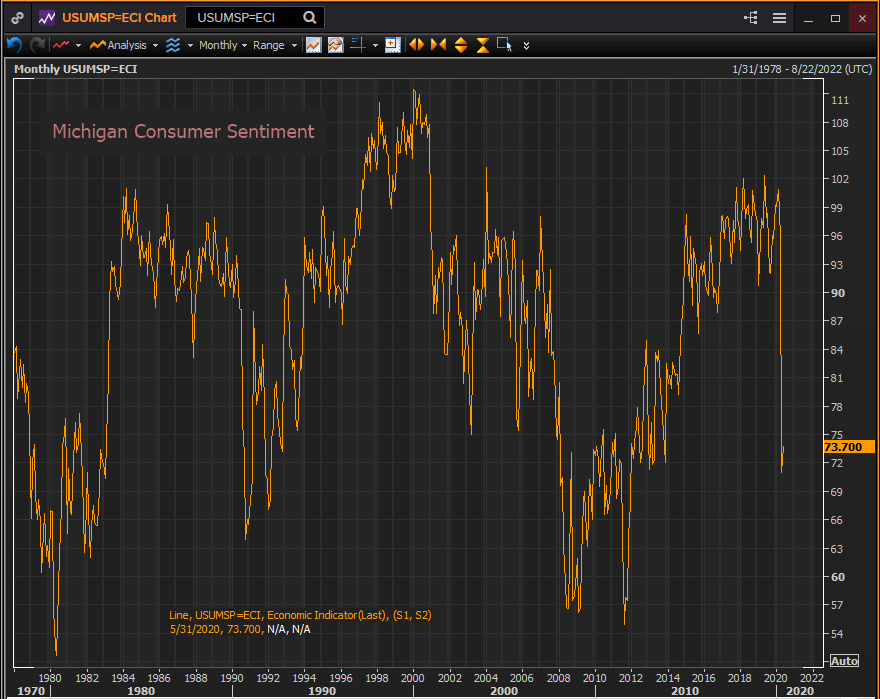

This confirms the Michigan survey of two weeks ago that saw its sentiment index rise to 73.7 this month from 71.8 after suffering a similar two month plummet.

Almost 40 million people have filed for unemployment insurance in the past nine weeks and non-farm payrolls tumbled 20 million in April, by a wide margin the greatest and most rapid loss of jobs in the nation’s history.

Shuttered by the virus

State governments in most of the country ordered ‘non-essential’ businesses closed and instituted draconian social-distancing restrictions in March as part of an effort to slow the spread coronavirus.

All states have rescinded at least some of their emergency regulations. Three states that were the first to remove business shutdown orders, Georgia, Florida and Texas have not had an appreciable increase in virus case or hospitalization rates. Most others states are expected to follow their lead in the next several weeks.

US GDP

The cascading shutdowns in March precipitated a collapse in GDP that was severe enough to push the first quarter, which had been expanding at a 2.7% annualized pace, into a 4.8% contraction. Estimates for the second quarter with much of the economy closed for two months, are running at -30% or worse with the Atlanta Fed GDPNow forecast at -41.9% on May 19. Even if much of the nation reopens in June, a negative quarter, and a recession by the traditional measure of two contracting quarters in a row, is almost sure to be met.

Signs of improvement

There were two other tentative signs on Tuesday that the bottom may be near. The Dallas Fed Manufacturing Business Index rose to -49.2 in May from its all-time low of -74 in April. New home sales in April, which had been projected to deepen the March 13.7% tumble at -21.7%, rose instead 0.6% to a 623,000 annual pace from the prior 619,000.

The Conference Board survey’s present situation index that gauges current business and labor market conditions, dropped to 71.1 in May from April’s 73. This measure has fallen nearly 100 points since as the pandemic panic took over the US economy.

The expectations index based on consumers short term outlook for income, business and job market conditions rose to 96.9 in May from 94.3 and the index of whether jobs are plentiful or hard to get rose to -10.4 in May from -15.7 in April.

“Following two months of rapid decline, the free-fall in Confidence stopped in May,” noted Lynn Franco, Senior Director of Economic Indicators at The Conference Board in the accompanying statement.

“The severe and widespread impact of COVID-19 has been mostly reflected in the Present Situation Index, which has plummeted nearly 100 points since the onset of the pandemic. Short-term expectations moderately increased as the gradual re-opening of the economy helped improve consumers’ spirits.”

Markets reflect recovery

Equities surged with the Dow adding 2.17%, 529.95 points to 24,995.11. The S&P 500 climbed 1.23%, 36.23 points to 2,991.77. West Texas Intermediate, (WTI, CLc1) slipped $0.25 to $34.1.

Treasury yields rose with the 10-year gaining four basis points from Friday’s to 0.695% and the 2-year less than a point to 0.174%.

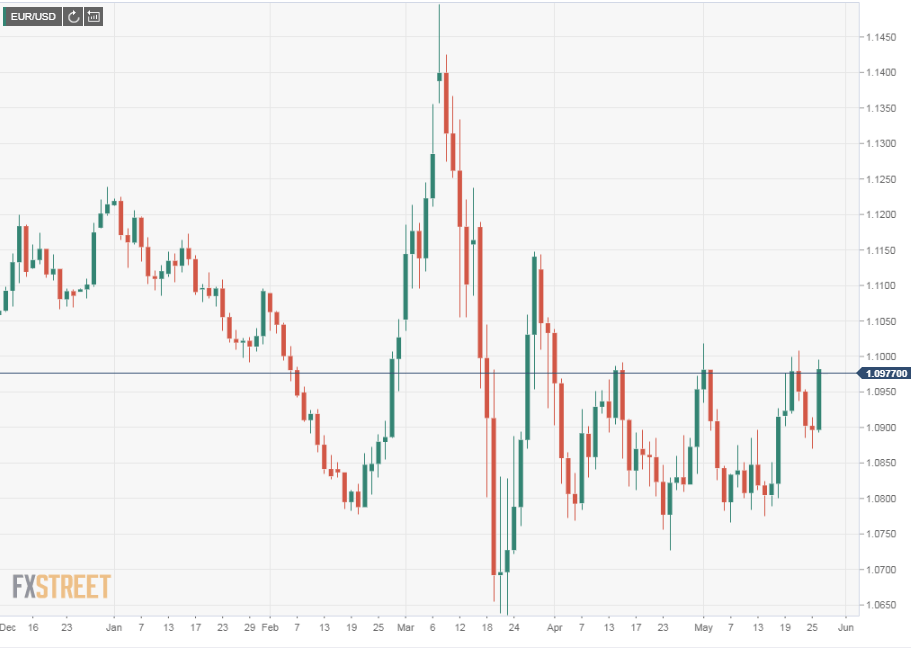

The dollar lost ground against all the majors on the day with the losses open to close as follows: Euro-1.0897-1.0982; yen 107.71-107.40; 1.2190; aussie 0.6545-0.6648; Canada 1.3982-1.3757; 0.6104-0.6199.

The combination of optimistic news on several vaccines, the better than forecast US data and the powerful equity rally prompted by the first two, helped to convince traders that the remaining pandemic risk premium in the US dollar is fast becoming an anachronism.

Unless there is a profound and unexpected revival in viral infection and fatality percentages and the market recovery from the pandemic panic is well underway.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.