US 10-Year Treasury Auction: Interest rates return to center stage

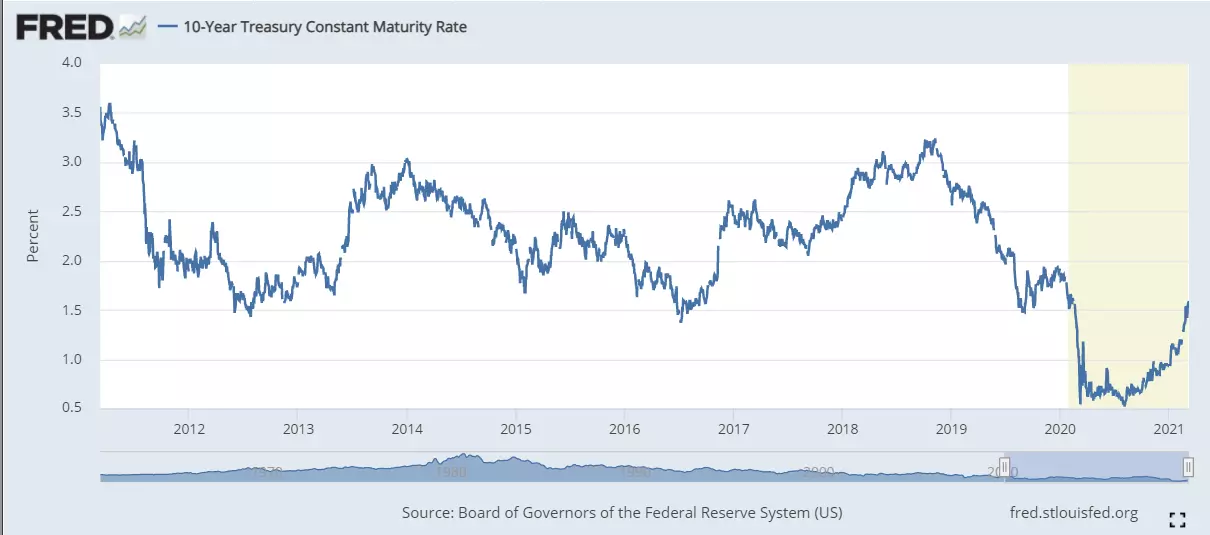

- 10-year yield at 1.54% is up 70% this year, 300% in seven months.

- Economic growth and inflation prospects driving credit markets.

- Federal Reserve expects temporary inflation and unaffected economic expansion.

- Yield on the 10-year Treasury remains at extreme low of historical range.

- Dollar is riding the yield surge, both are headed higher.

After almost a year in the pandemic dungeon, Treasury yields have a qualified parole.

The 10-year Treasury reached 1.613% on Monday its highest since last March before closing just below 1.6%.

Market expectations are high for a burst of US economic growth in the first half of the year. The first signs of inflation are visible and conditions seem ripe for its return. The Federal Reserve has signaled that, at least for the time being and at current levels, it is not concerned that rising interest rates will choke off growth. Enormous US federal deficits, including the latest $1.9 trillion spending package, funded entirely by debt, have placed an unprecedented amount of issuance into the global financial system.

All these are indications that Treasury rates, except for the short end of the curve, pinned by the Fed, will continue to move higher.

10-year Treasury auction

Into that mix Wednesday's auction of 10-year bonds could put a seal on the direction for interest rates and on the willingness of investors to absorb the burgeoning American debt.

The chief question is for the major financial institutions that participate in Treasury auctions. Are yields sufficient given the risks inherent in the economy? With $414 billion of Treasury supply in March, almost twice the previous record, the answer will determine the immediate future for bond prices and rates. Treasury prices move inversely to yield.

Until last month markets had taken in the proceeds of several large auctions without driving rates appreciably higher.

But the 7-year note auction on February 25 had the worst participation since the US Treasury reintroduced the debenture in 2009. The highest return of 1.212%, tailed by 4.2 basis points, was the worst in the auction's history. The tail is the term for the gap between the yield before the auction and the highest return resulting from the auction.

Immediately after that auction the 10-year yield broke above 1.6% in intra-day pricing for the first time since last February.

US economic growth

The US economy, freed from pandemic restrictions and fostered by massive fiscal stimulus and individual grants, is expected to explode into expansion in the first and second quarters.

Payrolls have resumed growth, adding 166,000 jobs in January and 379,000 in February.

Consumers signaled their potential cooperation with a 5.3% burst of spending in January Retail Sales. The ostensible reason was the $600 stipend in the December stimulus package but that was likely enabled by declining pandemic cases and the reviving job market.

February Retail Sales are due on March 16 and are forecast to slip 0.4%. If spending is positive, it will be another sign that the US consumer is ready to fund the expansion.

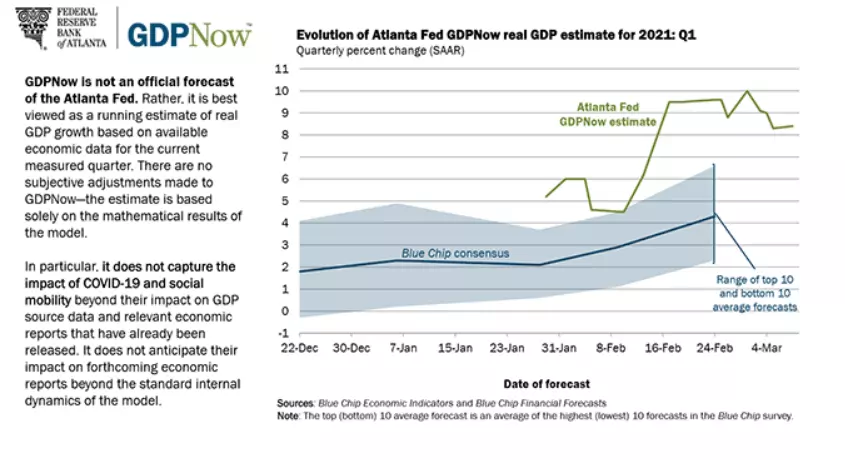

The current Atlanta Fed GDPNow estimate for first quarter annualized GDP is 8.4%. The next update is after February Retail Sales.

Finally, even Fed Chairman Jerome Powell noted in Congressional testimony that the economy might expand at 6% this year.

Inflation

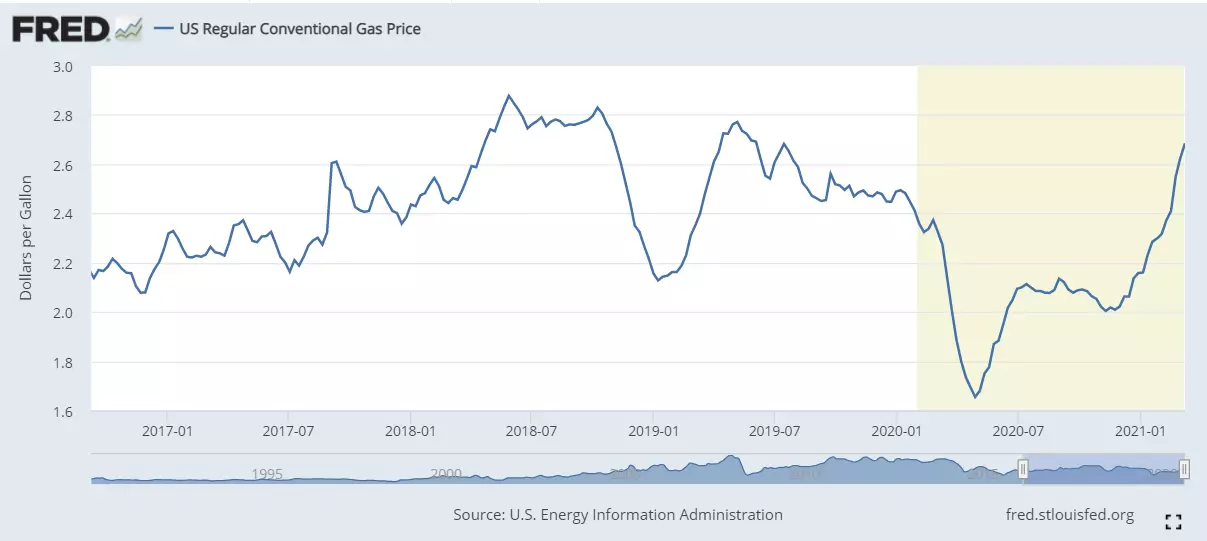

The Producer Price Index jumped 1.3% in January driving the annual rate to 1.7% from 0.8% in December. Monetary conditions at their most accommodative since the financial crisis. The Federal Reserve rate projections have the fed fund at its current 0.25% upper target through the end of 2023. Annual multi-trillion dollar federal deficits have placed more money into the economy than at any time in US history. Gasoline prices have also risen sharply, 34% to $2.68 from November 9 to March 8.

Overhanging unemployment should deter immediate wage increases but that could well change by the third or fourth quarter particularly in specific fields like construction where demand for homes is running above housing bubble levels. Demand for consumer goods coming against supply constrictions lingering from the pandemic might also push prices higher.

While price increases have not yet shown in the Consumer Price Index which was 1.4% on the year in January, it is expected to climb to 1.7% in February.

Federal Reserve

Chairman Jerome Powell has said that the bank expects any rise in inflation to be temporary, a product of the base effect from the collapse of prices in the spring.

Inflation averaging, the Fed's new price management policy intends to tolerate gains above target for periods long enough to produce the 2% average. Since core PCE inflation has only rarely been above target in the past decade the FOMC can obviate a potential inflation trigger simply by lengthening the averaging period.

Interest rates, specifically the benchmark 10-year yield are at the extreme lower end of their historical range. The all-time low was just over six months ago on August 4 at 0.515%.

That is likely the source of Mr Powell's expressed confidence that the US economy can tolerate an orderly ascent of rates without sacrificing economic growth.

A final piece of logic may help to define the Fed's seeming insouciance in the face of rapidly rising Treasury and commercial rates.

The Fed is committed to providing maximum support to the economic recovery and to keeping the short end of the yield curve and the fed funds rate low as long as necessary to achieve that goal. Yet the governors know the conditions for inflation are quickly amassing. By letting the longer side of the curve rise the governors can hopefully brake any inflationary expectations without surrendering their promises.

Conclusion

Rising interest rates in the US are an economic function. The credit markets are responding to modest improvements in economic data and to the enormous potential for US expansion this year. The signs of the gathering rush are plentiful.

The recovery of the American economy and employment will not be deterred by 10-year rates rising toward 2%. Traders and investors know this. The equity, credit and currencies markets have already rendered their judgment.

Higher interest rates are a sign of economic health.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.