United States: The Fed’s discount window now more attractive for smaller banks

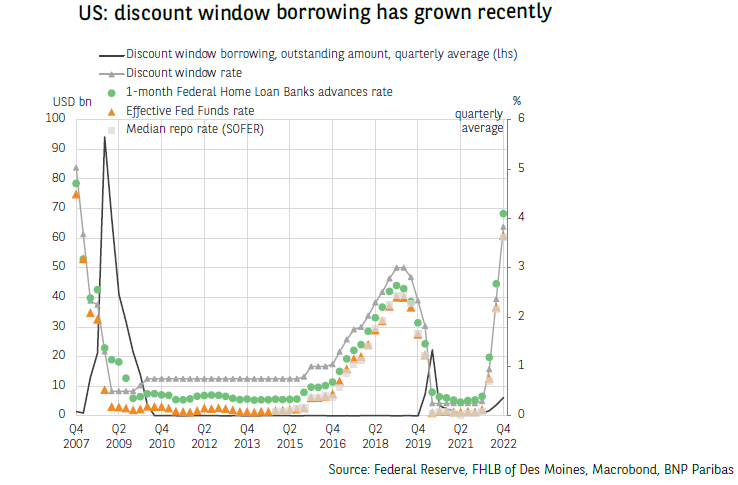

The drawdowns of depository institutions from the US Federal Reserve’s (Fed) discount window have intensified over the past year. Their outstandings amounted to USD 4.6 billion on 18 January, certainly far from the USD 110 billion borrowed at the height of the 2008 financial crisis, but well above the USD 360 million borrowed on average for 15 years1. However, no major financial stress or central bank money shortage seems to justify this. The list of borrowers – which will only be disclosed in two years’ time – should mainly include small institutions, which are distanced from the risk of stigma associated with the use of this window. We see two main reasons for this.

The first is that the reduction in the Fed’s balance sheet has significantly reduced the liquid assets (reserves) and stable resources (deposits) of smaller banks. Their reserve-to-asset ratio is now at a level comparable to that of the last round of quantitative easing (and the massive central bank liquidity injection) at 6.5% (Fed H.8 data), while their loan-to-deposit ratio has risen by 10 percentage points in just one year.

The second reason is the relaxation of the scheme in March 2020 by the Fed. On the one hand, the Fed removed the penalty applied, by fixing the discount rate at the upper limit of the target rate for federal funds2 and, on the other hand, extended the maturity of loans3. Since the beginning of monetary tightening in March 2022, so-called “ emergency” loans from the Fed (4.5% on 18 January 2023) have thus become less expensive than collateralized loans from Federal Home Loan Banks (4.59% overnight, 4.54% at 1 week, 4.68% at 1 month and 4.95% at 3 months).

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.