Ukraine war to slash Eurozone 2022 growth, boost inflation: EU

USDINR 77.74 ▲ 0.39%.

EUR/USD 1.0432 ▲ 0.01%.

GBP/USD 1.2337 ▲ 0.16%.

India 10-Year Bond Yield 7.378 ▲ 0.82%.

US 10-Year Bond Yield 2.917 ▲ 1.31%.

ADXY 102.59 ▲ 0.03%.

Brent Oil 114.02 ▼ 0.19%.

Gold 1,822.56 ▲ 0.47%.

NIFTY 50 15,953.00 ▲ 0.70%.

Global developments

In a sign of how severely lockdowns in China have hit consumption, retail sales fell 11.1% yoy against expectations of a drop of 6.1%. The unemployment rate in China's 31 largest cities rose to a new high of 6.7% in April. With cases dropping, Shanghai will be gradually lifting restrictions and is likely to return to normalcy by mid-June.

Sweden and Finland have announced that they want to join NATO. This is likely to result in an escalation in geopolitical tensions in Europe as Finland shares a long border with Russia. Russia could retaliate by halting the flow of natural gas to Finland.

Price action across assets

The S&P500 and Nasdaq ended flat, giving up gains towards the end of the session, US yields have eased a bit with a 10y yield now at 2.90%. Crude prices have risen as China is looking to ease lockdown restrictions which would boost demand. Brent has climbed to USD 114 per barrel. The US Dollar has weakened against majors as most Fed members seem to be comfortable with 50bps hikes. 75bps hikes seem to be off the table as of now. The Euro has bounced back to 1.0440 from Friday's lows around 1.0360. The pound has risen to 1.2340. Commodity currencies have seen a massive recovery with the Australian Dollar popping up above 70 cents to the Dollar in anticipation of China's demand returning back.

China's covid controls will impact foreign investment for years - U.S. lobby.

Domestic developments

India has banned exports of wheat to cool off domestic prices. Government procurement was falling short due to high international prices. LIC's stock would list on bourses today.

USD/INR

The rupee had ended at 77.43 on Friday. Yesterday was a Rupee holiday. Rupee however weakened in offshore trading yesterday with NDF implied spot having got dealt at 77.85 as well.

The rupee is likely to underperform on higher crude prices today.

The forward curve has been under pressure with the 1y forward yield dropping to 3.68% on Friday.

Bonds and rates

The gsec auction on Friday had gone through smoothly. We may see bonds come under pressure on rise in crude prices. The yield on the benchmark 10y had ended at 7.32% on Friday.

Equities

The stock markets were open yesterday. After a strong opening, the Nifty gave up gains during the session to end 0.4% higher at 15842. Cement stocks dragged the index lower. Competing Cement stocks fell on the announcement of the Adani-Holcim deal on fears of loss of market share.

Strategy

Exporters are advised to cover on upticks towards 77.80. Importers are suggested to cover on dips towards 76.50. The 3M range for USDINR is 75.50–78.30 and the 6M range is 75.00–78.90.

Asian stocks up, but inflation and China's covid outbreaks remain concerning.

FX outlook of the day

USD/INR (Spot: 77.74)

The Indian rupee settled at 77.43 levels in the previous session. Yesterday was a Rupee holiday. The rupee however weakened in offshore trading yesterday with NDF implied spot having got dealt at 77.85 as well. Crude prices have risen as China is looking to ease lockdown restrictions which would boost demand. The surge in crude price is expected to keep the rupee under pressure. The US dollar has weakened against majors as most Fed members seem to be comfortable with 50bps hikes. 75bps hikes seem to be off the table as of now. We may see bonds come under pressure on rising crude prices. The pair is expected to trade with an upside bias. The intraday range for the pair is expected to be 77.50-77.90

EUR/USD (Spot: 1.0438)

The EURUSD pair is displaying back and forth moves in a tight range after a modest upside move from a low of 1.0350 last week. A minor improvement in the risk appetite of the market participants has supported the shared currency bulls. Risky assets were beaten hard by investors on souring market mood for a tad higher time period. While the euro docket will report the Gross Domestic Product numbers. The yearly and quarterly figures are expected to remain unchanged at 5% and 0.2% respectively. Sweden and Finland have announced that they want to join NATO. This is likely to result in an escalation in geopolitical tensions in Europe as Finland shares a long border with Russia. This news has also affected the euro pricing. The pair is expected to trade with a sideways bias. The intraday range for the pair is expected to be 1.0400-1.0480.

GBP/USD (Spot: 1.2333)

The GBPUSD grinds higher past 1.2300, keeping the two-day recovery moves from the lowest levels since mid-2020, as the market participants await the UK’s jobs report, as well as key Brexit updates, for fresh impulse. A softer USD and broad risk-on mood helped the pair to recover from the latest losses ahead of the key UK data, surrounding the Northern Ireland Protocol. UK PM Boris Johnson is all set to alter part of the NIP by citing it as an “insurance” in case of the European Union’s failure to respect other terms. Johnson’s move is in contrast to the bloc’s warning of cutting trade and will be observed closely. The pair is expected to trade with a sideways bias. The intraday range for the pair is expected to be 1.2290-1.2370.

USD/JPY (Spot: 129.38)

The USDJPY refreshes its intraday high to 129.45 as upbeat sentiment joins firmer Treasury yields to please buyers after a lackluster start to the week. The quote’s latest run-up could be linked to the positive headlines from China, as well as in anticipation of US Retail Sales for April and a speech from the Fed Chairman Jerome Powell. The Japanese policymaker recently said, in FY 2025/26, the primary budget surplus aim must be met. Elsewhere, Shanghai conveyed plans to end the covid-linked lockdown after the third consecutive day of zero coronavirus cases outside the quarantine area, which in turn favors the market sentiment and propels the USDJPY prices. The pair is expected to trade with a neutral to bullish bias. The intraday range for the pair is expected to be 129.00- 129.70.

ECB to hike deposit rate 25 bps in July, ditch negative rates by end-September: Reuters poll.

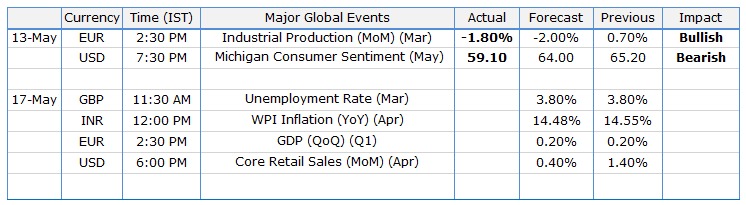

Economic calendar

Author

Abhishek Goenka

IFA Global

Mr. Abhishek Goenka is the Founder and CEO of IFA Global. He pilots the IFA Global strategic direction with a focus on relentlessly improving the existing offerings while constantly searching for the next generation of business excellence.