UK labor market Preview: Strength confirmed with policy response already delivered

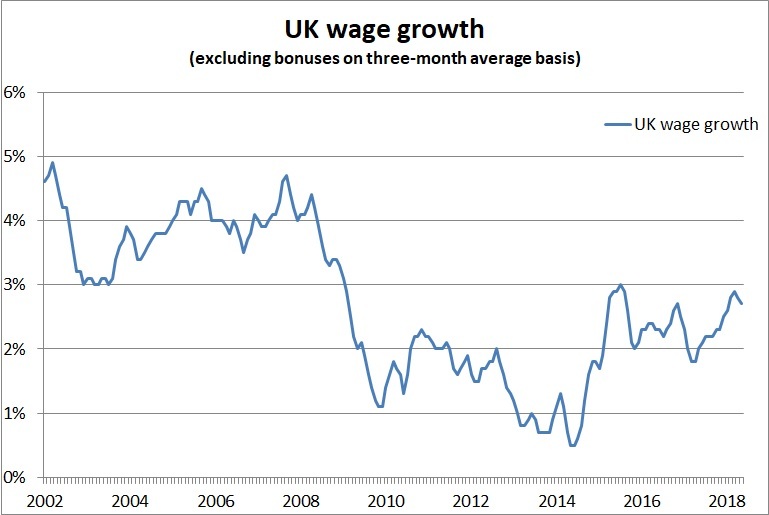

- The UK labor market is expected to deliver another proof of its strength with the unemployment rate stuck to a four-decade low of 4.2% and wage growth of 2.7% y/y excluding bonuses.

- The UK claimant count is seen rising 3.8K in July, the lowest in 2 months.

- The UK labor market served as the main reason for the Bank of England to hike rates in August and now it is unlikely to alter the ultra-dovish monetary policy outlook.

The strength of the UK labor market was the main argument behind the Bank of England raising the Bank rate in August and those trends are set to be confirmed also in July reading. The UK wages excluding bonuses are expected to rise 2.7% y/y in three months ending in June while wages with bonuses are seen rising 2.5% y/y, the report from the Office for National Statistics is set to disclose on Tuesday, August 14 at 8:30 GMT.

The claimant count representing the number of people seeking the unemployment benefits in the reporting month is expected to rise by 3.8K in July, down from 7.8K reported in June, the lowest since May when it fell -7.7K, confirming strong UK labor market condition that keeps the unemployment rate stuck to a four-decade low.

In the August Inflation Report, the Bank of England said that the UK labor market continued to tighten and the strength of the UK labor market served as a major justification for the 25 basis points rate hike with the unanimous vote from all Monetary Policy Committee (MPC) members.

“ Most indicators of pay growth had picked up over the past year and the labor market remained tight, suggesting that domestic cost pressures would continue to firm gradually,” the Bank of England wrote in August Inflation Report.

While the strength of the UK labor market is positive in terms of the outlook for inflation, the labor market tightness is a thret to the inflation target as the labor market tightness is expected to push up pay growth slightly further in coming years.

In terms of the monetary policy outlook, the Bank of England delivered a very dovish outlook. The August Inflation Report projections were conditioned on the Bank rate rising from 0.5% before this month's meeting to 1.0% by Q1 2020 and then edging higher to 1.1% by Q3 2021 and the outgoing MPC member Ian McCafferty confirmed that the market expectations for a couple of rate hikes during the next two years are acceptable.

Although Ian McCafferty is an external Monetary Policy Committee member who is leaving the MPC at the end of this August, his hawkish views are well known as he was voting for a rate hike since March until the Bank of England raised the Bank rate to 0.75% last week delivering dovish monetary policy outlook.

The outcome of the UK labor market report, even if overly positive, is unlikely to alter the monetary policy outlook, but it might support Sterling that has been under immense selling pressure recently stemming from both a no-deal Brexit uncertainties and the external shocks related to Turkey-related Risk-off market sentiment.

UK wage growth excluding bonuses

Author

Mario Blascak, PhD

Independent Analyst

Dr. Mário Blaščák worked in professional finance and banking for 15 years before moving to journalism. While working for Austrian and German banks, he specialized in covering markets and macroeconomics.