UK growth to rebound through 2025 after a sluggish January

Don’t be distracted by volatility in the monthly GDP numbers, because despite a surprise fall in January’s economic output, higher government spending should lead to reasonable growth through 2025. Whether that’s enough to avert tough decisions for the Treasury, we’re not so sure.

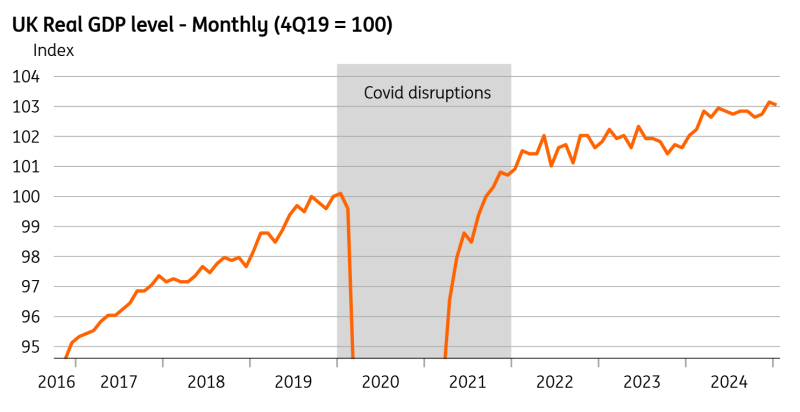

The UK economy got off to a sluggish start in 2025, judging by the 0.1% fall in output through January. Manufacturing has had a particularly bad run, having grown in just one of the past five months, driven in large part by weakness in car production. Outside of that, it’s hard to pick out many consistent trends from the past few months and the simple reality is these monthly numbers are unhelpfully volatile. January’s fall only partially offsets a very healthy December for overall economic growth (+0.4%). And that strong end to the fourth quarter sets up a decent base for overall first quarter growth, which we expect at 0.3%.

In short, January’s weakness shouldn’t detract from what is likely to be a fairly reasonable year for UK growth. The Treasury is dramatically boosting day-to-day spending this year, even if some of that will get pared back in the Spring Statement later this month. Given much of that spending boost will land in wages, the impact on the wider economy should be discernable in the GDP numbers this year.

January's fall in monthly GDP only partially offset a strong December

Source: Macrobond

The problem for the Treasury is that its independent forecaster, the Office for Budget Responsibility, has been far too optimistic on 2025 growth. Its 2% forecast looked wildly optimistic even when it was announced back in October. The truth is likely to be more like half that.

That downward revision, in and of itself, shouldn’t move the dial too much for Chancellor Rachel Reeves as she tries to rebuild the “fiscal headroom” that has been eradicated by higher market rates. But that is contingent on the OBR making no further downward revisions to growth in future years, which are more heavily linked to its view on longer-term trends for productivity.

The difficulty for the Treasury is that its recent flurry of announcements, from planning reform to airport expansion, are unlikely to convince the OBR to upgrade those longer-term predictions. As we discussed in a separate article, this partly explains why the government is looking more carefully at changes to the UK’s economic relationship with the EU. Closer alignment would almost certainly convince the OBR to boost its forecasts, though we're less convinced this would make a decisive difference to the outlook for the public finances.

For the Bank of England, the recent run of data, including today’s weakness in January GDP, is unlikely to have shifted the dial materially ahead of its meeting next week. In general, the committee seems to be getting a little more cautious, in light of sticky wage growth and services inflation. The major question mark, both for the BoE and the growth outlook generally, is what impact the big tax hike on employers next month will have on the jobs market, which has already cooled significantly over recent months. A spike in layoffs, which so far hasn’t happened, could be a game changer for the 2025 growth outlook and for monetary policy.

For now, we expect the Bank to continue its quarterly pace of cuts, with moves in May, August and November this year.

Read the original analysis: UK growth to rebound through 2025 after a sluggish January

Author

James Smith

ING Economic and Financial Analysis

James is a Developed Market economist, with primary responsibility for coverage of the UK economy and the Bank of England. As part of the wider team in London, he also spends time looking at the US economy, the Fed, Brexit and Trump's policies.