UK CPI Preview: With inflation decelerating in favor of real wages, Sterling will be supported

- The UK headline inflation is expected to have decelerated to 2.4% y/y in August while core inflation slow to 1.8% y/y.

- The UK Inflation outpaces the nominal UK wage growth by 0.2% y/y when bonuses are included and by 0.4% y/y excluding bonuses.

- Decelerating inflation should join the wave of Brexit positive headlines of late in support for the Sterling.

- The Bank of England hiked the Bank rate at the beginning of August expecting the external cost pressures like Sterling’s past depreciation and higher energy prices easing while domestic factors like wage growth taking over.

The headline inflation is expected to have decelerated to 2.4% y/y in August, from 2.5% y/y in July while core inflation stripping the consumer basket off food and energy prices is seen decelerating to 1.9% y/y from 2.0% in July, the Office for National Statistics is expected to announce on Wednesday, September 19 at 8:30 GMT.

The deceleration of the UK inflation marks the positive macroeconomic development in the UK of late with August labor market reporting 2.9% y/y increase in the regular pay (excluding bonuses) and 2.6% increase in total pay (including bonuses), that should see the real total and regular pay adjusted for inflation rise 0.2% y/y and 0.4% y/y respectively.

With the UK inflation decelerating in support of rising real wages, Sterling should be supported on the FX market as GBP bulls benefit from positive Brexit news of late making Brexit deal looking achievable in a foreseeable time of next 5-7 weeks.

While inflation in July ticked up to 2.5% in July helping the Bank of England to justify its August decision to hike interest rates, the outlook for further monetary policy remained dovish as central bank already said further rate hikes will only be limited and gradual.

The Bank of England expects inflation to moderate in coming months, as the previous effect of Sterling´s depreciation is fading away and domestic price pressures are taking over with the UK labor market tightness being the primary factor. Recent data relating to companies' costs and trade prices suggest it inflation might remain stubbornly high.

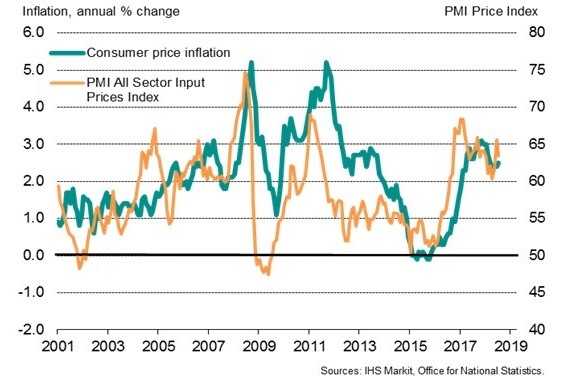

The IHS/Markit Economics reported that the PMI survey gauge of average prices charged by companies for their goods and services remained elevated by recent historical standards in July, indicating inflation running at just under 3%.

In order to protect the margins, companies in the UK are likely to pass higher costs onto customers increasing their selling prices, the effect related to a weaker Pound and higher import prices stemming from the recent wave of Sterling´s depreciation from 2018 high of 1.4377 to 1.2766 low in the middle of August.

The UK PMI input prices and UK inflation

Author

Mario Blascak, PhD

Independent Analyst

Dr. Mário Blaščák worked in professional finance and banking for 15 years before moving to journalism. While working for Austrian and German banks, he specialized in covering markets and macroeconomics.