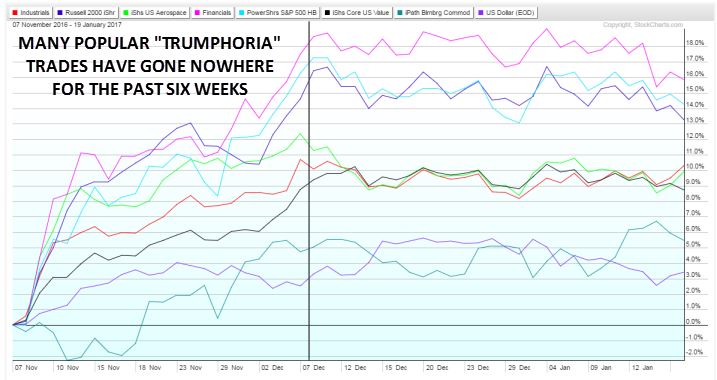

"Trumpflation" is still thriving, but "Trumphoria" is fading away

Looking back to the market's reaction to the US election, it's difficult to find a comparable period of euphoria over the last couple of years. Seemingly every risk asset rallied, with the biggest perceived "winners" (industrial/defense/financial/small cap/high-beta/value stocks, commodities, and of course, the US dollar) exploding higher on expectations of broad tax cuts, massive infrastructure plans, and the reduction of onerous regulations.

"Hindsight is 20/20"

With the benefit of hindsight and a bit of perspective, it's starting to look like investors' were wearing their rose-colored glasses when making some of these projections. In some ways, traders were projecting only their biggest hopes onto Donald Trump's vague (often 140-character) proclamations, while pricing in none of the potential downside from having a bombastic political novice running the planet's largest economy.

In particular, investors' hopes for an imminent, massive fiscal stimulus plan appear to be misplaced. Since his middle-of-the-night victory speech, Trump has hardly mentioned infrastructure spending or reforming the tax code, preferring to focus on trade issues. A new infrastructure plan could still be in the offing, but at least as of writing on the eve of the inauguration, all economic issues will take a back seat to trade.

So what's that mean for markets?

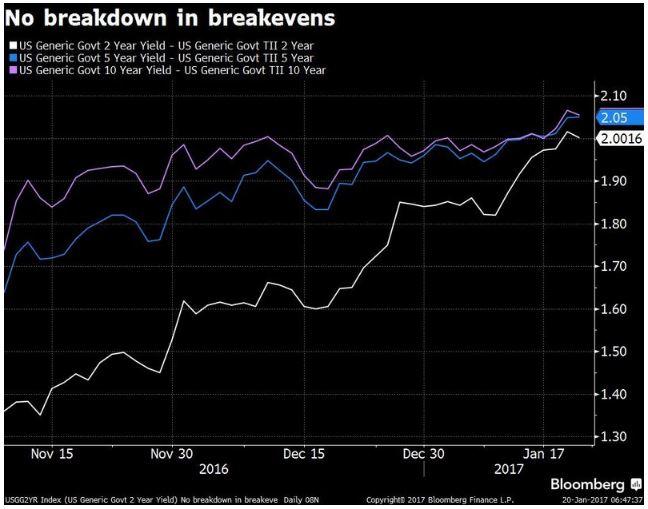

Inevitably, traders will have to adapt to the new administration's policy's as they come, but there are a couple of post-election market moves that are poised to excel regardless of which campaign promises President Trump prioritizes first. Notably, whether he focuses on trade, infrastructure, cutting taxes, or reducing regulation, inflation is likely to rise. As the chart below shows, breakeven inflation rates have continued to rise consistently throughout the 10 weeks since the US election:

These measures, which just show the difference in yield between nominal Treasury yields and TIPS yields, show the market's expectations for inflation over the coming 2, 5, and 10 years respectfully. The biggest move by far has been in the 2-year breakeven rate, which has risen from less than 1.4% before the election to above 2% today.

The impact of higher short-term inflation, especially if it manifests as a result of trade protectionism, is more nuanced that the "Trumphoria" trade that emerged in November. Obvious beneficiaries of rising short-term inflation include TIPS, commodities (including gold), and gold miners. To the extent that this theme flattens the yield curve, financial stocks will face a headwind. Meanwhile, the outlook for the US dollar is difficult to divine at this point: rising inflation could certainly prompt a more aggressive rate hike path for the Federal Reserve, but if the rising prices are a result of trade protectionism, slower economic growth could moderate the Fed's hawkish tendencies.

Author

Matt Weller, CFA, CMT

Faraday Research

Matthew is a former Senior Market Analyst at Forex.com whose research is regularly quoted in The Wall Street Journal, Bloomberg and Reuters. Based in the US, Matthew provides live trading recommendations during US market hours, c