There's a new sheriff in town. Will he act differently than the old sheriff?

There’s a new sheriff in town over at the Federal Reserve. He sounds a lot different than the old sheriff, but one would be wise to remember that Kevin Warsh is enforcing the same laws in the same town as Jerome Powell did.

While it sounded a lot different, the first FOMC meeting of the Warsh era looked exactly like the previous meeting. The committee held interest rates steady at between 3.5 and 3.75 percent, and it hinted that there could be a rate hike before the end of the year.

There was similar hawkishness in the last meeting; however, the committee seemed to be more unified in their views. The vote to hold rates steady was unanimous, and most members seem to be willing to entertain the possibility of a hike.

Hinting at Warsh’s communication style, the official FOMC statement was much shorter at just 130 words than those released during the Powell era.

Powell addressed the brevity of the statement during his presser.

“It’s a bit shorter, a bit simpler, and it dispenses with some older language. That statement just gives you the facts, as best we can judge it.”

The statement emphatically asserted that the Fed “will deliver price stability,” hinting at Warsh’s commitment to fight inflation. However, it erased any clue as to what the Fed might do next from a policy standpoint.

The new Fed chair reiterated this messaging during his press conference. He reminded listeners that “persistently high prices are a burden for the American people,” and assured them, “Members of the [Federal Open Market Committee] are unambiguous and unanimous: this committee will deliver price stability.”

Apart from the aforementioned assurances, Warsh gave very little indication about the future trajectory of monetary policy. He even refused to submit data for the new dot-plot projections. During his press conference, Warsh indicated that he’s not a big fan of “forward guidance,” a staple of the Powell regime.

“I did not submit a dot for me. It’s not helpful in the conduct of policy. I suspect by year-end, as I mentioned in my opening statements, there’ll be a review about communication broadly, press conferences, dots, meetings, and the like, transcripts, minutes. This will be part of that. I don’t want to prejudge the outcomes there, but I’m pretty open-minded about what they could be.”

In practice, this means we could see more “surprise moves” by the central bank in the months ahead. Unlike Powell, Warsh seems much less inclined to telegraph what the Fed might do next.

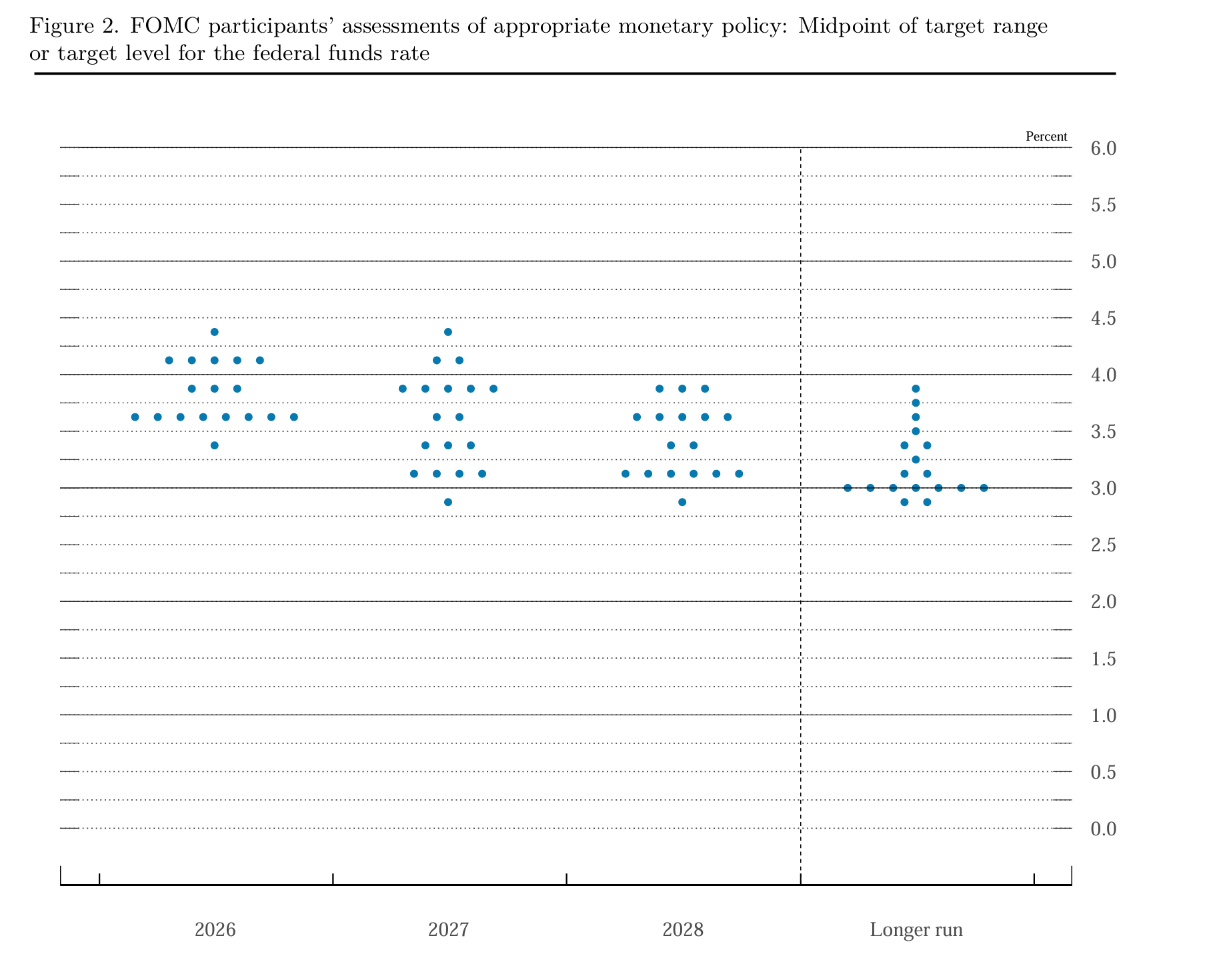

The new dot plot erased any indication of a possible rate cut this year and hinted at the possibility of a rate hike. The median rate projection was 3.8 percent by the end of the year, up from 3.4 percent in the last plot.

Warsh is right about one thing. These dot plots are pretty useless as a forecasting tool. Fund manager David Hay analyzed past dot plots and found the FOMC only got interest rate projections right 37 percent of the time. And as Hay pointed out, “They control interest rates!”

For instance, in March 2021, the FOMC projected that the interest rate would still be zero in 2022. The actual 2022 rate was 1.75 percent. And in 2023, the vast majority of FOMC members thought the rate would still be at zero. The actual rate was over 5 percent.

Talk is cheap; What will the Fed do?

Cleaning up messaging is one thing. Getting the job done is something else altogether.

It’s easy for Warsh to insist that the Fed will bring price inflation back down to the 2 percent target. It’s easy to say, “We’ll hike rates.” Delivering on the promise won’t prove as easy.

It’s important to remember that Warsh is operating in the same environment as Powell was. The Debt Black Hole still looms large, making rate hikes a dangerous prospect. In fact, holding rates steady may be enough to pop the debt bubble.

The ugly truth is that debt-riddled economies don’t function very well in higher-interest-rate environments. It won’t take much to pop the debt bubble, and the central bankers at the Fed and the markets speculating about their next move seem to be ignoring this vital piece of the puzzle.

In other words, the Fed is still in a Catch-22. So, what Warsh says isn’t relevant. The central bankers are limited in what they can do by the massive Debt Black Hole dominating society. They can inject the rate hike medicine and hope it doesn’t interact with the Debt Black Hole and hope it doesn’t kill the economy, or they can feed the Debt Black Hole with lower rates (and more inflation).

Speculation that the Fed will hike rates has put significant downward pressure on gold and silver prices over the last two months. Conventional wisdom holds that higher rates are bearish for precious metals. But there is no guarantee that they will really be able to cut -- no matter what Warsh may want to do. And if they do, there is a high likelihood it will precipitate a recession and/or a financial crisis.

The fact that the Fed apparently plans to continue running quantitative easing despite the talk about inflation worries reveals the difficulty of the path ahead for the central bankers at the Fed.

In the official statement, the FOMC “reaffirmed its policy of maintaining ample reserves in the banking system.” This is code for keeping the balance sheet at roughly the same level.

Warsh has indicated a desire to drastically reduce the balance sheet, but there is no way the Fed can dump its Treasuries in the open market without driving yields even higher. High interest rates are already stressing the federal government. Interest on the national debt set a record last year, costing $1.2 trillion. That was up 7.3 percent over 2024.

The government needs the Fed to keep buying bonds (and expanding the balance sheet) to facilitate the out-of-control borrowing and spending.

So, what's a Fed member to do?

Talk about how policy is in the right place and crack the door open for a rate hike, apparently. But ultimately, they will have to choose. Will they give the rate-hike medicine and hope the interaction with the Debt Black Hole doesn't kill the economy? Or do they forgo the medicine and pray inflation doesn't kill it?

There is no good choice here. But historically, when push comes to shove, the Fed picks inflation.

The Debt Black Hole is just one dynamic that mainstream pundits are missing in their narrative surrounding gold (The other is real interest rates). That’s why you might be wise to stop and think hard about following the herd and selling your gold.

There's a new sheriff in town at the Fed, but his options are every bit as limited by economic reality as the old sheriff's.

To receive free commentary and analysis on the gold and silver markets, click here to be added to the Money Metals news service.

Author

Mike Maharrey

Money Metals Exchange

Mike Maharrey is a journalist and market analyst for MoneyMetals.com with over a decade of experience in precious metals. He holds a BS in accounting from the University of Kentucky and a BA in journalism from the University of South Florida.