The US flash PMI may be a bigger deal than ever

Outlook:

Now that we have European PMIs and the very bad manufacturing PMI from Germany, the US flash PMI this morning may be a bigger deal than ever. We also get the Philly Fed, durables, leading indicators, existing home sales and the usual Thursday jobless claims. We know ahead of time that the government shut-down in January will affect some of this data, but the real question is whether we see slump leading to stagnation, as in Germany, or a steadier trajectory.

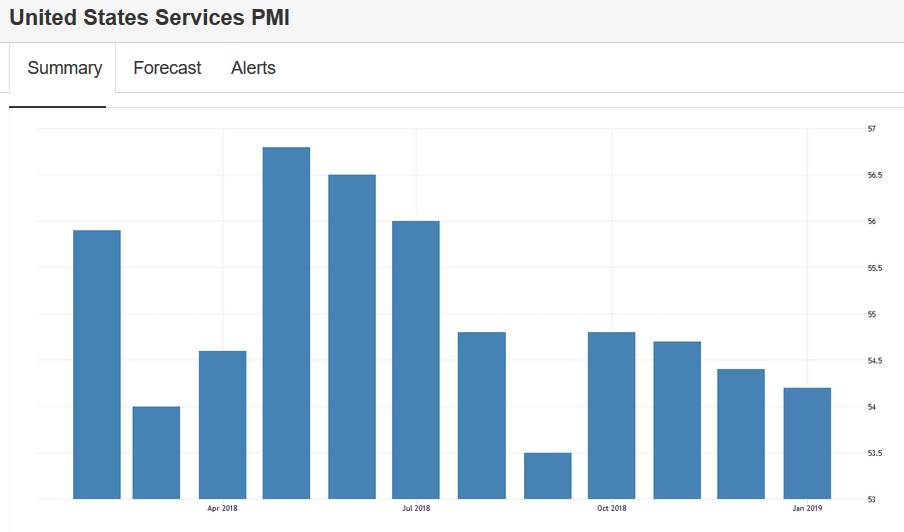

Tradingeconomics.com has this chart of the combined PMI showing a decline for over a year. In Jan, the PMI fell only a little to 54.2 from 54.4 in Dec. "The upturn in new business received by service providers was the joint-slowest since October 2017, with new export orders falling for the second successive month, and employment growth eased to the second-weakest since June 2017. On the price front, input cost inflation softened to a 22-month low while the rate of charge inflation picked up from December's 12-month low. Looking forward, firms registered a stronger degree of confidence towards business activity levels over the coming 12 months."

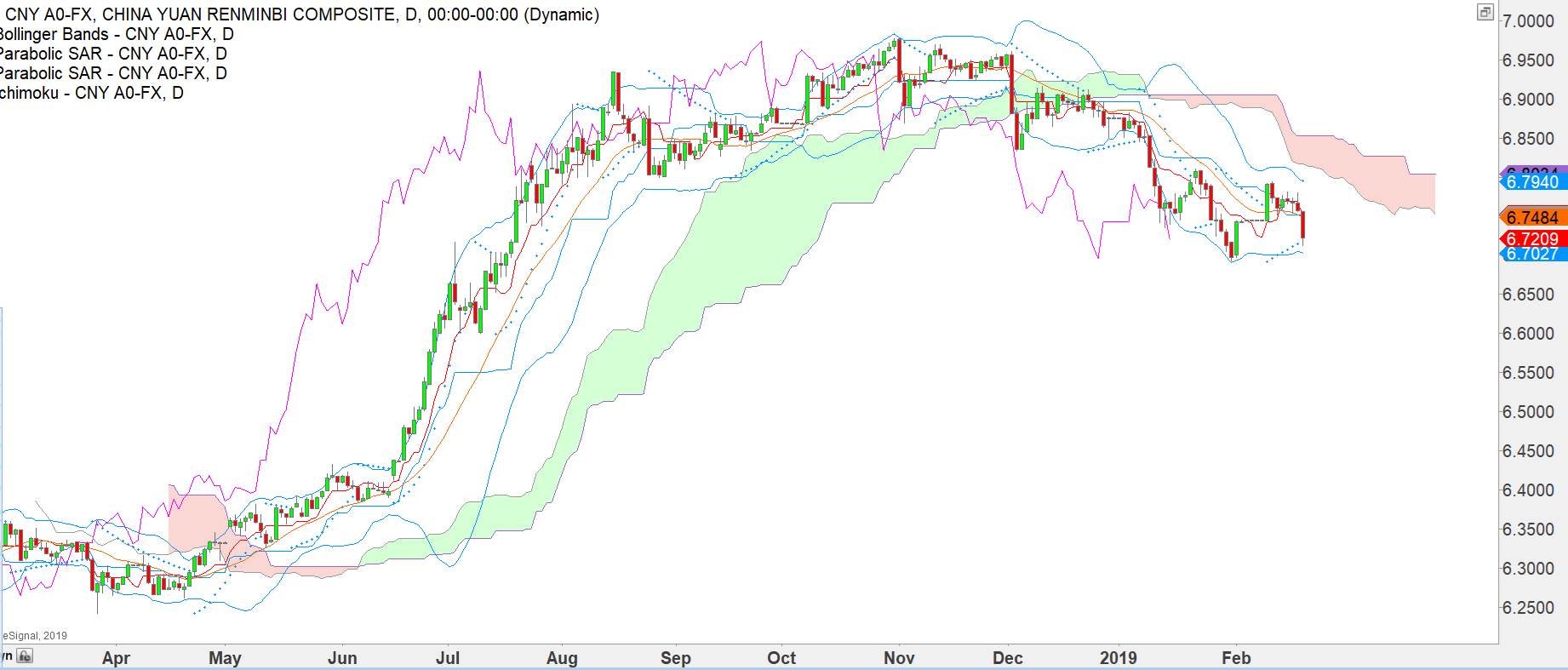

What this means is "mixed." If we get another mixed outcome from manufacturing today, the effect will be minor. A bad reading, however, sets the cat among the pigeons again—to mix metaphors, a contest between which is the least pretty girl, the US or Germany/UK/Japan. Bloomberg notes that the fate of China will determine or at least largely influence the rest of the world. Activity in China "would seem to be a major deal for global markets, to put it mildly. ‘Where the yuan goes is now as much a driver as a reflection of global FX trends,' writes SocGen's Kit Juckes. ‘Three of the last four cyclical peaks and troughs in the dollar's trade weighted index have come shortly AFTER the peak/trough in USD/CNH, and the correlation with global risk sentiment is very strong too.'" Well, we have one of those inflection points now. The dollar/yuan has already fallen over a third from the tough-peak rise. Additional dollar devaluation, which is what Trump wants, presumably lies ahead. This causes a headwind for the Chinese economy, but announcement of a trade deal will be bigger as well as more immediate. It could come as early as tomorrow. The signs we are getting, if they can be trusted, are that Trump is the one who will cave the most and China will see itself as the winner. Trump can claim all he likes that he was the winner but the rest of the world will know that's not true, except his base, which never fact-checks anything.

If the end or near-end of the trade conflict is what we get today, look for the dollar to drop, and possibly quite hard. The euro will gain on the prospect of renewed exports to China. The Trump-manufactured crisis will seem to be over, or nearly over. Stock markets will rally like crazy. It's even possible we can foresee a little inflation in the US from the effect of upcoming higher-priced imports. All will be right with the world. Well, no, but it's one scenario and a whole lot better than the scenario we had before, the one in which a stubborn Trump fights to the last breath—ours. The rosy scenario may be built on a weak premise—that Trump likes to brag and claim credit for things he has not in reality achieved. We can hope that the unsourced reports that he wants to end this thing are true.

Tidbit: The TV talking heads are all abuzz at the idea the special prosecutor report will be out soon, at least to the Attorney General and maybe to Congress and hopefully to the public. Some analysts see a specific crime Trump committed—obstruction of justice by firing Comey and maybe for trying to get his own man into the New York office—while others say there is no smoking gun proving Trump knew all the stupid and criminal things his minions were up to. Trump is so careless and such a bad manager that we can believe he really was ignorant. After all, he's ignorant of so much. He's also a liar, crude, self-absorbed, a liar, a bad speaker, arrogant, a liar, a sleaze, and a fraudster as well as a liar—but none of those things are crimes. At the moment, we see his lie that the press is the enemy of the people as the worst lie of all, but again, free speech and not a crime. At a guess, there will be enough in the report to inspire the House to start the impeachment process, but many would still prefer an indictment and to see this lout in an orange jumpsuit. We may have to wait for indictments until after he leaves office.

The imminence of the report is not certain. One worry is that the new Attorney General did shut the investigation down, despite saying in his confirmation hearings that he would allow Mueller to complete the project. Another worry is that the behavior of some parties, particularly Don Junior and son-in-law Kushner, was already deemed bad but not indictable, so let it slide. A third concern is that the investigations under way in New York State and otherwise outside the special prosecutor purview will lose steam. This includes misbehavior and perhaps crimes by the Foundation and the Campaign.

On the side of those who want to see decency restored, Congress can pursue any or all of these things, too, and add to it tax evasion not only by the Foundation but by the Trump Organization itself. And each state can go looking for Trump activity to prosecute, far from the grip of the Trump-controlled Justice Department. This has already lasted longer than Watergate and may well last until Trump is dead and gone. In a way, the resolve to punish a crooked president is a good thing. The US allows lots of unethical and unprincipled events to occur. To some extent, that's an inevitable side-effect of freedom, including freedom of speech, plus a reluctance to get tangled up in too many guidelines and regulations. As an aside, note that a US-China trade deal is not favorable for Australia. With China the winner, so to speak, it gets to persist in punishing Australia for banning Huawei (assuming that is what's behind the coal import ban). And the US could so easily write that in...

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a free trial, please write to [email protected] and you will be added to the mailing list..

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat