The UK monthly GDP rises 0.3% confirming the Bank of England improved growth outlook

- The UK GDP increased 0.3% over the three months ending in May in the first rolling monthly reading from the Office for National Statistics.

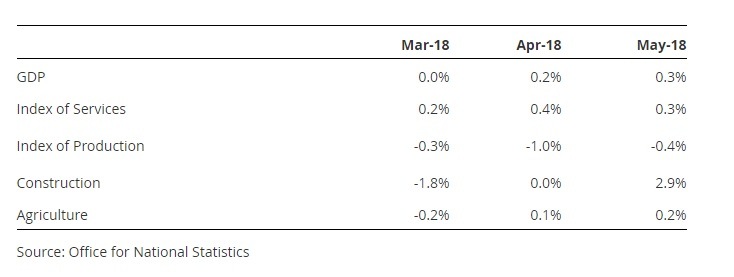

- The UK monthly GDP growth was driven by services, with falls in construction and production.

- UK manufacturing contributed negative -0.12 percentage points to the UK GDP.

The UK three months rolling GDP increased by 0.3% in May in the first reading ever made by the Office for National Statistics (ONS). The UK GDP growth was driven by services, with falls in construction and production.

The UK services marked 0.4% m/m growth in the services industries in the three months to May and had the biggest contribution to GDP growth. However, contraction in the production and construction industries meant that they each had negative contributions to GDP.

“Services, in particular, grew robustly in May with retailers enjoying a double boost from the warm weather and the royal wedding. Construction also saw a return to growth after a weak couple of months," Rob Kent-Smith, the head of National Accounts at the ONS said in the report.

In terms of main sectors, the UK manufacturing fell -1.2% in the three months to May with a negative contribution of -0.12 percentage points to headline GDP. This was the third consecutive fall in manufacturing and was driven by weak exports, the ONS said in the report.

Mining and quarrying increased by 4.6% in the three months to May despite a May growth figure of negative -4.6%, which was in part due to the Sullom Voe oil and gas terminal shutdown. Electricity and gas supply contracted by -0.5%, due to the warmer weather in this period.

The method of publishing the GDP on a rolling three-month data is based on a calculation comparing growth in a three-month period with growth in the previous three-month period. For example growth in March to May compared with the previous December to February. Such comparison is set to give the policymakers a better picture of the underlying changes in the economy than a method of quarterly comparisons.

To compare, the three months rolling GDP ending in March of 2017 was flat and rose 0.2% in three months ending in April.

This confirms the growth outlook of the Bank of England for the UK growth improving after the first quarter weather-related slump.

”Number of indicators of household spending and sentiment has bounced back strongly from what appeared to be the erratic weakness in Q1, in part related to the adverse weather. Employment growth has remained solid,” the Bank of England wrote in the monetary policy statement in June.

Breakdown of GDP growth rates by month

Author

Mario Blascak, PhD

Independent Analyst

Dr. Mário Blaščák worked in professional finance and banking for 15 years before moving to journalism. While working for Austrian and German banks, he specialized in covering markets and macroeconomics.