The S&P 500 closed up 0.47% at 2886.73 yesterday

Highlights:

Market Recap: The S&P 500 closed up 0.47% at 2886.73 yesterday. The 10 year Treasury note yield increased 6 basis points. Copper showed some strength, up 1.29%, while the rest of the commodity market was down -0.20%. The US Dollar was up 0.23% on the day, bouncing from short-term oversold levels. The Russell 2000 was up 0.61% yesterday as well. Small caps gained against large caps for the first time in several trading sessions.

Economic Data: Today we get data on producer prices for the month of May. Consensus expectations are for a gain of 0.1% month over month.

Sector Spotlight: Retail has been extremely weak relative to the broad market. It is in a strong negative trend and concerns us regarding broad market direction.

Semiconductors: The semiconductor index has bounced off support and staged an impressive rally over the course of the last week. If semiconductors can continue to rally, it would be a positive signal for the broad market. The ratio of the semiconductor sector relative to the S&P 500 is back above the 200 day moving average.

Factors: The quality factor bounced off the 200 day moving average and has rallied significantly. Will it surmount the old highs? This would be a positive sign for the overall market. Technology will need to continue to show strength for this to occur.

US 10 Year Yields: Yields bounced 6 basis points yesterday after dropping last week. The benchmark rate is back above support but still in a strong negative trend. With expectations of a Fed rate cut and slowing economic growth and inflation, we expect interest rates to continue their downward trajectory.

Junk Bonds: High yield bonds (JNK) rallied substantially last week. They continued the rally against Treasury bonds (TLT) yesterday. As the Fed has all but ensured us that they will support the credit markets, buyers came back in and spreads have compressed slightly. The question is whether this is short-term, or whether spreads will shrink to new lows.

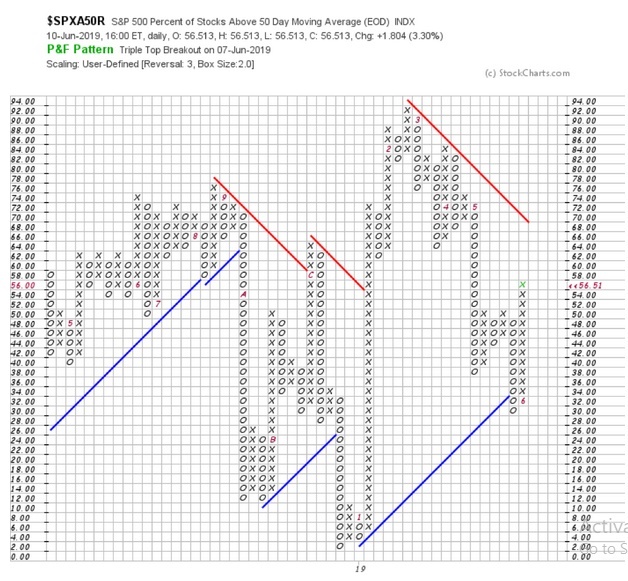

Market Internals: Short-term market internals gave a point and figure buy signal. The percentage of stocks in the S&P 500 that are above the 50 day moving average closed above 52% and generated a triple-top buy signal. This is supportive of a continuation as this index is not yet overbought. The market rally could last a little while longer. However, it is important to remember the continued backdrop of slowing economic growth and high valuations.

Futures Summary:

News from Bloomberg:

Apple has a backup plan if the trade war gets out of hand. There's enough capacity to make all iPhones bound for the U.S. outside of China if necessary, according to its main manufacturing partner Hon Hai. Most are currently made in the Chinese mainland. Hon Hai also said it will hire up to 13,000 in Wisconsin as promised.

The U.S. expressed "grave concern" over Hong Kong legislation that would allow extraditions to the mainland as the city braces for new protests and potential strikes. Here's a QuickTake on the law that's sparked massive opposition. And, out at sea, the U.S. Coast Guard said its increased presence in the South China Sea is in response to complaints from island nations of overfishing and dredging, particularly by China.

Deals news: Apollo will buy Shutterfly for about $1.74 billion in cash and plans to merge it with Snapfish. CVS's $68 billion purchase of Aetna may be blocked by a federal judge, the NY Post reported. A final T-Mobile, Sprint decision may come this week, Fox Business said. And a group led by Ares and Leonard Green are close to buying Press Ganey from EQT Partners for $4 billion, people familiar said.

Russia and Saudi Arabia—the OPEC+ deal's architects—may find it hard to reconcile differences and extend output cuts, Goldman Sachs said. Uncertainty over supply, Iran's exports and demand fundamentals make it difficult to know what output level will actually balance the market. Separate energy outlooks from BP and the EIA today will offer food for thought.

U.S. stock-index futures rose with European and Asian equities as investors trained their focus anew on the trade arena. Chinese shares got on board, with news that local governments will have more room to spend on infrastructure. Treasuries and gold slipped. Oil gained.

Author

Clint Sorenson, CFA, CMT

WealthShield