The S&P 500 closed the day up 0.97% at 2917.75

Highlights:

Market Recap: The S&P 500 closed the day up 0.97% at 2917.75. The Russell 2000 closed up 1.14% for the day. The CRB index (commodities) was up 0.96% on the day. The U.S. Dollar was flat on the day, and the U.S. Treasury Yield dropped 3 basis points. Risk-on assets rallied on the news that Trump will meet with President Xi at the G20 meeting to discuss trade with China.

Economic Data: Building permits grew 0.3% month-over-month and housing starts shrank by -0.9% month-over-month. Housing starts were expected to decline by -0.4% month-over-month. Tomorrow we get the Fed rate decision and economic projection. The market is expecting that the Fed will drop the "patient" language from the statement and pave the way for a rate cut in July.

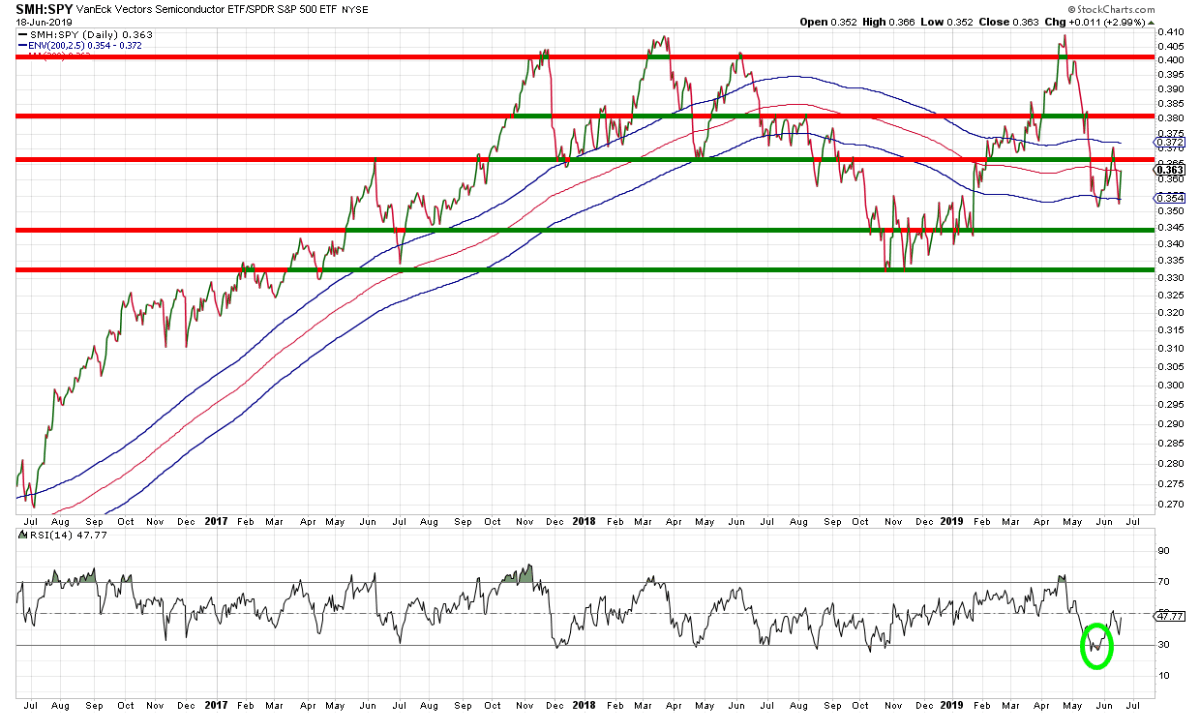

Semiconductors: Semiconductors rallied over 4% on the news of a meeting with China at the G20. The sector rallied 2.99% against the S&P 500, despite terrible fundamentals and slowing growth. Relative to the S&P 500, they are still in a negative trend. A move to new highs in this index would open up new highs in the S&P 500 and would be a risk-on indication.

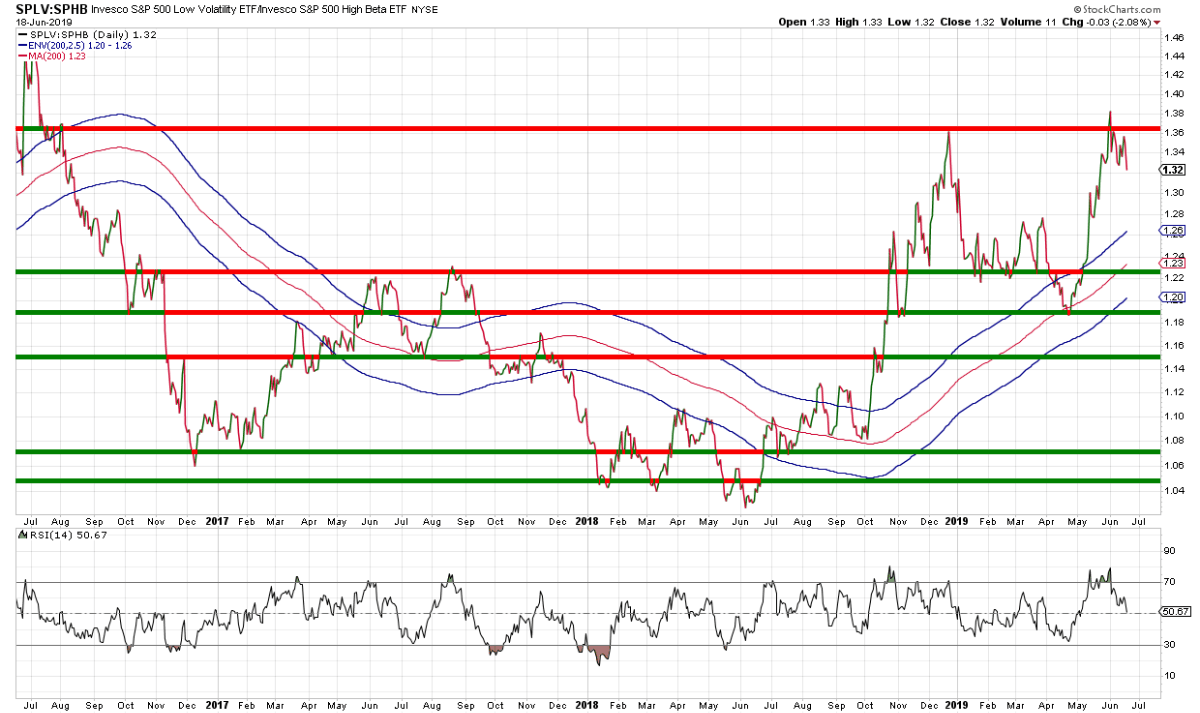

Low volatility: The low volatility ETF (SPLV) dropped over 2% against the high beta ETF (SPHB). This is an indication of a risk on move in equity markets. The move higher in prices today was confirmed by the relationship between low vol and high beta. The question is now whether this is just a pause before a move higher by low vol, or if it is a reversal in trend. We believe the implications are of great importance. A breakdown would indicate a failure at important resistance and would suggest that new highs from the broad market could follow.

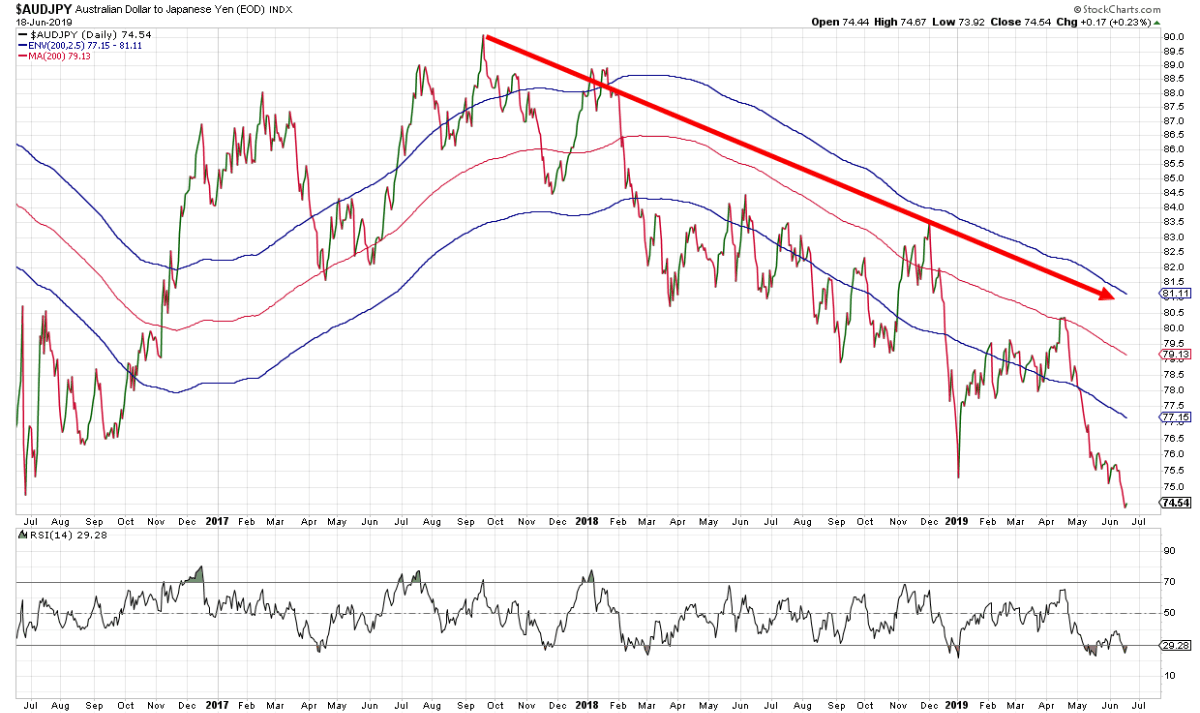

Australian Dollar versus Japanese Yen: The Australian dollar rallied slightly against the Japanese yen. The trend has long been in favor of the traditionally defensive currency, the Yen. However, the Australian Dollar rallied today, confirming the broader risk-on move. The Australian dollar is still in a negative trend relative to the Yen, although momentum is positively diverging. A move upward in the Australian dollar could be a positive signal for risk assets. Currently, however, the trend is still suggestive of a negative non-confirmation of broad equity markets.

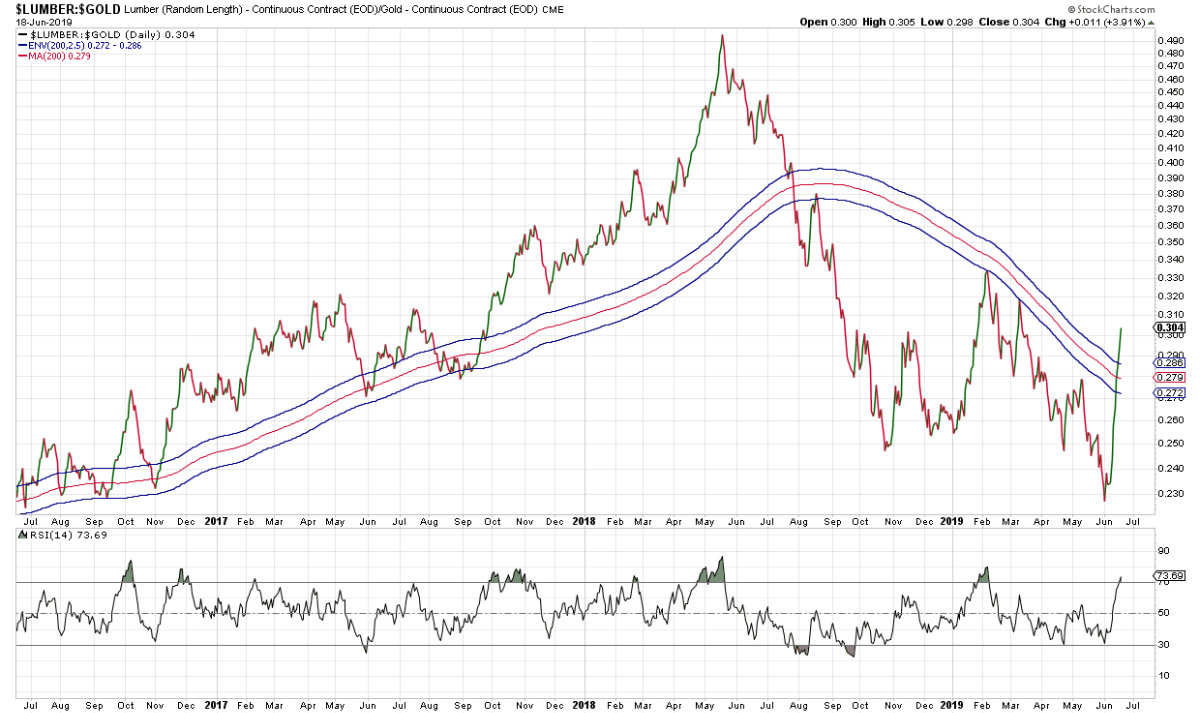

Lumber/Gold: The lumber to gold ratio has staged an impressive rally that bodes well for equity markets and suggestive lower volatility. Lumber is back in a positive trend relative to Gold for the first time since early 2018. Will the trend last? We will only know in hindsight. The move has been fast and furious, indicative of an oversold rally. It could be prone to failure. However, the current trend is bullish for equity prices now, and that is all we can go by.

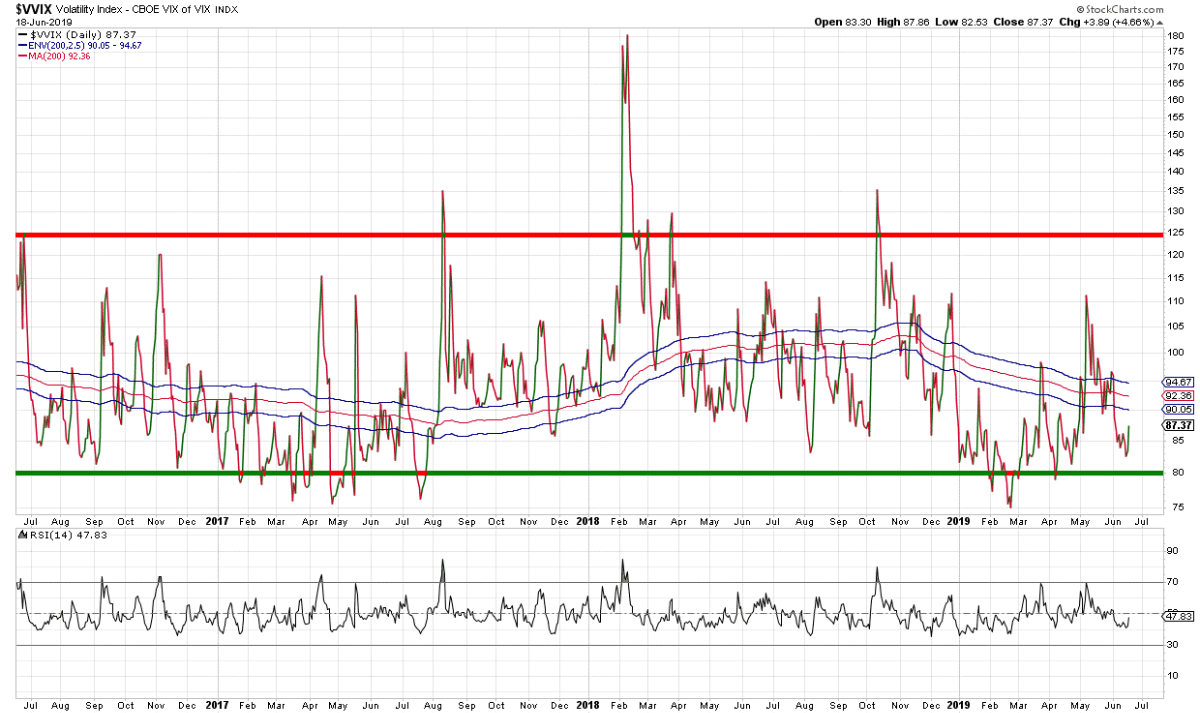

Volatility: The volatility of volatility (VVIX) rallied over 4% today in a move that seemed contrary to the overall risk move in asset prices. The VIX ultimately dropped -1.30% today, despite the spike in the vol of vol. Historically, this could mean a short-term top in the S&P 500 and bottom in the VIX. Nothing is for certain, however. Just evidence that suggests using a risk management approach to investing. Stop losses are probably welcome.

Futures Summary:

News from Bloomberg:

The Fed may open the door to a rate cut, but is unlikely to slash them today even as its chairman Jerome Powell faces political pressure. Instead, investors will watch to see if "patient" vanishes from the statement. Markets expect at least one reduction this year and some strategists think the Fed may start with a bigger-than-priced move. The last two easing cycles began with 50 basis-point cuts. Here's our Decision-Day Guide.

Apple asked its largest suppliers to work out the cost of shifting 15% to 30% of its output from China to Southeast Asia as the trade war bites, Nikkei reported. Even if the U.S. and China call a truce, Apple will press ahead because it has become too reliant on Chinese manufacturing. For more information about the trade war, this guide explains where we are.

Donald Trump is weighing sanctions to punish Turkey for buying a Russian missile system, people familiar said. The most severe packages under discussion will effectively cripple Turkey's economy. But President Erdogan thinks he can persuade Trump that buying the S-400 isn't a big problem, other people said. Here's the history of the strained relationship between the U.S. and Turkey.

The president began his re-election bid, making it clear he'll try to animate his political base by exploiting political divisions, appealing to fear of immigrants and hostility toward Democrats. His allies said the Florida rally demonstrated how he'll confront running as an insurgent incumbent. He roused the crowd by testing two slogans: "Make America Great Again" and "Keep America Great." The latter won.

U.S. stock-index futures were in a holding pattern before the Fed decision, while Treasuries and the dollar slipped. Asian markets bucked the trend, with the benchmark headed for its biggest advance in five months. The yen was steady. Oil was little changed, while gold and most industrial metals dropped.

Author

Clint Sorenson, CFA, CMT

WealthShield