The Return of the Impeachers [Video]

![The Return of the Impeachers [Video]](https://editorial.fxstreet.com/images/Markets/Equities/stock-certificates-11742678_XtraLarge.jpg)

US Dollar: Dec USD is Down at 97.475.

Energies: Jan'20 Crude is Down at 58.24.

Financials: The Mar'20 30 year bond is Down 1 tick and trading at 158.22.

Indices: The Dec S&P 500 emini ES contract is 20 ticks Higher and trading at 3116.00.

Gold: The Feb'20 Gold contract is trading Down at 1480.00. Gold is 2 ticks Lower than its close.

Initial Conclusion

This is not a correlated market. The dollar is Down- and Crude is Down- which is not normal and the 30 year Bond is trading Lower. The Financials should always correlate with the US dollar such that if the dollar is lower then bonds should follow and vice-versa. The S&P is Higher and Crude is trading Lower which is correlated. Gold is trading Lower which is not correlated with the US dollar trading Down. I tend to believe that Gold has an inverse relationship with the US Dollar as when the US Dollar is down, Gold tends to rise in value and vice-versa. Think of it as a seesaw, when one is up the other should be down. I point this out to you to make you aware that when we don't have a correlated market, it means something is wrong. As traders you need to be aware of this and proceed with your eyes wide open.

At this time all of Asia is trading mainly Higher with the exception of the Indian Sensex exchange which is Lower at this time. Currently Europe is trading Higher with the exception of the London and German Dax exchanges which are Lower at this time..

Possible Challenges To Traders Today:

-

Challenger Job Cuts y/y is out at 7:30 AM. This is Major.

-

Trade Balance is out at 8:30 AM EST. This is Major.

-

Unemployment Claims are out at 8:30 AM EST. This is Major.

-

FOMC Member Quarles Speaks at 10 AM EST. This is Major.

-

Factory Orders are out at 10 AM EST. This is Major.

-

Natural Gas Storage is out at 10:30 AM EST. This is Major.

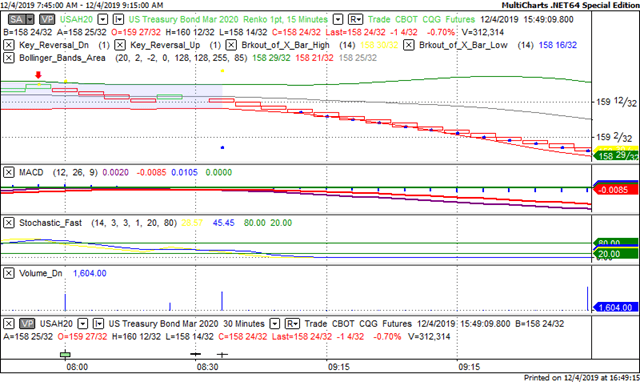

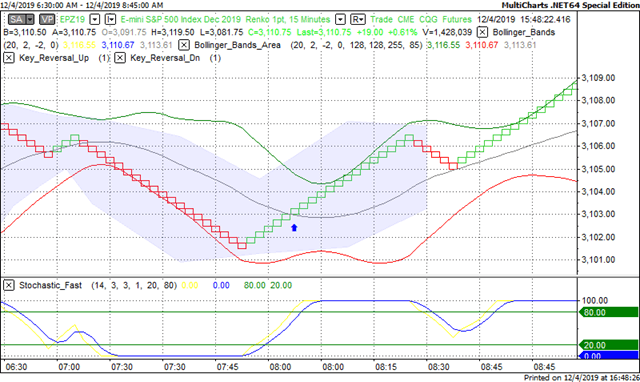

Treasuries

We've elected to switch gears a bit and show correlation between the 30 year bond (ZB) and The S&P futures contract. The S&P contract is the Standard and Poor's and the purpose is to show reverse correlation between the two instruments. Remember it's liken to a seesaw, when up goes up the other should go down and vice versa.

Yesterday the ZB made a major move at around 8 AM EST. The ZB hit a High at around that time and the S&P moved Higher. If you look at the charts below ZB gave a signal at around 8 AM EST and the S&P moved Higher at the same time. Look at the charts below and you'll see a pattern for both assets. ZB hit a High at around 8 AM and the S&P was moving Higher shortly thereafter. These charts represent the newest version of MultiCharts and I've changed the timeframe to a 15 minute chart to display better. This represented a Shorting opportunity on the 30 year bond, as a trader you could have netted about 20 plus ticks per contract on this trade. Each tick is worth $31.25. Please note: the front month for the ZB is now March '20. The S&P contract is still December. I've changed the format to Renko bars such that it may be more apparent and visible.

Charts Courtesy of MultiCharts built on an AMP platform

Bias

Yesterday we gave the markets an Upside bias as both the Bonds and Gold were trading Lower yesterday morning and this usually reflects an Upside day. The Dow gained 147 points and the other indices gained ground as well. Today we aren't dealing with a correlated market and our bias is to the Upside.

Could this change? Of Course. Remember anything can happen in a volatile market.

Commentary

Yesterday we witnessed the return of the impeachers as the impeachment hearing have returned. I don't why it is but each time there's an impeachment hearing the markets rise. You would think the opposite would be the case but no the markets advance. Yesterday was no except as the Dow rose 147 points and the other indices gained ground as well. Today we have a bit more economic news on the docket as we have Factory Orders and Challenger Job Cuts which will dovetail nicely with tomorrow's Non Farm Payrolls report.

Author

Nick Mastrandrea

Market Tea Leaves