The rest of the inflation story

If you’re reading the headlines, you know that the Consumer Price Index (CPI) came in even cooler than expected. And the expectation was for a much cooler CPI thanks to falling oil prices. However, the CPI doesn’t tell the entire inflation story.

The CPI measures price inflation. That is just one manifestation of monetary inflation (the way economists used to define “inflation”). While price inflation has cooled dramatically, there is still plenty of inflation in the pipeline.

And this better-than-expected CPI print may green-light even more inflation in the near future.

CPI By the Numbers

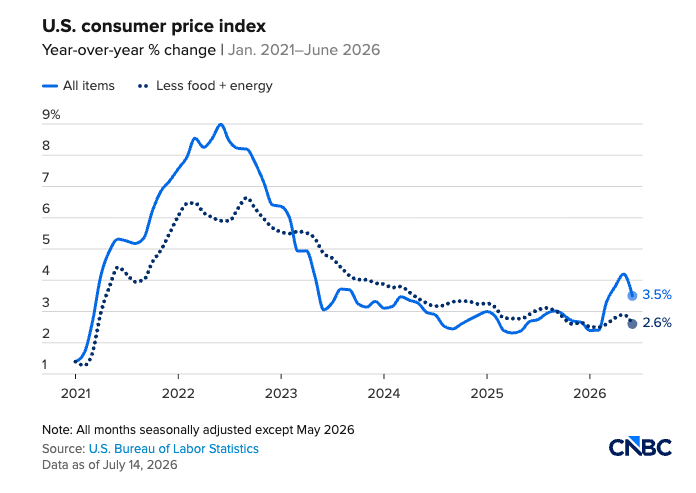

If we just consider the CPI, the inflation picture looks fantastic.

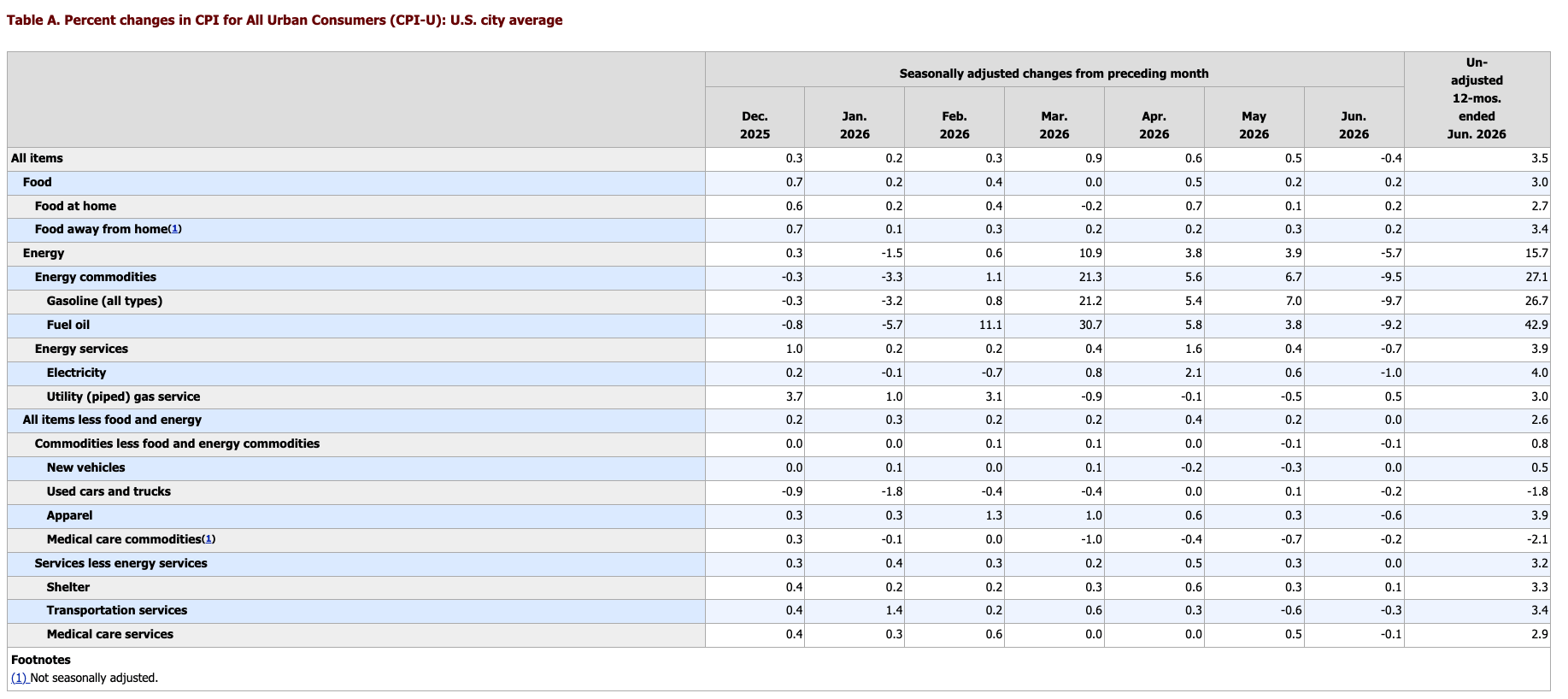

Month on month, prices fell by -0.4 percent in June. The expectation was for a more modest -0.2 percent decline in prices.

It was the largest monthly price drop since the COVID crash in 2020.

The monthly decline in prices pushed the annual CPI down to 3.5 percent, much better than the 3.8 percent forecast. Keep in mind, this is coming off a 4.2 percent annual CPI in May.

It was the biggest decline in CPI in six years.

A significantly cooler CPI was expected due to plunging gas prices. However, the better-than-expected core CPI numbers were a bit more surprising.

Stripping out more volatile food and energy prices, core CPI was flat. The forecast was for a 0.2 percent increase. With no monthly change in core prices, the annual core CPI fell to 2.6 percent. The forecast was for the annual core CPI to remain flat at 2.9 percent.

Looking at some of the trends creates even more of a cause for optimism. The three-month CPI annualized is just 2.8 percent.

Falling energy prices were the biggest factor driving the overall CPI down. The energy index declined 5.7 percent month-on-month. Gasoline prices fell by 9.7 percent.

Notably, apparel prices, which are heavily impacted by both tariffs and energy costs, dropped by a healthy 0.6 percent month-on-month.

Service prices were flat.

Other sectors reported price increases, including a 2 percent month-on-month rise in food prices.

I should note that despite the victory dance, price inflation remains above the mythical 2 percent target, as it has been for years.

You also need to remember that the CPI data understates price inflation by design. The government revised the CPI formula in the 1990s so that it understated the actual rise in prices. Based on the formula used in the 1970s, CPI is closer to double the official numbers. So, if the BLS used the old formula, we’d be looking at CPI closer to 6 percent. And using an honest formula, it would probably be worse than that.

The rest of the inflation story

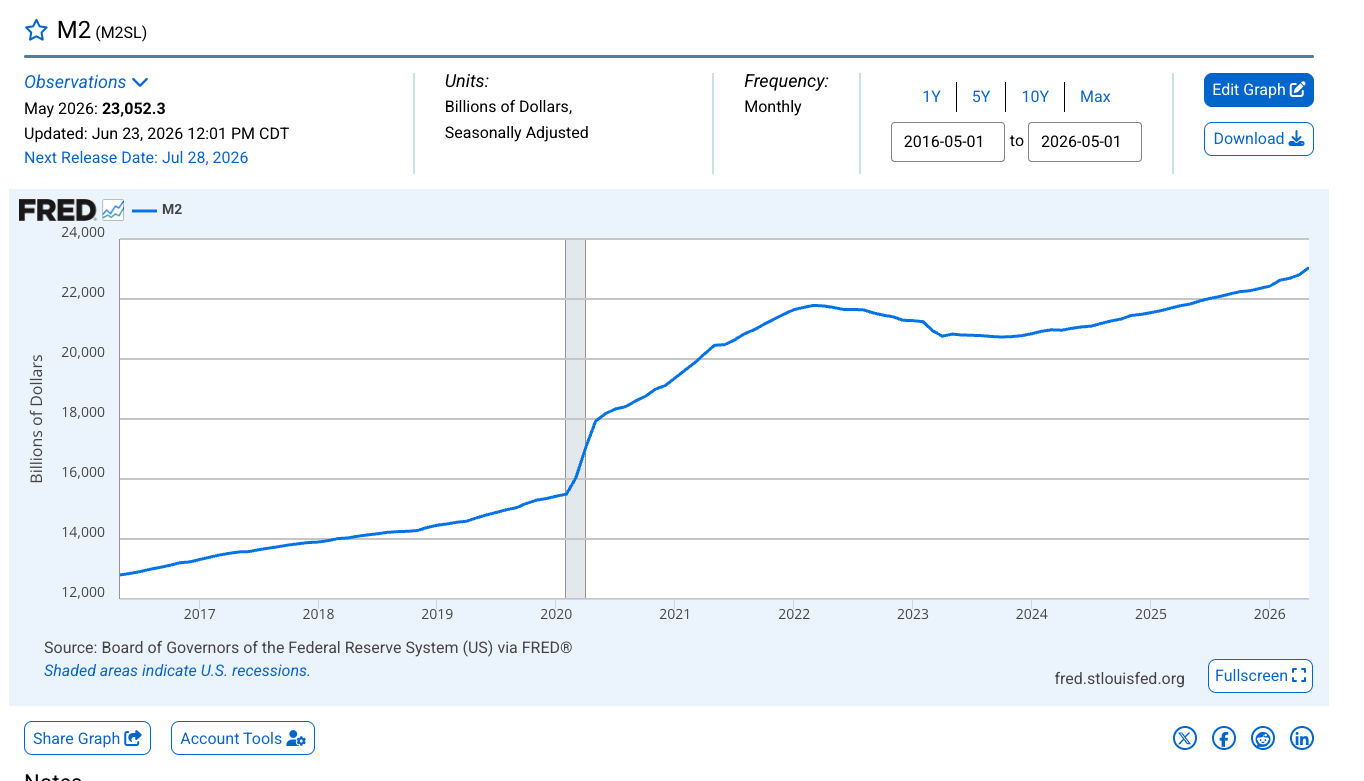

The CPI doesn’t tell the entire inflation story. As already mentioned, inflation, properly defined, is an increase in the amount of money and credit. Rising consumer prices are one symptom of this monetary inflation.

Based on the absence of this symptom, one might conclude that inflation is retreating. However, when we look at the money supply's trajectory, we find that inflation is on the rise.

According to the Fed’s M2 data, the money supply increased from $21.83 trillion in May 2025 to $23.05 trillion in May 2026, a 5.6 percent increase.

In other words, we have an actual inflation rate of 5.6 percent.

This monetary inflation will eventually find its way into consumer prices. (It could also manifest in rising asset prices such as real estate and equities.)

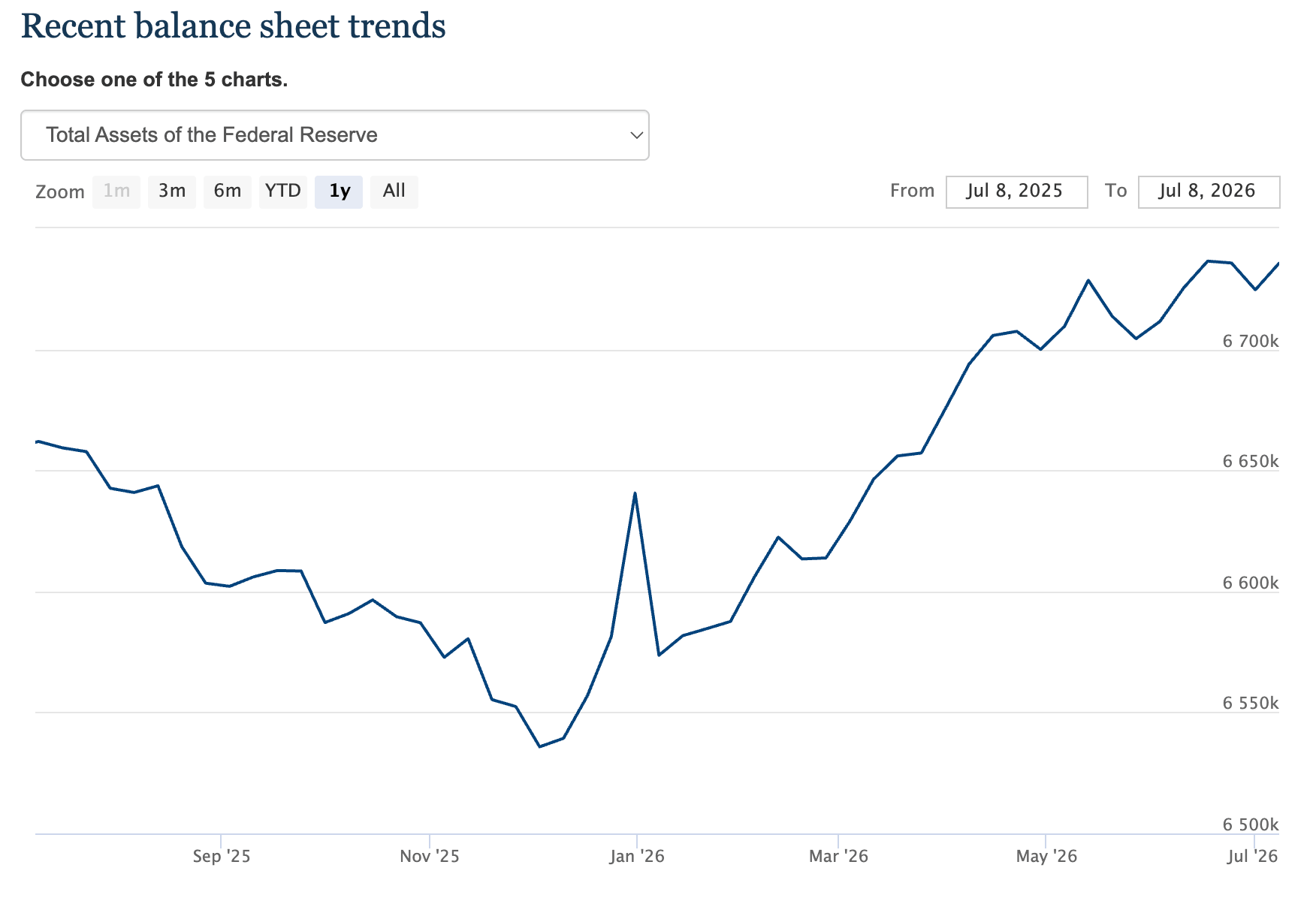

Given the Federal Reserve’s tough talk on inflation, many analysts think a good CPI report won’t motivate the central bankers to return to monetary easing. CNBC reported, “Though the inflation readings provided some hope, they are unlikely to motivate Federal Reserve officials to lower interest rates anytime soon, with the central bank broadly expected to raise its benchmark rate in September.”

However, the Fed is already delivering monetary easing. The central bank’s balance sheet began ticking up in December, and the upward trend continues today.

This indicates that the Federal Reserve is running quantitative easing (QE) operations as we speak to provide support to the bond market. This involves creating money out of thin air to buy U.S. Treasuries on the open market. This is, by definition, inflation.

A positive CPI print gives the central bankers at the Fed a plausible excuse to cut rates, especially if the economy shows signs of deterioration.

Fed Chair Kevin Warsh & Company will likely keep up the tough inflation talk; however, it will eventually run up against economic reality.

The bottom line is it’s not the time to celebrate inflation’s demise. Absolutely enjoy the lower fuel prices. But remember, there is more inflation in the pipeline. One thing you can count on: the powers-that-be will relentlessly devalue your money – at least by the planned 10-plus percent every five years.

To receive free commentary and analysis on the gold and silver markets, click here to be added to the Money Metals news service.

Author

Mike Maharrey

Money Metals Exchange

Mike Maharrey is a journalist and market analyst for MoneyMetals.com with over a decade of experience in precious metals. He holds a BS in accounting from the University of Kentucky and a BA in journalism from the University of South Florida.