2% and nothing else: Why Warsh gave Congress three hours of Greenspan

The Federal Reserve (Fed) Chair who wants the institution to say less spent Tuesday legally required to say more, on the one morning the data handed him something pleasant to say. June's Consumer Price Index (CPI) fell 0.4% on the month, the steepest single-month decline since April 2020. Kevin Warsh, in the second hour of his first semiannual testimony before the House Financial Services Committee, told lawmakers that mission accomplished is not his view of the numbers. The refusal is the story. Across roughly three hours of questioning, the no-guidance regime installed in June survived its first statutory stress test, but it leaked in three places, and the leaks say more about where policy is heading than anything in the prepared text.

The one communication he can't cancel

Warsh has spent two months stripping the Fed's voice. Forward guidance is gone, the policy statement runs about 130 words, his own dot is withheld from the Summary of Economic Projections (SEP), and press conferences may soon happen only when the Fed has something to say. The semiannual Monetary Policy Report is the one channel he cannot touch: The Federal Reserve Act compels it, and his prepared text conceded as much, noting that some Fed communications are discretionary but not this one.

Then he opened with a eulogy. Alan Greenspan died last month after a century of life, and Warsh reminded the committee that his friend appeared before Congress more than 200 times with his famously distinctive way with words. Honouring the man who turned two decades of mandatory hearings into a masterclass in saying nothing quotable is not sentimentality, it is a mission statement. The Warsh doctrine was never silence. It is Greenspan's opacity at a lower word count, and Tuesday was its first live demonstration: Three hours in the chair, and the market learned nothing about the rate path it did not know at breakfast.

The quietest hawk in the room

The print he declined to celebrate was the best of the war. Headline CPI fell 0.4% in June against a consensus of -0.1%, dragging the annual rate to 3.5% from May's 4.2% and well under the 3.8% forecast. The energy index sank 5.7%, its largest monthly drop since April 2020, gasoline fell 9.7%, and core prices were flat on the month, the softest core reading since May 2020. On any normal Tuesday, a new chair fighting a five-year inflation surge takes the win.

Warsh took the opposite. Shortly after 15:40 GMT he told the panel that mission accomplished is not his view after the data, and that he does not think everything is, in his word, swell. His prepared text had already laid the track, calling monthly price fluctuations inevitable in an unsettled world, a line that waves away good months and bad ones with the same hand.

The scepticism is earned, and readers of this desk know why. June was the peace-dividend month: Crude fell roughly 25% while the interim framework held, and that is the decline sitting in Tuesday's energy line. The ceasefire died last week. The third break of the ceasefire re-shut the Strait of Hormuz, sanctions on Iranian crude are back, and Brent is higher again Tuesday, extending the rebound that ran through $80 within two sessions of the escalation. The machine that put a 4 handle on May's CPI works in reverse too, and it has already shifted gears again. Meanwhile, the downstream bill, fertilisers, food, petrochemicals, the passthrough the hawkish SEP was actually pricing, arrives on a planting-to-harvest lag no ceasefire can refund. The pump handed June its discount. The pump was never the tell.

Guidance is dead, long live guidance

What Warsh refused to give was everything the hearing exists to extract. No rate path. No standard for when elevated inflation becomes persistent, the very word his committee's resolve hangs on. Asked directly by Chairman French Hill how the Fed intends to restore price stability, he pointed to the rate and balance sheet toolkit and stopped. Pressed on his communications diet, he told the panel that forward guidance is not a business the Fed should be in — an answer delivered, without apparent irony, to the body that legislated his attendance.

The vacuum did not stay empty. Governor Christopher Waller said on Monday that a hot Tuesday print would force the committee to consider a near-term hike, adding he is loath to repeat the Fed's post-pandemic sin of waiting too long. John Williams of the New York Fed argued last week that core inflation holding a 0.2% monthly pace through year-end means no hike is needed at all. Kill the chair's dot and guidance does not die, it multiplies: Nine of 18 June dots carried a 2026 hike,. While the minutes credited only a few, and that “family fight” denied a statement or a dot to live in, now it plays out speaker by speaker in public.

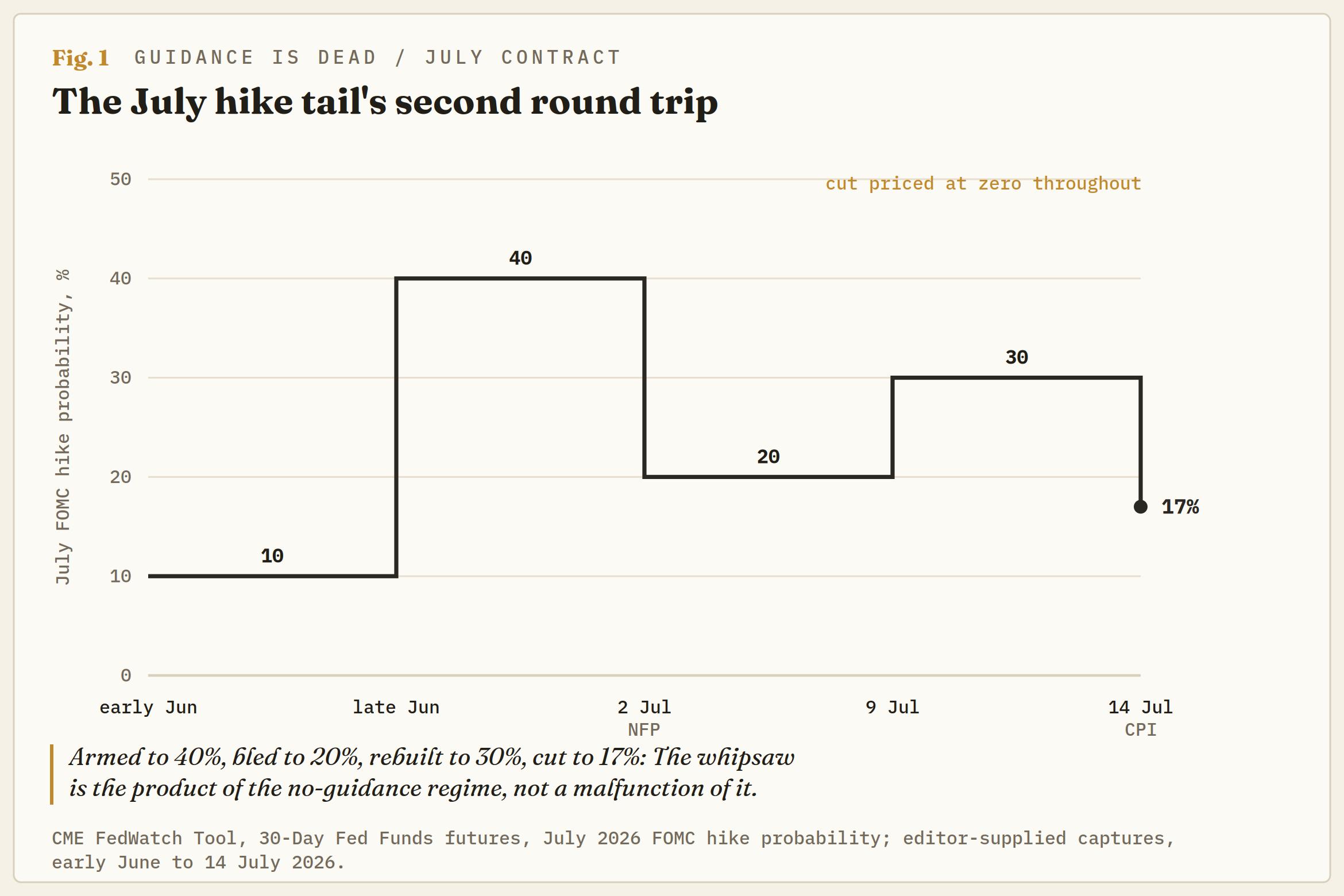

The tape shows the cost. Bond traders spent Monday building July hike bets into the CPI release. By Tuesday afternoon, CME FedWatch had the odds of a July 29 hold at 86%, cutting the hike tail roughly in half from the 30% it carried a week ago. That is the second five-session round trip in the July contract this month. Under the old regime, the chair would have leaned against at least one leg of it. Under this one, the whipsaw is the product.

The signals he sent anyway

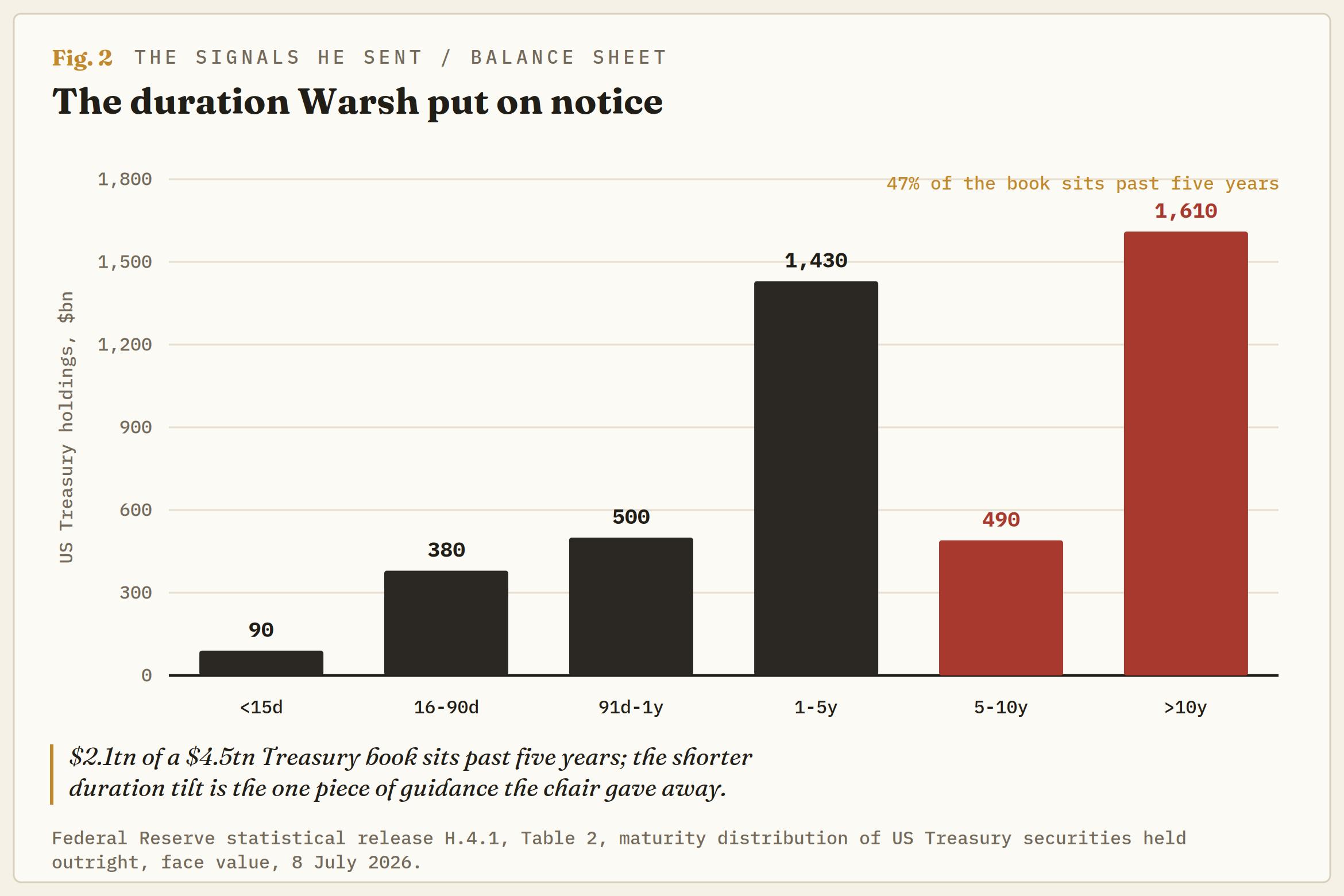

For a man allergic to guidance, Warsh left three signals on the table. The first was the balance sheet: He told the committee the Fed's holdings are too skewed toward long-dated Treasuries, which is forward guidance in everything but name, just aimed at the other tool. Taskforce two was chartered to review the asset mix; the chair has now pre-announced its finding, and a tilt toward shorter duration is a signal the long end can trade today.

The second was the target. At 15:48 GMT he said he is doubling down on 2%, and two minutes later that the broader price stability objective remains in the back of his mind, with further reforms possible. Read together: The number is safe, the framework is not. Taskforce five was told to weigh a range of ideas for delivering price stability, and the chair has just confirmed the range includes the definition itself.

The third was territorial. Dollar liquidity swap lines, he said, are part of monetary policy; the Treasury's Exchange Stabilization Fund (ESF) can run swap lines unrelated to the Fed's. That is a border, drawn politely, with the administration that appointed him, on the same morning he assured Representative Nydia Velazquez that he works for an independent central bank and told Representative Gregory Meeks the Fed would hold its course even if the White House publicly turned on it. The independence answers were scripted. The swap-line demarcation was policy.

What the prepared text glossed

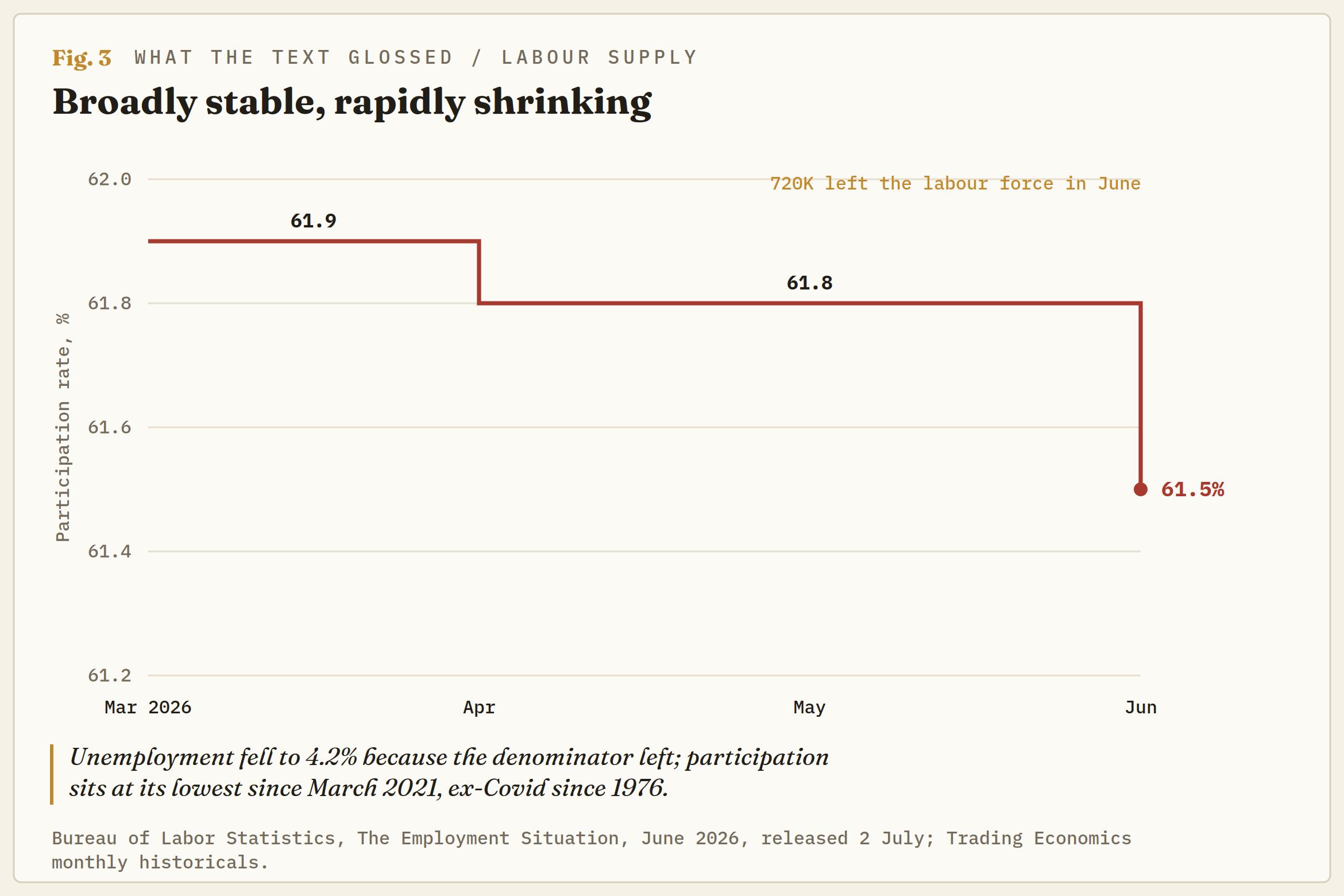

Two claims deserve the asterisk the testimony withheld. The labour market was described as broadly stable, with unemployment low and little changed. The 4.2% rate printed in June because participation fell to 61.5%, its lowest since March 2021, with roughly 720K people leaving the workforce in a single month. Stable is one word for a jobless rate propped up by a shrinking denominator.

The AI section stayed sunny. Investment is the most striking feature of the economy, equipment spending up about 8% YoY to Q1 and high-tech categories near 25%. In the second hour Warsh offered that AI will augment work rather than replace it: disruptive near term, job-creating after. His committee is less certain: June's Minutes had participants flagging AI infrastructure demand as inflationary while the chair publicly calls the technology net disinflationary. The prepared text retreated to monitoring the implications, which is what a truce sounds like when one side chairs the meeting.

Wednesday's rematch

The Senate Banking Committee gets its three hours from 14:00 GMT Wednesday, minutes after June's Producer Price Index (PPI) prints. May's PPI ran 6.5% YoY with roughly 80% of the monthly advance traced to energy, so the same peace-dividend arithmetic applies: A soft June pipeline print hardens the hold case and makes Warsh's second session easier. A hot core reading is Waller's trigger, live before the chair reaches the witness table.

The framework into the July 28-29 meeting is simple. The hold sits at 86% and the hike tail near 14%. A soft PPI and any ceasefire-four headline bury the tail, while a hot core print, a Hormuz still shut at month-end, and the crude rebound feeding into July's CPI re-arm it.

No SEP attaches to this meeting, so there are no dots to referee the family fight, and a 130-word statement cannot carry nuance even if the committee wanted it to. That leaves the speakers, the data, and a Chair who told Congress to its face that guidance is not his business. Markets were promised they would trade the data instead of the Fed. Tuesday delivered the fine print: when the data whipsaws, everything else does too, and the shock absorbers have been removed by design.

Author

Joshua Gibson

FXStreet

Joshua joins the FXStreet team as an Economics and Finance double major from Vancouver Island University with twelve years' experience as an independent trader focusing on technical analysis.