The RBI’s problem with the Indian Rupee has no easy fix

The Indian Rupee’s drama continues despite the RBI’s recent aggressive interventions and regulatory curbs. While these actions have caused the sharpest single-day gains in years, their effect has been wiped out in a matter of days. So why is every RBI move failing to break the Rupee’s downtrend?

The Indian Rupee has slumped nearly 5% vs the US Dollar in 2026, hitting an all-time low of 95.53 this week.

The RBI has been trying to stabilize the currency, but the results have been mixed, to say it politely. Let’s review first everything (or everything we know) the RBI has done:

Direct market intervention

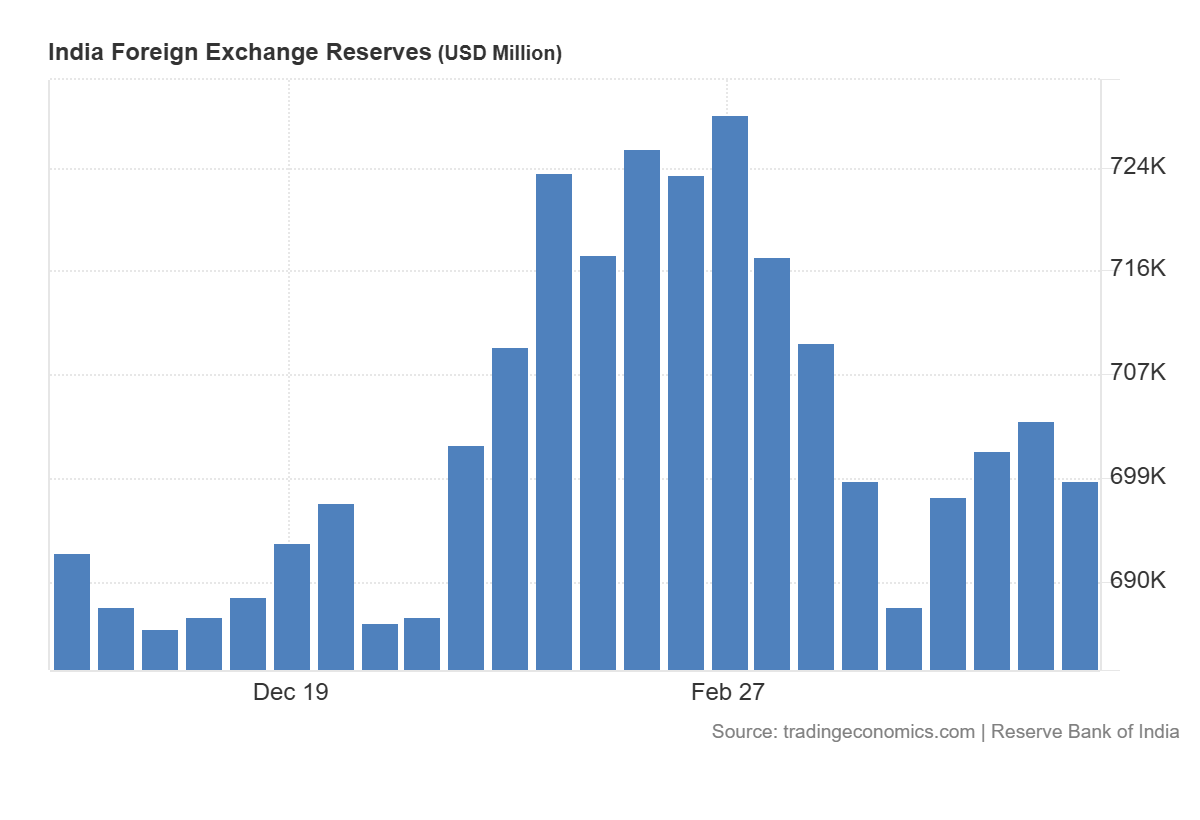

The RBI utilized its substantial forex reserves to intervene in spot and forward markets, selling USD to curb excessive volatility and defend the falling INR. In fact, India's forex reserves dropped from a peak of $728.5 billion to roughly $698 billion as of April 2026, due to continued intervention. Reserves serve as a financial safety net during times of economic instability, external shocks, and volatile currency markets. However, aggressive usage risks depleting buffers against future, more severe economic shocks.

Net open position cap

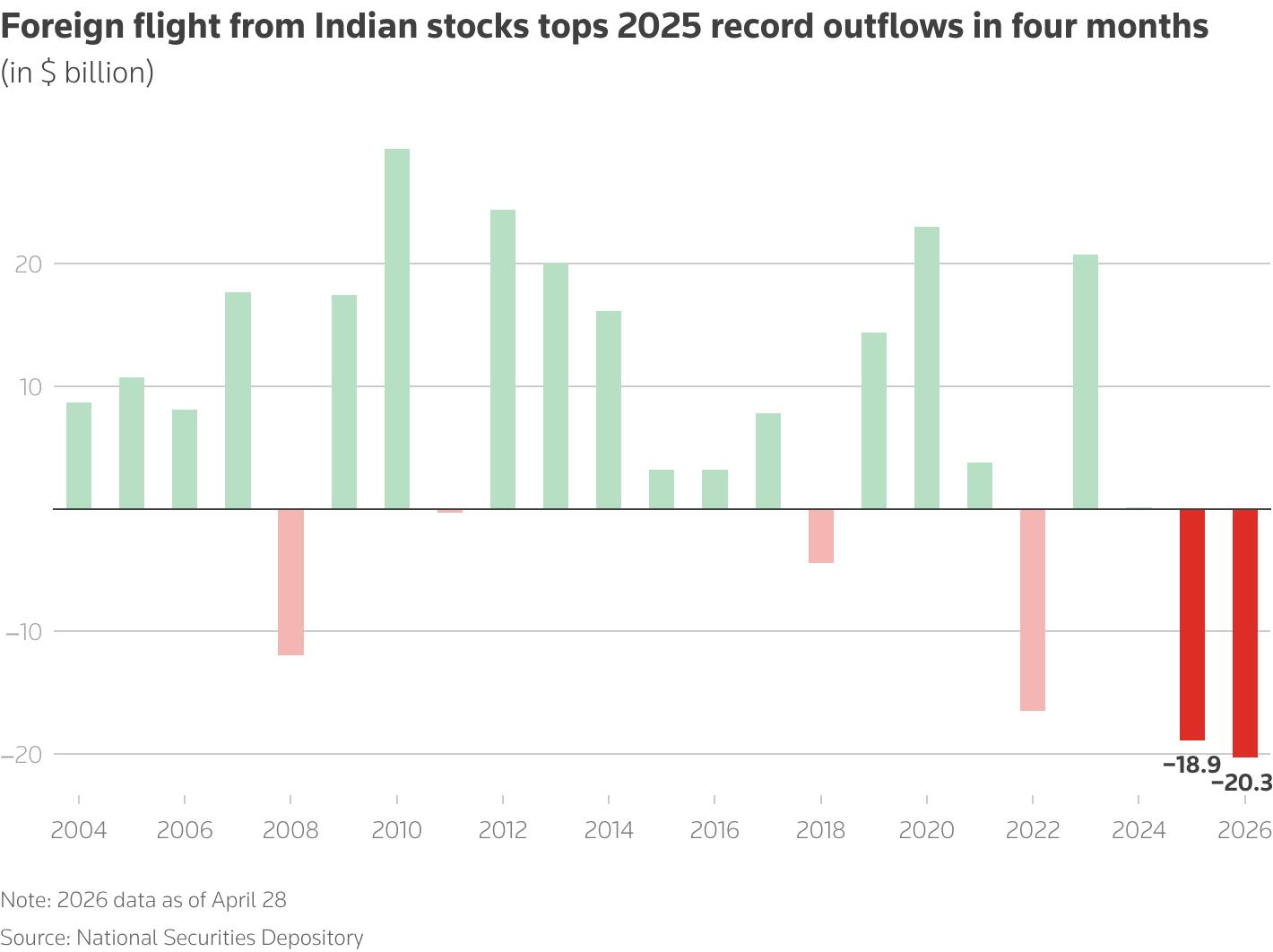

To reduce pressure on FX reserves, the RBI mandated all Authorized Dealer (AD) banks to cap their net open position in onshore currency markets to $100 million at the end of each business day, effective April 10. The move, however, does little to support the INR amid structural pressures stemming from persistent capital outflows. In fact, foreign portfolio investors (FPIs) pulled out $7.28 billion from Indian equities in April 2026, marking a second straight month of heavy selling after March's record outflow of $12.66 billion.

Non-deliverable forward (NDF) regulation

The RBI has barred banks from offering, trading, or facilitating INR Non-Deliverable Forward (NDF) contracts, previously used to hedge offshore without physical delivery, to restrain speculative volatility. This successfully closed the channel that allowed companies to engage in arbitrage between the higher-priced offshore NDF and the onshore market. Meanwhile, Indian importers have been buying USD at favourable prices, overwhelming tactical regulatory moves, and failing to stop the broader downward trend for the INR.

Encouraging refiners to utilize a specialized FX credit line

To prevent the Rupee from falling further, the RBI asked state-run oil refiners to curb their spot USD purchases and instead use a special credit line for their foreign exchange needs. The RBI has previously directed Oil companies – the biggest buyers of USD – to channel their requirements through a single public sector bank to reduce the overall market impact and ease severe pressure on the domestic currency. However, what needs to change for INR is a more sustained period of capital inflows, which have already been lacking before the Iran war.

The INR problems are structural

The RBI's priority remains volatility management rather than defending a specific level, and the recent policies were aimed at trying to break one-way bets on the INR.

These bets are almost impossible to stop in the current context: a large and consistent outflow of foreign funds from Indian equity markets, intense demand for USD from Oil importers and high energy import costs. All these remain structural factors that should keep the INR – Asia's worst-performing currency – fundamentally pressured regardless of short-term intervention.

Good luck to the RBI.

Author

Haresh Menghani

FXStreet

Haresh Menghani is a detail-oriented professional with 10+ years of extensive experience in analysing the global financial markets.