The pound fell as British voters headed to the polls

Highlights:

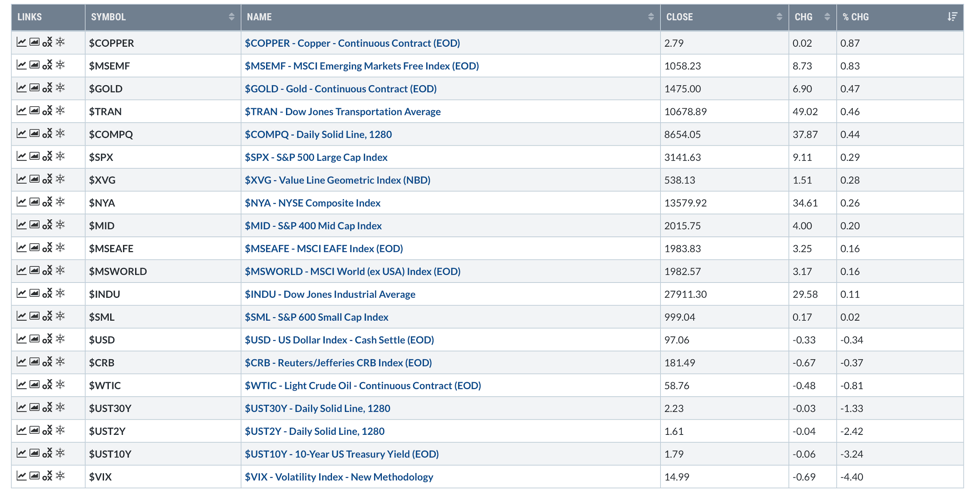

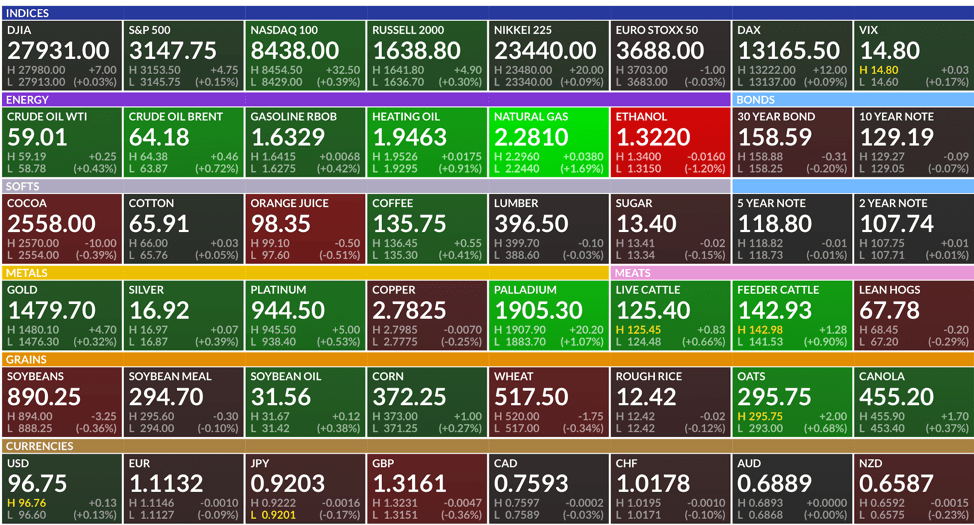

Market Summary: The S&P 500 finished higher yesterday, closing up 0.29%. Emerging markets were the top performing equity market segment, gaining 0.83%. Copper and Gold were also higher on Fed comments. The Fed seems intent on maintaining an accommodative stance until inflation becomes an issue.

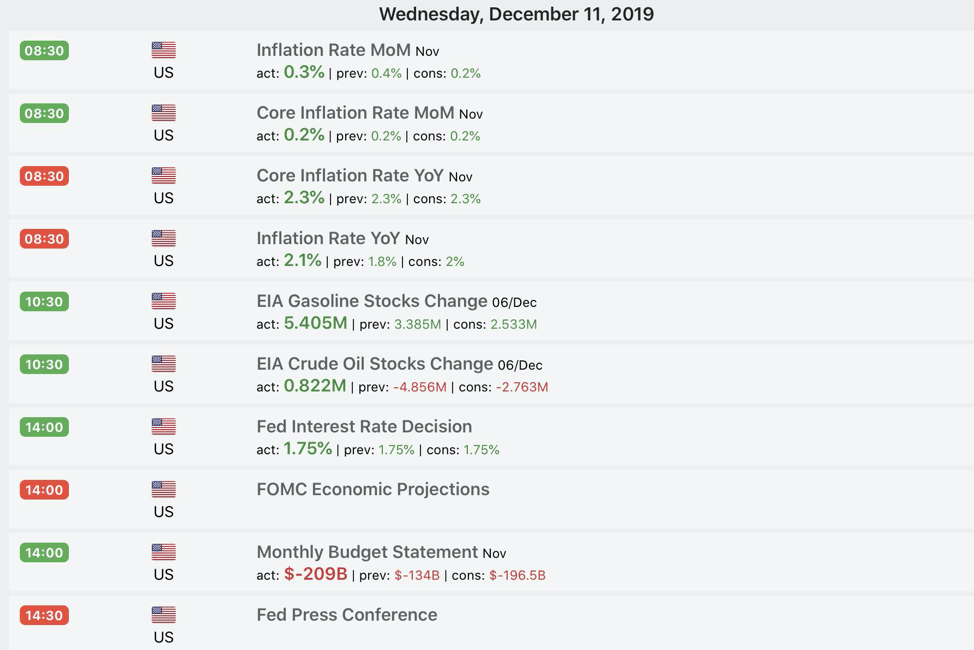

Economic Data: Speaking of inflation, yesterday we received inflation data. Month-over-month, the inflation rate was up 0.3%. On a year-over-year basis, inflation accelerated to 2.1%. That is up from 1.8% year-over-year from the month prior. The Federal Reserve kept interest rates at 1.75%.

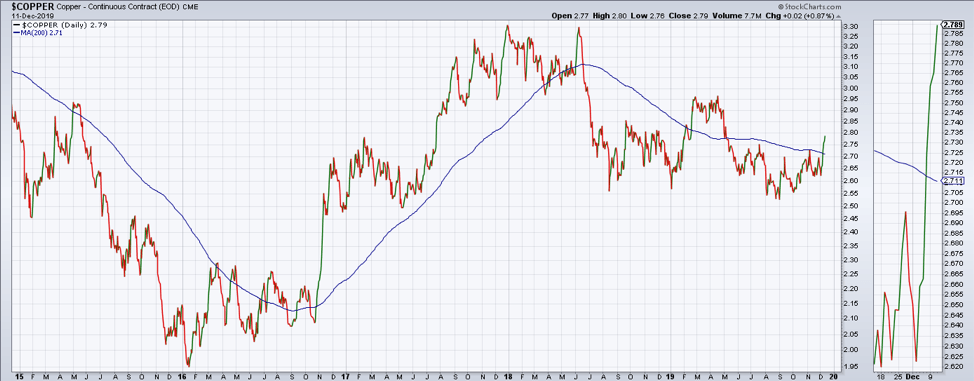

Copper: Copper moved higher as inflation expectations picked up yesterday. Copper is now back above its 200-day moving average. Does this mean that inflation is set to increase over the coming months? We will have to wait and see.

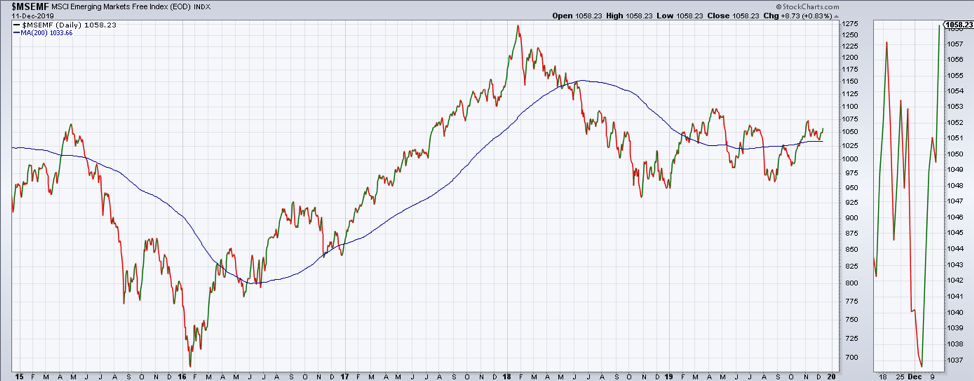

Emerging Markets: Emerging markets have successfully tested and bounced off the 200-day moving average. Emerging markets have failed to break out to new highs and are still negatively diverging from the S&P 500. If Emerging markets can breakout, that could imply that economic growth is accelerating around the world.

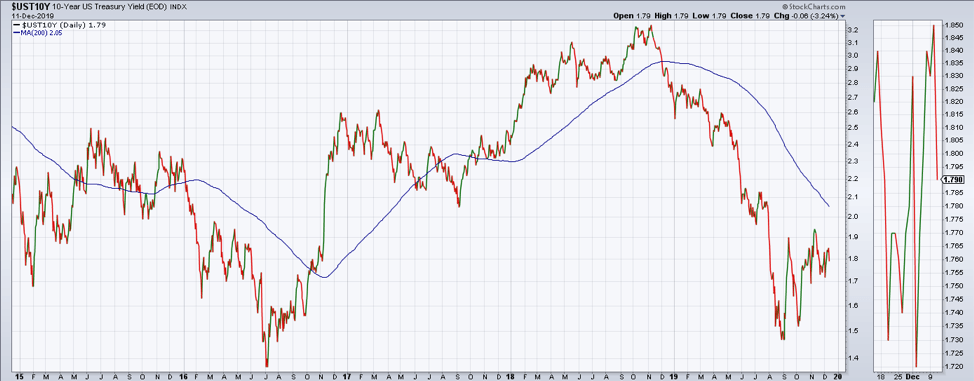

Bond Yields: Bond yields dropped yesterday, despite the pick-up in inflation expectations. Are market participants expecting that a more stagflationary scenario is going to play out? Growth slowing and inflation rising looks to be the current economic reality.

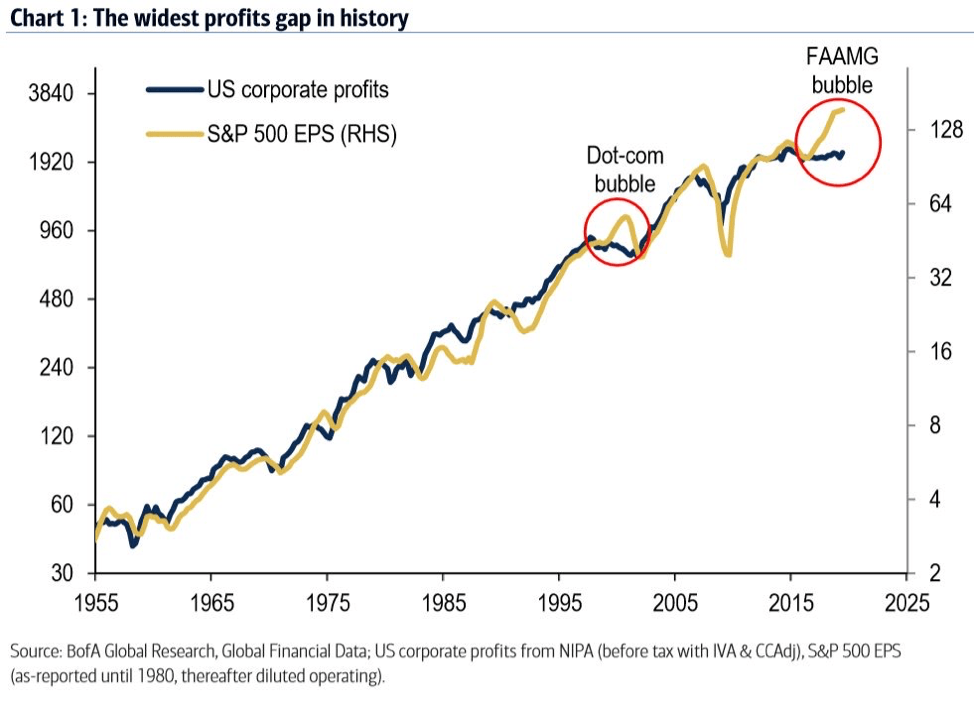

Chart of the Day: We have called attention to corporate profits and the disconnect with the S&P 500. It is clearly illustrated in the chart below by BofA Global Research. Corporate profits are now in a contraction, yet earnings per share continue to increase. This is very similar to what we saw in the Dot-com bubble. Hopefully this time is different.

Futures Summary:

News from Bloomberg:

Aramco surged for a second day, with its market value exceeding the $2 trillion mark—potentially making further share sales abroad more difficult. The amount was a goal of Saudi Crown Prince Mohammed bin Salman ahead of the IPO, which alienated global investors, many of whom said the stock was too expensive given governance and geopolitical concerns. Bernstein recommended investors take profit now.

Christine Lagarde will set the tone for her tenure as head of the European Central Bank. Her first policy meeting is unlikely to deliver a surprise but her press conference will give a flavor of her style. She may fire the starting gun on the bank's first strategic review since 2003 and recent comments about including climate change will probably face scrutiny. Economic forecasts may stay broadly the same. Check out our Decision Day Guide.

Voting in the U.K. is underway. The final polls before today suggested the Conservative lead over Labour may have narrowed a touch. Last night, Boris Johnson warned his supporters not to be complacent and Jeremy Corbyn attacked the media for downplaying his chance of victory. Polls close at 10 p.m. and the first results will start to come in at about 11. Here's an hour-by-hour guide.

Israel's political dysfunction means a third election in less than a year. The fractured parliament had until midnight to find someone who could form a governing coalition after Benjamin Netanyahu and Benny Gantz failed during months of horsetrading. The deadline passed with the deadlock intact. Early this morning, the Knesset officially disbanded itself and set elections for March 2.

U.S. stock-index futures edged up with equities in Europe as those in Asia rose. The euro was steady ahead of Lagarde's debut briefing, the pound fell as British voters headed to the polls and the dollar was up a smidge. Treasury yields recouped some of yesterday's losses. Gold and the yen edged lower, while oil climbed.

Author

Clint Sorenson, CFA, CMT

WealthShield