The outlook for a full recovery has been pushed out to late in 2021, and perhaps as far as 2024

Outlook:

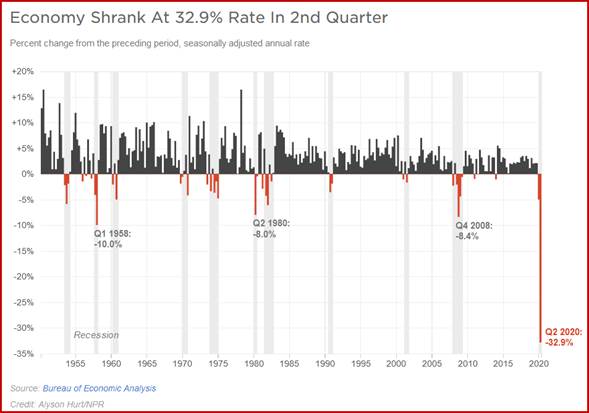

The US had a horrendous second quarter of contraction in GDP, -32.9%, hence (formally) recession. The eurozone has the same thing, with an annualized second quarter even worse than the US at about 40%. Recession was always the high-probability outcome, but some of the details are bone-chilling—private investment dropped 50%. Personal consumption dropped 35%. Savings rose 26%. Government spending rose 3%. See the Atlanta Fed Q2 chart—a drop of 32.1% (vs. the Census Bureau's 32.9%). The Atlanta Fed has moved on to Q3, which last Friday showed a Q3 estimate of 11.9%. We get a fresh version today.

This means the outlook is still "the bottom is in."

But that's not saying much, mostly because the outlook for full recovery to pre-pandemic levels has been pushed out to late in 2021 and perhaps as far as 2024. This is probably the scariest idea any economist has entertained short of world war.

We have yet to see the evictions/foreclosures, bankruptcies, and price consequences. We already know tourism and the hospitality industry were the first to suffer, but coming hot on their trail is retail, with as much as 40% of mom-and-pop stores closing permanently and malls a thing of the past. Of note is the oil industry. On Friday, Exxon and Chevron posted huge losses. One report says "Chevron fully erased the value of its Venezuela operations, amounting to $2.6 billion, and wrote down another $1.8 billion in assets due to lower commodities prices."

Forget their share prices—think about all the factors that point straight to lower oil prices for several years. It's not just the pandemic, but also the Russia-Saudi price war, whatever the hell that's all about, and the socio-political consequences for the Middle East producer states, which The Economist reports absolutely, positively need prices well over $40 just to survive as governments. Some needs prices over $100. As we all know to our rue, oil pricing permeates every blessed thing in every advanced economy. We must expect crises or at least fireworks.

So as we return to high-frequency data like ISM today and the employment report on Friday, keep in mind that the Big Picture is black, black, black. We can't expect equities to respond appropriately, but we can expect gold to take center stage and governments not to fail to notice. Gold is as much an advance indicator of "confidence in government" as any survey or poll. At a guess, loss of confidence in government suppresses activity as economic actors hide under the bed (like companies that plan capital spending). To the extent that Europe/Canada/Asia have done a better job at pandemic control than the US, they are the ones that will get the growth, not the US. Currencies follow growth. Forget taxes. Forget debt/GDP ratios. Forget debt—high debt is now a Good Thing as an emergency response. We can possibly cling to US yields being positive while everyone else is negative, but it's a slender lifeline.

The international finance world sees the US stumbling around all over the place, without decent testing and with a very large minority refusing to mask or social distance, which means one thing—the pandemic is not being managed correctly and will persist in the US for a longer time than elsewhere. Also important is that the US is balking at the second recovery finance package and lacks the social safety nets in place in "pinko" countries like the UK and the eurozone, so the consequences (evictions/foreclosures, bankruptcies, etc.) will be mitigated there and worse here.

Keep this perspective in mind when looking at charts of forecasted GDP recovery across multiple countries. For example, if China is really going to recover faster and bigger than elsewhere, that bodes well for Australia and not just data points like exports and PMI's but also retail sales, real estate and business confidence. A fat Chinese recovery means good news for Germany, too, via exports. We already see it coming: the FT reports Italy has a rise in the manufacturing sector for the first time in two years, with the Markit PMI index up 51.9 in July (from 47.5), more than forecast and led by domestic demand. We already had higher readings in France and the UK. Also, Spain delivered a gain today, too--53.5 in July (from 49.0), a bit of an offset to the dreadful GDP on Friday. In Asia, "Taiwan posted its best reading since January, making it the rare economy in the region crossing into expansionary territory. China's Caixin manufacturing PMI, a gauge more focused on smaller export-oriented firms, rose more than forecast and reached the highest level since January 2011" (Bloomberg).

Unless we get a Shock—and Trump is increasingly unable to invent shocks—the dollar can continue to slide, albeit with the important caveat that once historic levels are met, a correction is almost certainly inevitable, if only for the big players to clean out their closets of too big positions. Bloomberg has the most salient headline: "Dollar's slump is a warning to the U.S. to get virus under control." But Bloomberg misses an important point, perhaps the most important point—Trump wants a weak dollar, hence has some motivation not to take the actions that would bring the pandemic under control, like a national mask order. Besides, a return to "normal" is likely when the Senate returns today and ends up passing something resembling a second recovery spending bill. It won't be the $3 trillion the House wanted, but it won't be nothing, not with tens of millions of voters facing bankruptcy and even starvation.

Tidbits: For a few days, Trump stuck to his script in the pandemic briefings, and then he went nuts and re-tweeted crazy tweets, asserted masks don't work, complained that Fauci is more popular than he is, and said again that hydroxychloroquine is a cure, despite vast evidence it doesn't and can kill you. He also wondered about postponing the Nov 3 election, which even sycophant Republicans were quick to say he can't do, although he can still question the outcome, even if it's an overwhelming loss for him, claiming mail-in-ballots are sure to result in a rigged/invalid result (another lie).

The real problem with Trump trying to undermine the election is failure to fund the US Postal Service, which ran out of money and is being managed on an emergency basis. Mail-in ballots work only if the post office works, so undermining the post office is equivalent to sabotaging the election. If there is fraud and rigging in the mail-in balloting, it's by Trump (who himself votes by mail). It's not going unnoticed. House Speaker Pelosi is fulminating about it and even Pres Obama mentioned it at the funeral of an important Congressman. But complaining is not action: the new Postmaster General (a Trump donor) halted overtime pay for mail carriers and we already see delays in delivery. This raises the specter of not finding out the winner on election night and needing to wait weeks for the final count from the mailed ballots. We have been here before in Gore v. Bush and Gore was decent enough to quit. Trump, of course, doesn't have a shred of decency and will make the process a nightmare.

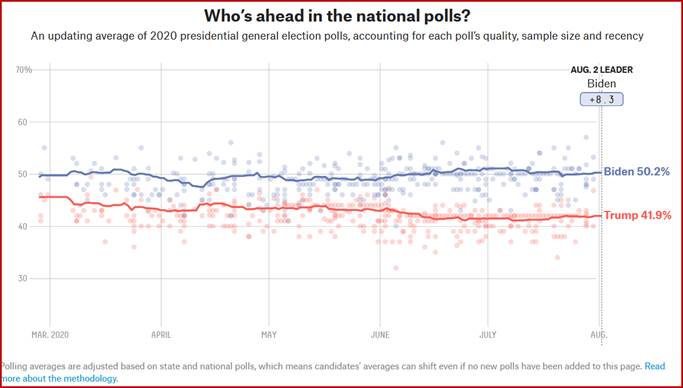

Why is Trump so desperate as to undermine the post office? Polls. The 538.com latest summary of multiple polls shows Biden leading by 8.3 points, a number that has been creeping higher since June.

The Economist, which uses a model plus polls, has Biden with 347 electoral votes and Trump with 191—when it takes 270 to win. But the model starts in March with Trump having fewer than 270 votes, and we're not sure that's credible.

Academics are modelling the various outcomes (big win for Biden, near-tie, etc.), and some skeptics say the polls are bad and Trump can still pull it off, especially if Biden stumbles. He has a chance to fall flat on his choice of VP, to be announced this week. Californians say it would be dumb to pick either of the two black ladies from California because California is blue to the bone, or to pick Susan Rice, because she worked for Obama and nobody wants to give Trump a chance to rant about that. Historically, the choice of VP does influence voting in the VP's state, but not by much. Probably the most interesting of the issues is whether Biden should refuse to debate, as proposed by a leading Republican campaign expert, because Trump lies so much that Biden can't win. And besides, Clinton was clearly the more competent and knowledgeable debater in 2016, and look what happened there.

It ain't over by a long shot. Trump's latest distraction—trying to derail TikTok as a leading wedge in the US-China cold war—has already bit the dirt. Evidently Microsoft talked Trump into allowing the acquisition of the English-speaking parts. (Oh, dear. Microsoft in the social media business! Having just wasted some six hours with an Outlook email problem, one can only despair.) But tigers and stripes—blaming China for everything from the coronavirus to job losses is still a vote-getter.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat