The only way the euro suffers is if the US gets stimulus and the EU does not

Outlook:

The Wall Street Journal's assessment of the probability of the second stimulus bill getting passed—the snowball's chance in hell—is probably wrong. Legislators, even the awful McConnell, can see the next election coming and worry they will lose the 2022 midterm, again, if they don't hand out some dough. Photos of long lines at food banks in formerly prosperous places are reminiscent of the Depression. Republican voters are deeply loyal, but not entirely unaware it's their party denying them food for their children. This may be at the margin but it's a wide margin.

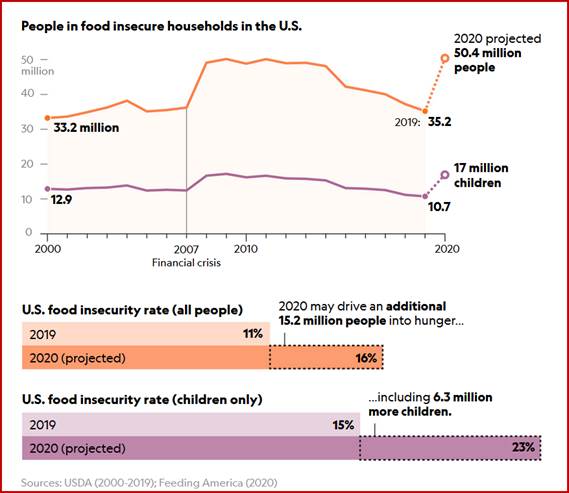

See the charts from the National Geographic. So-called food insecurity will rise to 50 million this year, an increase of 15 million persons, while 6.3 more children will go hungry. For the richest country in the world, this is a disgrace. The charity Feed America says the 50 million Americans going hungry is one in six and one in four of the population, almost 50% more than in 2019.

Bleeding heart liberal sentiment aside, there are wide and deep consequences of this economic development. First is the new impetus to get a second stimulus package as noted. Second is the penetrating waves of losses to manufacturers, importers and retailers of slumping consumption. We have to wait a few weeks for the official retail sales data, but so far the US shoppers spent 14% y/y less money on the 5-day discount holiday last week (including Black Friday and Cyber Monday). In-store shopping was down 37% y/y and online shopping failed to make up for it, up only 8%. Cyber Monday is the exception, with sales up 15% y/y for the "biggest day for online shopping in U.S. history" (WSJ). If we get a Christmas surge in Covid 19 cases arising from foolish socializing at Thanksgiving, the scientists' forecast of a dark winter will be right and drag the economy lower.

The Fed, of course, is watching all this, giving it a more dovish bias, especially in light of an inadequate fiscal response, of we get one at all before year-end. Timing counts, and both Fed chief Powell and incoming TreasSec Yellen know it. It's all very well to start making plans for post-inauguration initiatives, but to prevent a double-dip recession, we need action now. The next Fed meeting is Dec 10-11. Wait for it—chatter about some new ideas at the Fed.

Meanwhile, it's not entirely clear the ECB is as dovish as everyone thinks, especially if the budget does get through. The next ECB policy meeting is also on Dec 10.... We can get dueling central banks or we can get no action at all. In days of yore, by which we mean the dear departed Volcker, the phone lines were hot between Washington and Frankfurt. It's hard not to imagine Powell calling Lagarde. Are they going to "coordinate"? At a guess, yes. We may never hear about it until memoirs get written, but we can make sensible deductions. We imagine both sides get their fiscal boost and the central banks stand pat. Alternatively, one gets it and the other doesn't by the Dec 10 deadline, and the one without the fiscal boost is the one that cuts rates or increases QE or otherwise signals dovishness. Or they both fail to get the fiscal help and they both get more dovish, perhaps in sync.

This is not yet on the radar, but stay tuned. The only way the euro suffers is if the US gets stimulus and the EU does not.

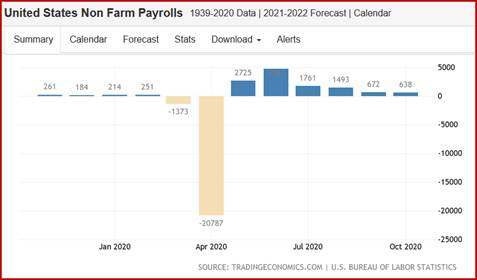

One of the biggest determinants of economic wellness, payrolls, is due Friday. Today we get the ADP estimate of the private sector component, expected at a gain of 420-430 million jobs vs. 365 million last month. Payrolls were a gain of 638,000 in October (from 672,000 revised in Sept), the smallest gain since the recovery started in May. It's not even close to recovering the record 20.787 million loss in April. Current payrolls forecasts are discouraging—Bloomberg has a mere 486,000. We will be getting more forecasts later today after the ADP results. TradingEconomics.com says the consensus forecast is 481,000 and its own forecast is 500,000.

As we feel compelled to repeat, the data is lousy because it fails to count so many unemployed and the millions working off the books, but we have to deal with what we've got. In fact, many more are no doubt working off the books, mitigating the rise in food insecurity and drop in spending mentioned above. That's a wild guess arising from local ads for gutter cleaning and yard work, so take it with a grain of salt.

Anyway, the ADP data today and the payrolls on Friday are likely going to appear low to okay, without triggering fear of that double dip recession that really is lurking around the corner. This is useful mostly in terms of failing to offer a drag on the stock market, and the stock market is our barometer of risk-on sentiment.

If the second stimulus fails again, if Trump refuses to sign the continuing resolution budget, if ADP and payrolls are seriously worse than built in—it's possible risk-off comes back and the dollar becomes a safe-haven again. Most analysts give this outcome a small probability, and instead expect further euro gains to be modest, with a little retracing and fiddling around sideways for a while until we get a bit more clarity.

Politics: Attorney General Barr announced the election had no sign of fraud, contradicting Trump and his crony lawyer Giuliani. This is the break in the dam, although it's too late—nearly a month after the election—and tens of millions of Trumpies now doubt the voting process. Dems kind of hope that means they will stop turning out, while acknowledging it's an unpatriotic thought. A top election official in Georgia (and a Republican) called out the president and Georgia senators for failing to condemn death threats against poll workers and the secretary of state, another Republican. Partisanship has gone way too far and "it has to stop."

Separately, a new court case (with names and details redacted) was released charging somebody with trying to bribe Trump for a pardon, but no details yet. The whole subject of pardons is in the air; it's a dead cert Trump will be pardoning people left and right, including probably himself, even though Nixon himself doubted self-pardoning is legal. The NYT reports he has been exploring pardons for his children and Rudy, but there's a giant problem in doing that: he would have to name what crimes he is pardoning them from having committed. A blanket pardon won't cut the mustard, according to some legal experts. (Pretty funny, really). Bottom line—more messy stuff from Trump, some of it possibly dangerous and all of it ridiculous and pathetic. We have 49 days to the inauguration.

Equally important is the 34-days to the Georgia Senate run-off election. If the Dems gain those two seats, we can get some real action. We may have to hold our noses for some of it, but nothing like holding our noses for what Trump did—Muslim ban; children in cages; dumping the Paris Accord, TPP and threatening NATO; McCain not a hero, and "my button is bigger than Kim Jong Un's button." To name just a few.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat