The Monetary Sentinel: The resumption of the easing cycle?

Central banks are adjusting their perspectives in response to persistent worries about the global economy caused by the trade strategy implemented by the Trump administration.

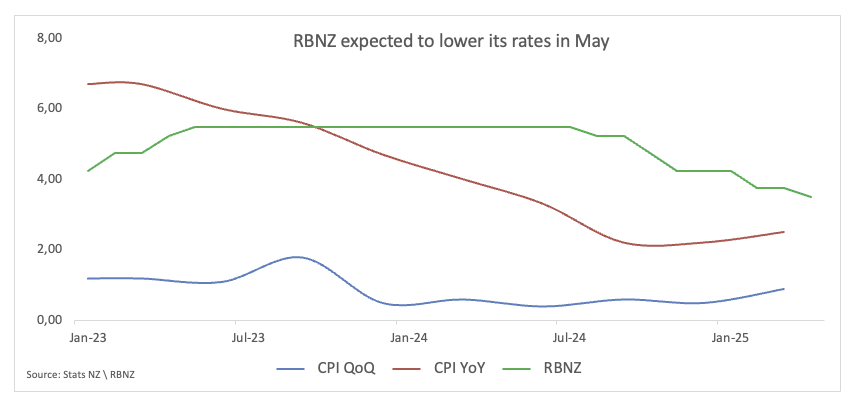

Reserve Bank of New Zealand (RBNZ) – 3.50%

Last week, the RBNZ issued a warning over the possible impact of new US tariffs on world supply chains and thus on the state of the national economy. In fact, Governor Christian Hawkesby indicated before a parliamentary committee certain local businesses might suffer long-term difficulties and were particularly sensitive to the changing trade policies.

Based on the lessons learnt during the epidemic, Hawkesby observed that supply-side shocks usually have a long-lasting and severe character. Furthermore, he said, a lot of unknown is regarding how the global economic structure will adjust to these changing dynamics.

With inflation now safely inside the bank’s 1–3% goal zone and unemployment climbing to a more than four-year high of 5.1%, the bank seems to have leeway to continue its easing cycle.

It is worth noting that should the bank stick to its present course, it may provide up to 275 basis points of cuts, the most aggressive easing campaign since the global financial crisis of 2008, well ahead of Australia's expected 100 basis point reduction.

Upcoming Decision: May 28

Consensus: 25 basis point cut

FX Outlook: NZD/USD rose to new two-week highs on Friday, approaching the key 0.6000 hurdle following the intense sell-off in the US Dollar. So far, while the pair seems to have embarked on a consolidative range, extra gains remain on the table while above its key 200-day SMA around 0.5880.

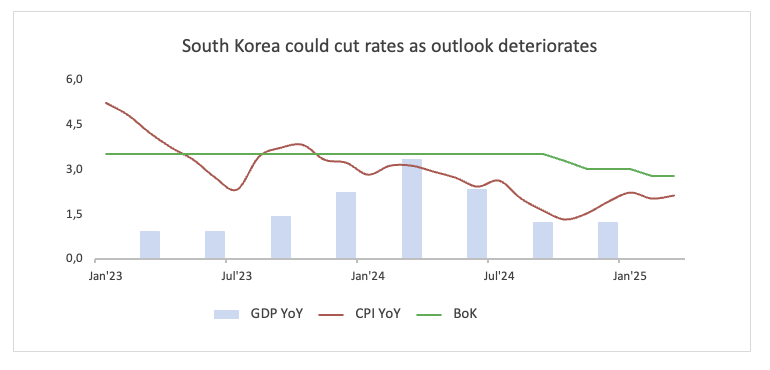

Bank of Korea (BoK) – 2.75%

Based on Minutes from the April meeting published, most members of the board feel that economic headwinds are developing quicker than predicted, therefore supporting the case for interest rate decreases.

One board member pointed out that preemptive rate reduction were becoming more important as growth probably would underfit prior estimates. The member noted, based on the minutes from the April 17 policy review, "Given the slowdown, there's growing urgency to act sooner rather than later."

At that event, the BoK maintained its benchmark rate constant at 2.75%, as generally expected, but noted the possibility of a May rate reduction. A major factor influencing the situation the board mentioned was "significant" negative risks related to US President Donald Trump's broad tariff policies.

Upcoming Decision: May 29

Consensus: 25 basis point cut

FX Outlook: Starting in April, the South Korean Won (KRW) has been strengthening consistently. Against that, USD/KRW fell to values last seen in October 2024 around 1,365 on Friday. Rising anxiety over US trade policy has been almost entirely responsible for the notable increase in Asian FX as of late; this trend might potentially support another drop in the pair in the coming few months.

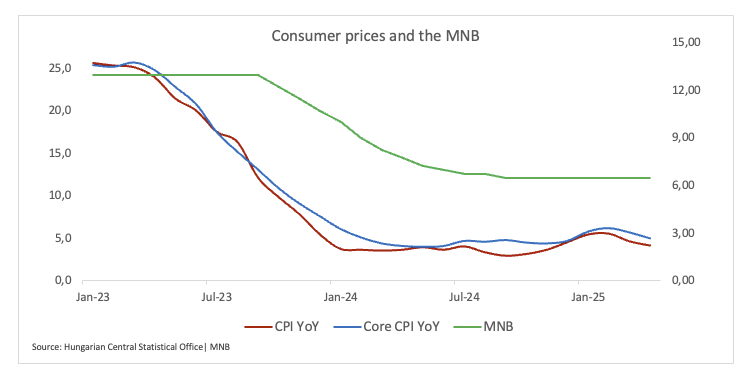

Hungarian Central Bank (MNB) – 6.50%

The MNB is predicted to hold its present interest rate for yet another meeting this week as depressing economic performance, ongoing budgetary concerns, and the possible consequences of trade tariffs are expected to continue influencing the existing state of affairs.

Mihály Varga, governor of the MNB, said last week that if the bank is to reach its aim sustainably, inflation expectations still need to be securely anchored. He cautioned that although the battle against inflation is still ongoing and underlined that rate reductions are not on the agenda for now, despite the negative projection of economic development.

Varga's comments follow the central bank's April decision to maintain its benchmark rate unaltered, a choice supported by the monetary policy committee generally. Officials underlined at the time the importance of a slow and patient attitude, therefore indicating that they are not hurried to change just yet.

Moreover, with elections approaching next year, growing domestic expenditure runs danger, and an increasing budget deficit clouds the picture.

Upcoming Decision: May 27

Consensus: Hold

FX Outlook: The Hungarian Forint (HUF) has been on a tear since the beginning of the new trading year, prompting EUR/HUF to recede to multi-month troughs around 350.00 in late April, embarking on a consolidative phase since then. As long as the cross navigates below its 200-day SMA around 373.60, further pullbacks should not be ruled out.

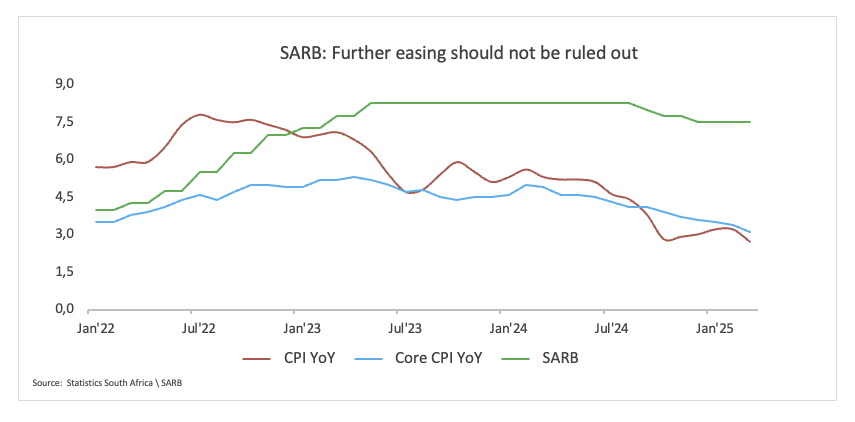

South Africa Reserve Bank (SARB) – 7.50%

As the South African Reserve Bank (SARB) prepares to meet this week, all eyes are on whether it will hold the line, or seize the opportunity to ease.

Back in March, the central bank struck a cautious tone, warning that the space for rate cuts was narrowing amid a volatile global backdrop. The US-led trade wars were flagged as a major risk, with SARB noting the potential for knock-on effects at home.

Fast-forward to today, and the picture looks a little different. Inflation has dipped to 3.6%, comfortably below last year’s 4.4% and now outside the lower end of the 3–6% target range. The rand, meanwhile, is at its firmest in months. Domestically, the finance minister has also shelved a contentious VAT hike in his revised budget, reducing pressure on households and shifting the fiscal conversation.

Despite these shifts, market consensus still leans towards a hold. But with inflation soft, the currency strong, and domestic uncertainty easing somewhat, the door to a 25 basis point rate cut is more open than it has been in months. Whether SARB walks through it remains to be seen.

Upcoming Decision: May 29

Consensus: Hold

FX Outlook: The South African Rand (ZAR) extended its bullish mood on Friday, sending USD/ZAR to fresh five-month lows around 17.8000 and further south of its key 200-day SMA around 18.1500. Further improvement in the sentiment surrounding gold coupled with extra weakness in the US Dollar should keep the downside pressure around the pair well and sound for the time being.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.