The FOMC to announce a tapering in its asset purchases later this year

In recent days, the seven-day moving average of new COVID cases has dropped to about 90K for the first time since July, after exceeding 170K at its September 13 peak around the timing of our previous forecast update.

As one problem fades, another has gotten worse. Supply chain issues have been with us to varying degrees since the pandemic first broke out in March 2020, but in recent weeks, supply chains have shifted from merely a major headache to an outright crisis.

COVID case spikes overseas and the resulting absenteeism at far-flung ports and factories have had a lagged effect on the production pipeline all over the world.

The result is the “everything shortage,” which is offering a fast education on the far-reaching impacts of global trade to everyone from big business owners to ordinary consumers.

The logjam will push back the timing of some growth we had anticipated later this year and early next year, which will weigh on our forecast for 2022, although most of that growth shows up later in the forecast.

We now forecast that real GDP will grow 4.0% in 2022, down from 4.5% last month. Our outlook for 2023 looks for output to grow at an above-trend rate of 3.2% that year, up from 3.0% previously.

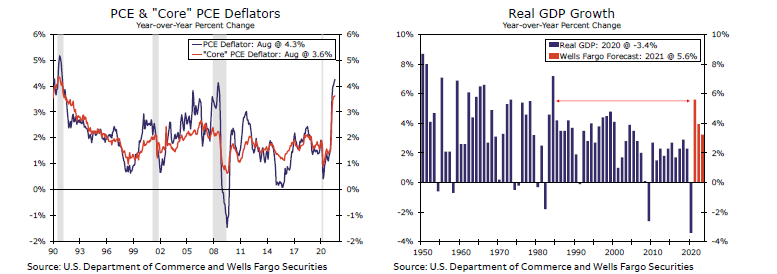

The shortages and longer wait times are having an effect on consumer prices. Headline inflation, as measured by the PCE deflator, rose to 4.3% on a year-over-year basis (see chart), with core PCE deflator coming in at 3.6%. These measures reflect the highest headline and core inflation in more than 30 years.

We expect the FOMC to announce a tapering in its asset purchases later this year, which should contribute to the upward creep in long-term interest rates that we will forecast in coming quarters.

Rate hikes are not on the docket, however, as the FOMC will likely wait until the labor market is nearing "maximum" employment until it begins to hike rates, a condition that we do not believe will be met until the second half of 2023. We forecast that the committee will raise its target range for the fed funds rate 75 bps in the last two quarters of 2023.

Supply chain reaction

While it may be true that hope springs eternal, if the past 20 months have taught us anything, it is that hopes can be dashed in unending ways as well. A surge in the Delta variant was the primary culprit in our downward revision to our growth forecast in September. This month, we are paring back expectations again, but this time it is the worsening backdrop for supply chains that is to blame. There is an upshot though: while some of the activity suppressed by shortages is lost forever, a lot of it is merely delayed. Our full-year growth forecast for 2022 at 4.0% is now half a percentage point lower than it was a month ago, but we see scope for a pickup in activity as supply chains normalize, perhaps as soon as the second half of next year. In the meantime, the shortages mean even higher prices, which has implications for Fed policy.

Although the virus case counts are again moving lower, Americans have generally remained more cautious, perhaps even growing leery of apparent improvements after so many false-dawns throughout this pandemic. The University of Michigan index of consumer sentiment rose to 72.8 in September, but that comes after having dipped to its lowest level since 2011 in August, while the Conference Board's index of consumer confidence fell in September to its lowest level since last winter.

Despite these setbacks in sentiment, retail sales shot up 0.7% in August. Control group sales posted a 2.5% gain, the biggest since stimulus checks went out in March this year. We see some gains reflecting catch-up in stores where inventory was previously picked clean and others tied perhaps to the Child Tax Credits and back-to-school spending. A key factor to keep in mind is that prices are playing a role here, and after adjusting for inflation, the spending gains are more modest. The retail sales figures are not adjusted for price changes, but the figures in the personal income and spending report are. After adjusting for inflation, the 0.8% nominal increase in personal spending was cut in half to a 0.4% real increase. That was not enough to offset the 0.5% decline in real PCE revealed in the revision to July. It is for this reason that we anticipate real consumer spending growth will come in at just a scant 0.7% increase in the third quarter.

While we remain concerned about COVID’s impact on consumer spending, most individuals seem to be going about their daily routines, albeit perhaps not with the same vigor as they did earlier in the summer when the pandemic appeared to be winding down. In short, significant retrenchment in consumer spending does not appear likely unless the new case count shoots markedly higher from its current level. We forecast that real GDP in the United States will grow 5.6% in 2021 (see chart). That still marks the strongest full year for U.S. economic growth since 1984, but it is a meaningful downgrade from the 7.3% rate that we forecasted in early June when new COVID cases were averaging roughly 15K per day and before prospects for a more vibrant rebound were ruined by the Delta variant.

Author

Wells Fargo Research Team

Wells Fargo