The Fed is thought to be thinking of 'extending the expansion'

Outlook:

The way in which central banks speak of their policy choices is shifting. Instead of preventing a major slowdown that could lead to recession, the Fed is thought to be thinking of “extending the expansion.” We bet Greenspan laughed when he heard that one—it’s exactly the kind of thing he would try to get away with. Similarly, Draghi spoke not so much of deteriorating conditions as about the absence of robustness. Low inflation and other depressing data is a function of expectations of bad things to come, like US tariffs.

While it seems clear an ECB rate cut and/or resumption of QE is in the cards for the second half—which begins next week—we don’t know what the trigger might be. Let’s make a guess and imagine that if in August, when Trump is looking for something to distract attention from his latest scandal or outrage, it’s tariffs on European autos. Heaven knows Trump has signaled it for long enough. Mr. Draghi could move immediately instead of keeping the two things disconnected as central banks would normally do. In other words, the central banks are starting to act less like economists (endlessly waiting for data to confirm sometimes iffy theories) and more like financiers. It’s not clear this is a bad thing. Central banks pretend they don’t look at stock market responses to their policies, but don’t be silly—of course they do. Stock markets are a long-standing “factor” in their own right.

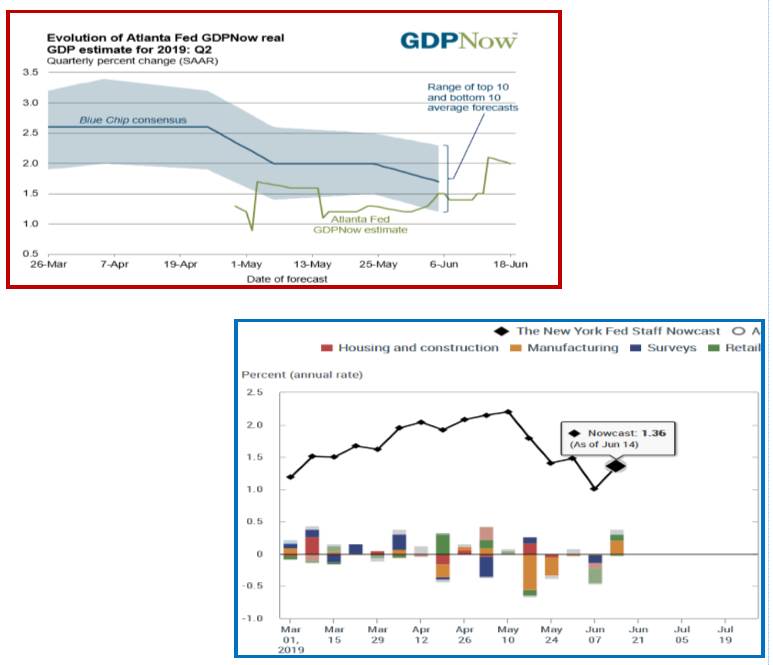

As for this particular case, we could end up having two central banks cutting interest rates in response to an ad hoc imposition of tariffs with no underlying analysis or plan (and thus no idea at all of how economic effects might develop). In the case of the US, the economic data does not yet support a cut. See the Atlanta and NY Fed’s forecasts. The Atlanta Fed sees the bottom is in and Q2 will end up delivering 2%. Granted, it was 2.1% last week, but never mind. We get the next one next Wednesday. Meanwhile, the NY Fed is a bit gloomier with 1.4%, but again, the chart shows the bottom is in.

One data point in each case can’t fairly be credited as a bottom, but the point here is that if the Fed promises a cut in July or September, it’s not doing it on data but rather on expected data (and the expectation is based roughly on events Trump hasn’t yet made up out of whole cloth). They are talking about the worst-case scenarios in the Fed’s economists room and you can bet Mr. Powell and Mr. Draghi are talking about worst-case scenarios on the phone, although Trump would go ballistic if he knew they were in any way coordinating policy.

Bottom line, at 2 pm today we will all be listening to hear the word “patience.” If it’s there, Powell’s head is still on the chopping block. If the word is missing, we are getting a rate cut.

The combination of dovish Fed and a “fair” China trade deal should drive the dollar down—if we think it was risk aversion holding it up in the first place. We are not so sure. The dollar has other legs to stand on, including being able to draw in foreign capital, a mostly just legal system, an educated labor force, social stability, a yield advantage (if diminishing), a decent banking sector, etc. After all, immigrants are still clamoring to get in, something you can’t say about Russia or China. And China may be more motivated to get a trade deal now that Hong Kong has rejected it so dramatically—2 million persons rejecting Chinese law out of a population of 7 million (well, probably more, but that’s the official number).

It’s ridiculous to think a meeting between Trump and Xi next week is going to re-shape the global economy but that’s exactly what everyone is counting on. If the president were someone sane and reasonable, it might not be a bad idea. Nixon changed the world with one visit to China a few decades ago. But Trump is a guy who says the Queen never had a such a good time in 25 years as she had meeting him. He’s nuts as well as vain, venal, and vulgar. So, while it may appear riskiness is on the wane, it will almost certainly be short-lived. Trump will do or say something else horrific over the course of the summer. It ain’t over until the Fat Man leaves the stage.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a free trial, please write to [email protected] and you will be added to the mailing list..

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat