The Eurozone Sovereign Debt Crisis.

Financial markets are about two things: Return and Risk. Until recently, in a world where the low interest rate environment was the overarching theme, it was the Return, the so called "search for yield" which seemed to dominate the psyche of investors, not least because central banks gave the impression that they were willing to handle the downside market risks in order to fuel an economic recovery which has proved quite fragile in the aftermath of the Global Financial Crisis and of the Eurozone Sovereign Debt Crisis. Things may be changing, however, as a Revolution seems to unravel before our eyes: it's the Revolution of Risk over Return.

As with most Revolutions, it's almost impossible to perfectly identify where the first spark came from, especially that we have many candidates aligned. Looking at the US alone, we have President Donald Trump stepping up protectionist trade policies, the Federal Reserve stepping up the retrenchment from its extraordinary monetary stimulus through a combination of balance sheet reduction and accelerating interest rate hikes, a policy that comes in stark contrast to the Republican administration's fiscal policy loosening implemented at the beginning of this year. In Europe, too, we have a potential reincarnation of the Core-Periphery dichotomy, sparked by Italy's choice of a populist government, having fiscal expansion and Euro bashing at the core of its new economic program. Geopolitical ping-pong (the US-North Korean stand-off turned soap opera vs the Iran nuclear deal turned into a hand slap game) and rising political/policy uncertainty in some important Emerging Markets (Turkey, Argentina, Brasil) are also good candidates, at least for a supporting role in the unfolding drama.

But if we don't know exactly where and when the spark was ignited, we know that the appreciation of the US dollar was clearly involved in the making of the fire which burned through most of the investor goodwill towards Emerging Markets since April. We also know that capital outflows from Emerging Markets, like wildfires, can take a life of their own even when the US dollar will stop depreciating. Finally, we Romanians should know that even if it remains behind the Great Money Wall erected by the ECB and the Great Ignorance Wall which we have ourselves built with our domestic policies in order to keep investors out, this fire has enough heat to make us sweat. It will perhaps not burn the house down, but it can definitely melt the icing on our consumption cake, if not fully transform it into a cake soup.

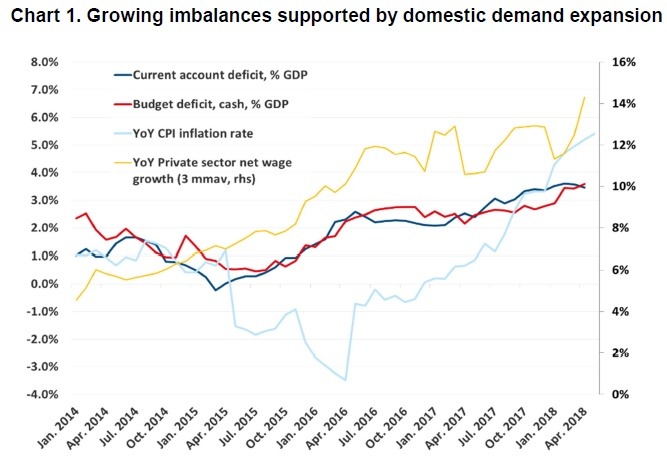

This is because we're already quite hot. Even after being revised down and with a dismal first quarter, Romania's GDP probably still remains in excess demand territory, as confirmed by the ongoing wage growth pressure and the continuously expanding current account deficit (see Chart 1). Then more recently we also have the hot weather, which can spell trouble for the agricultural sector. Already in May we have an upside surprise in case of food prices, which comes at a time when annual CPI inflation should have reached its peak (now at 5.4%, versus 5.2% expected). A hot and dry summer can add insult to injury: it can cause an output shock for agricultural products which will not only lift food prices and push inflation well beyond 6%, but it can also place an extra burden on GDP growth at a time when it is already down and flat (0.04% in 18Q1 over 17Q4). This is not yet our base scenario, but risks are mounting in that direction, such that inflation can end the year above and growth below our current projections of 3.7% and 4.1%, respectively. And beware, in a case of an agricultural output shock which is essentially a supply shock, a slowing GDP growth will not mean that excess demand is over and out. On the contrary, negative effects similar to the impact of excess demand will be present in the form of higher prices and increased pressure on the external deficit, as supply shortfall could be covered by rising food imports.

Author

Erste Bank Research Team

Erste Bank

At Erste Group we greatly value transparency. Our Investor Relations team strives to provide comprehensive information with frequent updates to ensure that the details on these pages are always current.