The Dow Jones Industrial Average (DIA) closed higher by 0.20%

Highlights:

Market Recap: The stock market finished the day mixed. The Dow Jones Industrial Average (DIA) closed higher by 0.20%. The S&P 500 (IVV) finished down -0.04%. Emerging markets were the worst performers (EEM), closing lower by -1.29%. The 10-year Treasury note yield closed higher as well, knocking down Treasury bond prices. The U.S. dollar closed higher, causing commodities and oil to move lower.

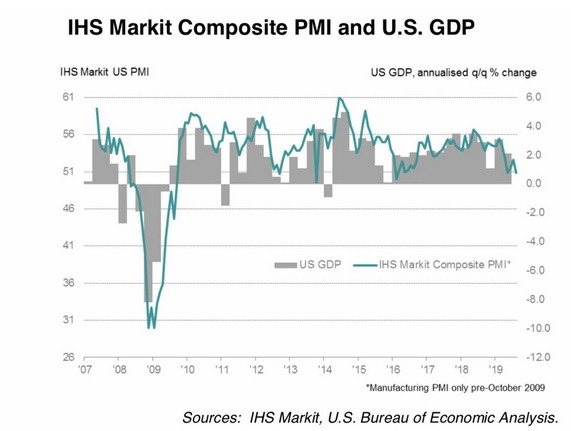

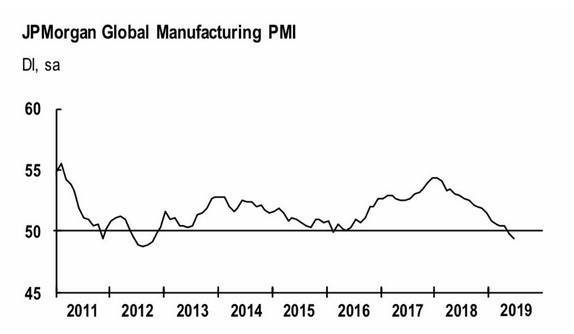

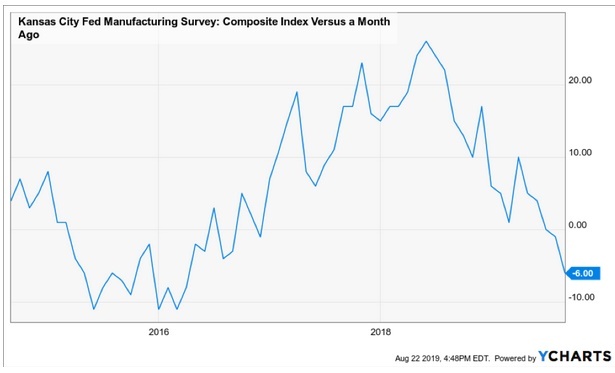

Economic Data: Stocks started out higher on the day before reversing course after the IHS Markit Manufacturing PMI showed a contraction in economic activity. Furthermore, the JP Morgan Global Manufacturing PMI also fell below 50. 50 is the line of demarcation whereby the manufacturing sector is said to be expanding above 50 and contracting below. Recession fears continue to rise as the data worsens globally. Whether we are in a recession or not doesn’t really matter. The fact of the matter is that economic growth continues to slow, and we know that means challenging times for risky assets. The Kansas City Fed Composite also contracted to -6 this past month.

10-year yields: Are interest rates set to bounce significantly? Yields are super oversold and bonds overbought. Yields are less overbought after a few sessions of increase. However, the 10-year yield is over 30% below its 200-day moving average. That is pretty wide historically. A consolidation is expected.

Oil: Oil remains in a negative trend despite bouncing from support. Oil is forming a descending triangle. Descending triangles show that supply is coming in at lower and lower levels. If this is resolved lower, it could mean a substantial decline in crude oil. It is illustrative of the uncertainty present in the market currently.

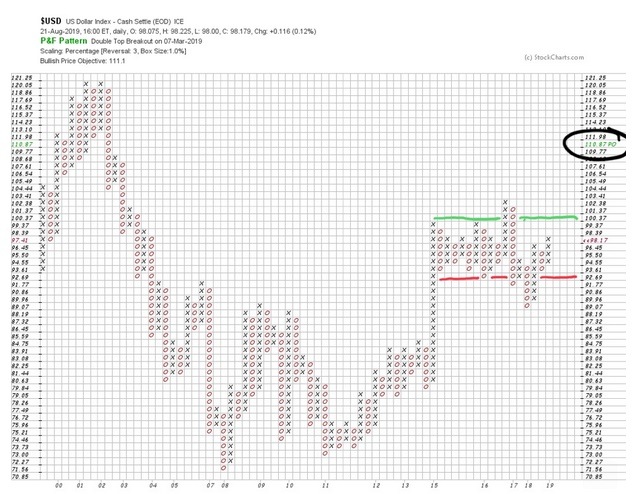

U.S. Dollar: The U.S. dollar remains in a range between 92 and 100. It is nearing the upper end of that range (98.17) and is on a point and figure chart buy signal. The price target is 110.87. If this is accurate, it could be significantly deflationary.

High Yield versus Treasuries: High yield bonds have bounced from short-term oversold levels so far this week. The trend is still firmly risk-off. Will the Fed announcement create more volatility in this ratio? This inter-market relationship is concerning for risky assets.

Futures Summary:

News from Bloomberg:

Stocks rose with Treasury yields and the dollar as investors await Jerome Powell's Jackson Hole speech at 10 a.m. ET. His words will be closely watched as he faces pressure from President Trump to cut rates, while some regional Fed chiefs have sounded more hawkish. Mark Carney speaks at 3 p.m. ET. Mario Draghi and Haruhiko Kuroda are skipping the event. Trump's Fed pick, Chris Waller, will be there.

Focus will then shift to the G-7 in the French coastal town of Biarritz. While the global economy will form the crux of the talks, the most urgent security challenge is navigating Trump's abandonment of the nuclear deal. Allies can't shake the suspicion he wants war with Tehran. Boris Johnson may be his best shot at winning some European support. This is a look at why the U.S. and Iran are at loggerheads again.

Trade latest: The new tariffs Trump threatened on $300 billion of Chinese goods would drag China's annual economic growth below 6%, a Bloomberg survey showed. U.S. and China deputies had a "productive call" Wednesday and there will be another one in the coming days, Larry Kudlow told Fox Business. Meanwhile, U.S.-Japan trade talks were extended and will be held in Washington today, Kyodo reported.

Hasbro is buying the U.K.'s Entertainment One in a $4 billion deal, its biggest ever. It's a major push into media and gives the toymaker a studio adept at making movies, TV, animation and music, as well as children's brands like Peppa Pig that will help it expand into China. The sinking pound added to the allure of the asset. Entertainment One's shares rose above the offer price.

Earnings roundup: Gap's shares fell post-market after sales declined again at its namesake brand and Old Navy. Results were rosier at Salesforce, whose third-quarter revenue view topped estimates. HP Inc. dropped on concern its profitable supplies business is still struggling and CEO Dion Weisler left because of a family matter. Enrique Lores, head of the printing business, will take over.

Author

Clint Sorenson, CFA, CMT

WealthShield