The CME FedWatch tool shows only 24.1% see a hike at the July meeting

Outlook

It’s a weak data week this time. We get the Fed minutes on Wednesday with some having high hopes of discovering any bias one way or the other, but seeming to forget new Fed chief Warsh wants to squash speculation about forward guidance. Still, at the FOMC, every gov can say whatever is uppermost so deductions and inferences will abound.

The CME FedWatch tool shows only 24.1% see a hike at the July meeting, not much changed from earlier. Those expecting at least one hike at the September meeting is 46.0%--from 48.3% a week ago. We say this is pretty small potatoes and indicates those betting on the Fed were not impressed by the payrolls report—and quite rightly, too.

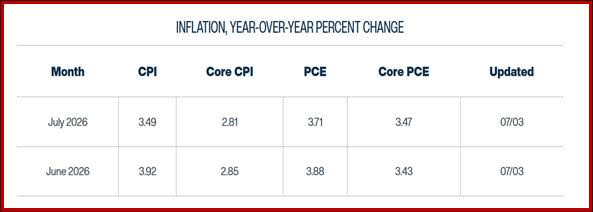

We don’t get fresh inflation data until next week when CPI comes out on Tuesday. The last reading for May was 4.2%, eek. The Cleveland Fed’s Nowcast has June at 3.88% with core at 2.81%. See the table. This is still way above the Fed target at 2% and with several components decidedly sticky.

We also get the ISM services PMI, likely at 54.2 for June from 54.5 in May. The number matters less than the idea the US economy is roaring along.

Forecast

Sentiment is not always reasonable. A single unfavorable payrolls number does not mean the Fed will abstain from a rate hike based on persistent, sticky inflation.

That the markets responded so strongly to the seemingly bad number is an indication of stubborn refusal to acknowledge a booming economy despite lower employment--and wishful thinking. The stock market in particular doesn’t want a rate hike, so will cling to whatever life-raft it thinks it has found.

It would take inflation relief that everyone can believe in to have a dovifying effect on the Fed. But never mind. The payrolls number this time led to the no-hike idea and the dollar lost ground across the board, even against the yuan and led by the NZD, weirdly enough.

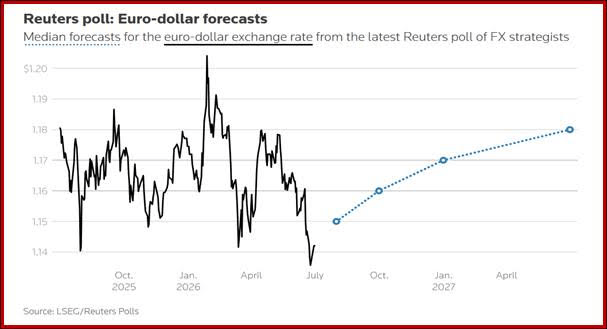

Assuming the rate hike idea comes back, and the CME betting board points that way, the dollar rise will resume. And yet we are keeping the Reuters survey of FX forecasters at the end of the report. The consensus is for a rising euro. For that to materialize, the ECB would have to hike and the Fed would have to stay its hand or cut. Lagarde has already said another hike may not be needed and we are pretty sure the Fed is not cutting, but it’s hard to forget that Reuters survey forecast.

Near the bottom of all this but capable of blooming upward is the price of oil. Keep an eye peeled. Oil “should” not be at pre-war levels. The price of oil permeates everything, everywhere. Even if we get a welcome relief for a while, the threat of another Strait closure remains.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat