RBNZ set to deliver July insurance hike

The collapse in oil prices makes the Reserve Bank of New Zealand’s 8 July decision more finely balanced. Even so, we expect policymakers to avoid disappointing hawkish pricing and deliver a 25bp ECB-style ‘insurance’ hike to anchor inflation expectations. That said, the risk of this being a one-off move is rising, which can limit NZD upside.

May's rate projections largely invalidated by now

The Reserve Bank of New Zealand once again faces an important policy decision with limited information. Key data is published only quarterly, and since the 27 May meeting, only first-quarter GDP figures have been released, with 2Q CPI and labour market data due on 20 July and 4 August. For what it's worth, growth was fairly robust in 1Q at 0.8% quarter-on-quarter, close to the 1.0% RBNZ estimate.

Back in May, the RBNZ kept rates on hold at 2.25% in a 3-3 split decision, with Governor Anna Breman casting the tiebreaking vote. The hawks’ concerns echoed those across other developed markets: the risk of inflation expectations de-anchoring and second-round effects. Breman opted for patience, but official rate projections signalled 50-75bp of tightening by end-2026.

But the oil assumptions underpinning those forecasts could not be more different now. The RBNZ assumed Dubai crude at around $95-105/bbl for the rest of 2026, versus current levels near $65. Accordingly, projections for headline CPI above 4.0% until 4Q26 now look unrealistic. We expect the 2Q print at 3.9%, followed by a return to 3.0% by year-end and a move back to 2.0-2.5% by mid-next year on base effects.

But it's risky to disappoint markets

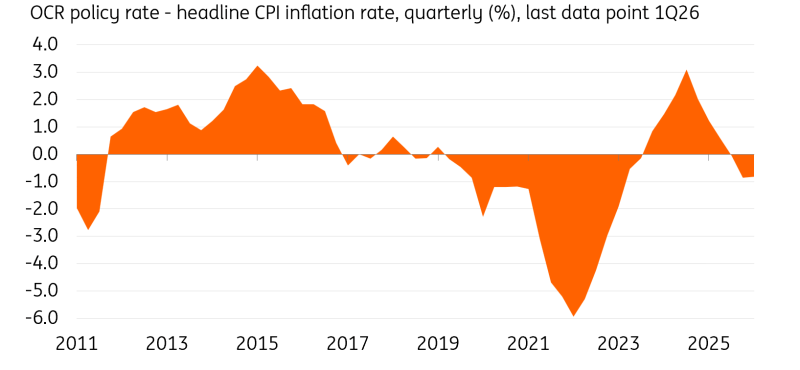

On that basis alone, a hold would be justified. However, the debate is less about headline CPI and more about inflation expectations. Crucially, policy entered the Iran war and energy shock in a relatively accommodative position, with a real rate of -83bp in 1Q26. That increases the risk that second-round effects are already in motion, especially with unemployment stabilising and wage growth still above 3.5%.

So while the inflation shock will be much shorter than projected, it looks risky to assume that wasn’t enough to trigger second-round effects. Markets are pricing 18bp for the July meeting and 55bp of tightening by year-end. A hold this week could trigger a sharp dovish repricing, even if accompanied by hawkish guidance, as markets may interpret delays as reducing the likelihood of any hiking at all given the improving inflation outlook.

RBNZ policy was accommodative before the Iran war

An insurance hike, another one close to 50-50

We therefore expect a 25bp hike to 2.50%, akin to the ECB’s June ‘insurance’ move. We still narrowly see one more hike in 2026, but the risk of this being a one-off has increased materially.

We have held a July hike call since May, though the oil price drop has made it tighter. Our baseline is a 4-2 split, where either Breman or Karen Silk shift to a hike, while the more dovish Chief Economist Paul Conway votes to hold.

This would likely be seen as a dovish hike. With no updated rate projections, the statement and vote will do the heavy lifting. We do not expect them to validate market pricing of 2.75% by year-end.

Less upside for NZD

While the initial reaction in the New Zealand dollar to a hike should be positive, markets may soon be tempted to fade the move on higher perceived risk that this will be a one-off move. Our call for NZD/USD remains bullish into year-end, primarily on the back of our expectation for no Fed hikes – where a dovish repricing should help pro-cyclical currencies and weigh on the US dollar.

However, we have lost a bit of conviction that NZD/USD will reach our 0.59 4Q target, and still see the higher-carry Australian dollar with greater upside potential.

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.