The calendar this week includes US existing home sales

Outlook:

We got no real change from the central bank in Japan and no real change is expected from the central bank in Canada, and that leaves the ECB on Thursday. Is there anything cooking? Nobody knows.

The calendar this week includes US existing home sales, not usually an FX mover, and we have to wait until Friday before we get the Jan flash PMI's. That leaves us nearly a whole week to contemplate the Chinese virus story and the overall importance of China in the grand scheme of things, plus the Trump impeachment (see below).

Commentary is starting to emerge that China not only won the trade war, but is winning the global hegemon battle, too. It's terribly slow and the US is not giving up the crown just yet, but China's globalization philosophy, if you can call it that, is the winner, not Trumpian xenophobia. China has not engaged in any war-like activities in decades (content to oppress its own people) and sets a model of sorts with the Belt and Road initiative. We don't buy it, but it's an emerging thesis—Trump has ruined the US reputation as a world leader, leaving the race open to others. European are cowardly. The British are busy. Japan doesn't want the job. Nobody respects the oppressive Chinese regime—especially censorship and racism and plenty of other features, too—but there is something resembling leadership going on.

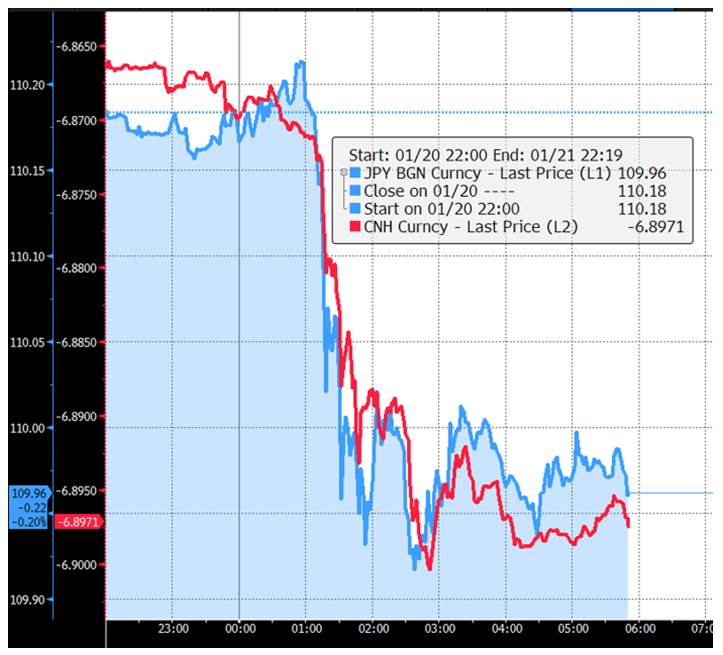

And while the yuan is hardly a top-drawer currency embraced by all, it is having an effect, perhaps for the first time ever, on a currency that is a major—the yen. We have seen the yen (and AUD) move along with developments in the US-China trade war, but we have not seen before today a direct one-to-one price move. This was detected by the astute Gittler at BDSwiss. See his chart.

As for the FX forecast, we continue to think that a contributing factor has to be Events. We have fundamentals, we have technicals, we have professional positioning, but we also have Events. In recent memory, the big Events have been Brexit and before that, Grexit. For a slew of reasons, the Trump partial ruination of the US economy is overlooked because the stock market has been manic. If it were to go depressive, Trump would get some blame.

The point is that financial markets are willing to overlook Trump as an Event because other factors are so massive. But Trump is an Event. Assuming the impeachment flops, Trump can still be seen as an Event for endangering the world by menacing N. Korea and then "falling in love," very nearly starting a war with Iran, the tariff wars and subsequent subsidy of US farmers, catastrophically rising income inequality, etc. And the unfitness may even be visible in his weight gain—the guy is fat—and inability to walk in a tidy fashion or speak coherently. More than one analyst notes dilated pupils, hmm. The day may come when we look back and see Trump as an Event.

Politics: The Senate impeachment trial of Trump begins this week. Hogging the airways over the long weekend, which was supposed to celebrate Martin Luther King, was Alan Dershowitz, hugely smug and always weaseling out of charges of hypocrisy. This time he claims he always said impeachment requires a crime, when we have tape of him saying the opposite in the Clinton case. Then he said "It certainly doesn't have to be a crime if you have somebody who completely corrupts the office of president and who abuses trust and who poses great danger to our liberty. You don't need a technical crime." In the Clinton case, Dershowitz said Clinton was guilty of a low crime, not a high one and thus not impeachable.

This time he says the impeachment charges should be dismissed because they do not charge "criminal-like conduct." Besides, obstruction of Congress is not named in the Constitution as a "high crime and misdemeanor" and shouldn't be an impeachable offense because it would set a terrible precedent. This is an interesting point but doesn't begin to address separation of powers.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports, including the Traders Advisories, send $3.95 to [email protected] using Paypal.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat