The Brexit Trade: And so it begins…

Britain’s official notification to the EU of intent to leave passed with little incident from a markets point of view, in line with most expectations. The pound, gilt yields and shares had priced in ‘known unknowns’ from leaving the EU long ago, but it is worth remembering that as we go through the Brexit negotiations further pockets of risk cannot be ruled out.

How politics can impact UK asset prices

The first test for markets is likely to come at the end of April when the EU will hold its first summit on Brexit. This is when the markets will hopefully gauge the tone of the negotiations and whether 0r not the EU wants to work with the UK to get a decent deal in the bag, or if it wants to punish the UK for voting to leave. If Theresa May doesn’t get her wish of trade talks alongside exit talks, something some EU members are reluctant to allow, then could confidence that the UK will get a good deal start to sour?

This souring could have an economic impact, especially if it dents consumer confidence. The UK’s economic resilience has been one of the sweet spots post Brexit, if this confidence starts to evaporate then it is hard to see how UK asset prices can continue to rally. However, as mentioned last week, we believe that the second wave of the Brexit trade, now that Article 50 has been triggered, could see stocks come under more pressure than the pound, where positioning is already heavily skewed to the downside. This is because there probably isn’t one company on the FTSE 100, maybe even FTSE 250, that isn’t touched by Europe in some way, which makes the entire index sensitive to the Brexit negotiations. See below for more detail on the stock market impact.

In contrast, Brexit was last year’s story for the FX market, and may not be a key driver of the pound again until late next year. This may sound like an odd thing to say, but investors are treating 2017 as something of a pause in Brexit-related sterling anxiety for now, after all, negations haven’t even begun, there is no real news at the moment to drive the pound, and markets only really move on fresh news. We think that by late next year, as a deal is eventually hashed out and put to all 27 members of the EU to agree, will be of more concern for sterling. This is reflected in sterling volatility, short term volatility is close to its lowest level in more than a year, which is keeping the pound stable for now.

Why UK shares are keeping the Brexit faith, for now…

UK shares are unlikely to be immune to any volatility as the divorce ensues. And whilst Britain’s stock markets quickly recovered and subsequently surpassed post-Brexit vote losses, a closer look reveals that investors have kept their eye on the ball with regards to risk.

Declines were not evenly distributed and the recoveries to date haven’t been either, although the passing of time and the influence of other economic factors has muddied the waters.

In the days and weeks after 24th June’s shock referendum result the weakest sectors were largely those in cyclical and financial industries operating domestically. These included general retailers, travel & leisure—namely airlines—supermarkets and housebuilders. Investors’ principle concerns over those shares relate to consumer confidence and spending as inflation begins to erode real earnings growth with the effect possibly compounded by price rises as the increased cost of imported goods due to weak sterling is passed on.

Another key differentiator of perceived and actual sensitivity to Brexit is companies’ exposure to sterling. In July, Citigroup estimated the London-listed market’s aggregate revenue exposure to the UK was around 30%. Within that of course, is a high concentration of some of the largest consumer-facing groups on the exchange, although low overall ties to sterling provides some underlying support to the market.

Among financials, sharp falls were seen in property investment companies, most listed as Real Estate Investment Trust (REIT), life insurers, and, banks. Investors are bracing for a hit from any slowing of the economy and subsequent fall in asset prices, though the most widely noted risk is around what is known as ‘passporting’: the ability of financial companies to offer their services within the European Union without regulatory restrictions.

UK-based financials have also been in focus as they are thought to be among the most likely to relocate staff to other EU countries for similar reasons. There has even been speculation that some might uproot themselves entirely—re-domicile—with attendant impact on market sentiment and even the wider economy. The notion that companies in other industries could do the same has not been entirely absent from investors’ minds, though it seems like an outside chance. Among Britain’s biggest banks, only Lloyds Banking Group does not currently have a ‘European Hub’. It has signalled that it will establish a subsidiary in Germany to rectify that, though is unlikely to go much further.

Another sector for which the retention of EU regulatory approval is urgent is air travel. EasyJet, which vies with Ryanair for the title of Europe’s largest low-cost airline by passengers carried, said last November that it will look to apply for a new licence to continue flying within the European Union. To do so, it will need to set up an Air Operator Certificate (AOC) in another EU country.

While it is common for airlines to have more than one certificate, they bring extra cost and complexity, factors that budget carriers try to avoid. EasyJet said it was close to selecting a location within the EU to make a formal application for the certificate early this year. Again, for now, it has stopped well short of suggesting it might move headquarters into the EU.

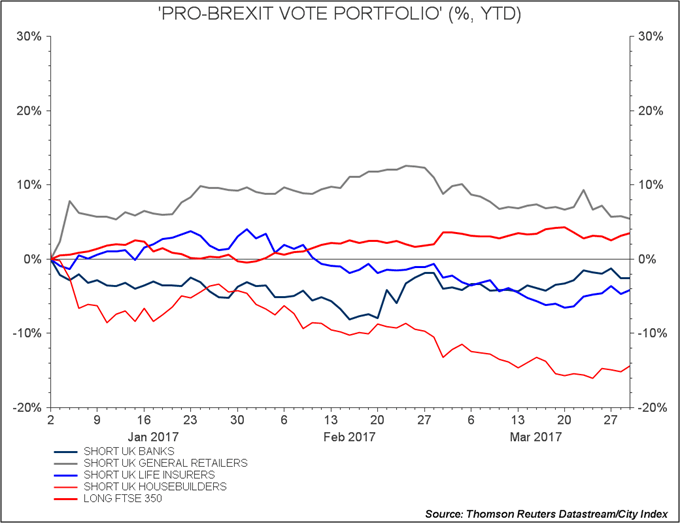

The withdrawal from Brexit-exposed sectors was reflected in a hypothetical portfolio of short-trades we compiled shortly after the Brexit vote. It markedly outperformed the FTSE 350 index for several weeks while these sectors in the FTSE struggled post the Brexit vote. However, a view of the year to date shows that there has been a strong recovery in the Brexit-exposed sectors of the broad FTSE index, as shown in our chart below. The only sector that has continued to underperform the broader index, is the general retailer sector, which is coming under pressure on the back of multiple factors including the expected inflation squeeze on the consumer as a result of the 2016 decline in sterling.

Figure 1:

Source: City Index

Even so, the challenge for investors is to assess the extent to which these moves have priced-in those known unknowns we mentioned above. Despite the market’s recovery, fund flows showed institutional investors were net sellers of London equities right into the beginning of this year. Whilst flows have since moderated, foreign investors have yet to return in large volume, according to Thomson Reuters Lipper, the funds data provider.

British government bond yields remaining close to rock bottom is another condition that may be less of a concern for British wholesale investors than for overseas funds. Worries of a hard Brexit are off-putting for all investors, whilst for American funds, the main concern is the currency translation impact.

Whilst British stock markets are calm, even resilient, investors remain poised for another flare up of volatility as anxieties are likely to rise as EU-UK divorce talks intensify in the coming months and years.

Author

Ken Odeluga

CityIndex

Ken Odeluga has over 15 years' experience of reporting and analysing global financial markets.