The biggie, if conditions were normal, would be the jobs reports this week

Outlook

Today we get factory orders, durable goods, and at least three Fed speakers. Oh, yes, Alphabet earnings, too. Some of the big houses remain in the camp of “tariffs will be short-lived” and others are calculating how much earnings will fall, by sector, if they persist.

The biggie, if conditions were normal, would be the jobs reports this week, including JOLTs today and the ADP private sector tomorrow, then nonfarm payrolls on Friday. We wonder if the fresh data will be noticed, since uncertainty is a mile high.

Where is the Fed in all this? It should be hiding under a rock. Yesterday the Atlanta Fed issued another revision to Q1 GDP, a stunning 3.9% from 2.9% only the day before. Not that the Fed funds bettors heed the Atlanta Fed, but the probability is not rate cut until June. Even so, the probability of no cut in June rose to 37.9% from 26.1% a week ago. As of the Dec 10 Fed meeting, a big 33.1% see only one cut this year, and 14.3% see no cuts at all.

Reuters reports “Three Fed officials warned on Monday trade tariffs come with inflation risks, with one arguing that uncertainty over the outlook for prices calls for slower interest-rate cuts than otherwise. Commerzbank has the right viewpoint—“… . There is still a high risk that significant tariffs and disruptions in international trade will ultimately occur."

Reuters reminds us that v”While there's some debate about whether one-off price hikes of this kind would necessarily lift the inflation rate per se, there are reasonable concerns that the endless threats and even the drip-drip application of them lifts inflation expectations.”

It's not even close to being over. Next up could be a Trumpy sovereign wealth fund. Somebody must have told him about those things and now he wants one, too. Two problems: it offers an opportunity to intervene in the FX market without seeming to. A sovereign wealth fund also offers the opportunity to deal in crypto. Three guesses which brand would get bought.

For what it’s worth, we see Trump as the reckless swashbuckler and Xi as a sniper. Or maybe Trump is a snake and China is a mongoose. China knows a direct assault when it sees one. And it fights dirty, as we see with ships wrecking undersea cables. We expect Trump to pretend to beat China but in reality, to back down. Realistically, Trump is trading Taiwan for something. We just don’t know yet what it is.

Forecast

The bond market has good economists and they pretty much all say tariffs are not temporary, tariffs are inflationary, and upheaval and uncertainty call for a rise in yields to include a heftier term premium. So far this has not exploded yields but it’s early days—just over two weeks, in fact. So while you can’t fight the tape, you can expect a rising differential plus risk aversion to feed the dollar. It won’t be consistent—no straight lines—and it won’t be pretty, but we can find no reasons to imagine other currencies “should” change trend direction. The exception is the Swiss franc, the ultimate safe-haven, and somewhat weirdly, the UK pound.

Tidbit: Elon Musk, not elected and not FBI-vetted, is closing down foreign aid, the Education Dept, the Small Business Administration and heaven only knows what else. He is accountable to only one person, Trump. This is not what the Constitution and over 200 years of practice and policy have called for. The Dems are shell-shocked and spineless, even though the power of the purse belongs to Congress, not the Executive. Secretary of State Rubio is stepping in on behalf of USAid. Trump made a somewhat offhand remark about reining in Musk.

Musk having seized the Treasury payment system is confusing. This could happen only because the TreasSec allowed it. We smell impeachment. Musk is being sued by private organizations who argue that it’s a privacy violation to give this “efficiency expert” access to peoples' tax refunds, veterans' benefits and disability checks. A brave Senator wrote a sedate letter to the TreasSec saying “I can think of no good reason why political operators who have demonstrated a blatant disregard for the law would need access to these sensitive, mission-critical systems.” Those include also Social Security and Medicare benefits, grants, and payments to government contractors including those that compete directly with Musk’s own companies.”

Do you really want this guy to have your Social Security number and net income?

The Supreme Court started the distrust of government among the people (with Bush v. Gore). Trump is finishing it. We had said the only good thing about Trump winning the election was the end of the civil war he promised to start if he lost. Now we wonder if the civil war doesn’t start from the other side.

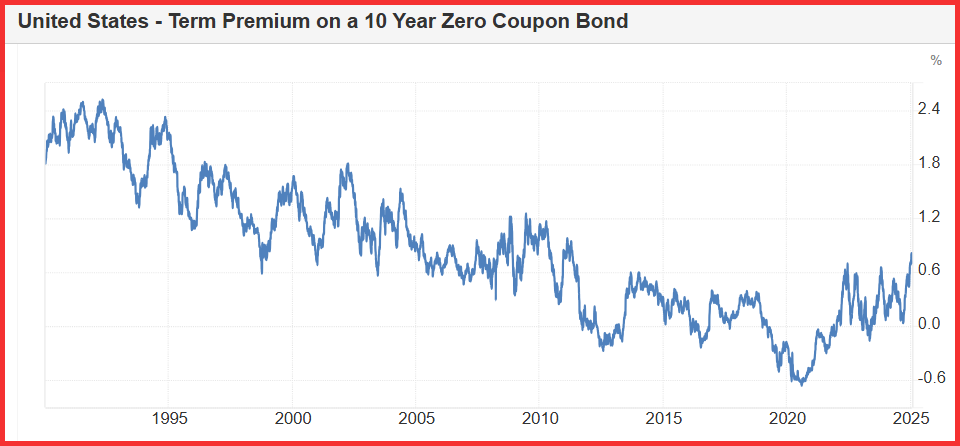

Keeper Tidbit: George Lucaci, a former Citi colleague and now a hedgie, did the taxing work of measuring and annotating the term premium. You can see it at the St. Louis Fed and also Trading Economics (see below).

But a list with additional info is always useful. He writes “Since 1950, the largest inflation premiums on the 10-year Treasury have typically occurred during periods of high inflation expectations - the 1970s and early 1980s.

1. 1979–1981 (Volcker era, early 1980s inflation)

-

Inflation premium: Approx. 7–8%.

-

This was during the period of stagflation, with inflation peaking above 13%. Fed Chairman Paul Volcker, raised interest rates dramatically to control inflation, which caused a massive gap between the 10-year Treasury yield and expected inflation.

2. 1974–1975 (Oil crisis and high inflation)

-

Inflation premium: Approx. 6–7%.

-

The 1973 oil embargo caused oil prices to skyrocket, leading to inflation above 10%. Treasury yields spiked in response to high inflation expectations.

3. 1947–1948 (Post-WWII inflation spike)

-

Inflation premium: Approx. 5–6%.

-

After WWII, the U.S. faced a period of high inflation as wartime price controls were lifted and pent-up demand surged.

4. 1973–1974 (Second oil crisis and inflation fears)

-

Inflation premium: Approx. 5–6%.

-

Similar to the 1974–75 period but with a sharper short-term spike as the oil embargo pushed prices up quickly.

5. 1980 (Inflation crisis)

-

Inflation premium: Approx. 4.5–5%.

-

Inflation in 1980 was ~13.5%, and investors demanded a high premium to hold Treasuries, especially long-term bonds.

6. 1965–1966 (Inflation and economic overheating)

-

Inflation premium: Approx. 4–5%.

-

The mid-60s saw inflation begin to rise as government spending surged during the Vietnam War and the Great Society programs.

7. 2008–2009 (Financial crisis and fears of deflation)

-

Inflation premium: Approx. 4–5%.

-

The global financial crisis created a period of deflation risk, and inflation expectations shifted, causing a big difference between real yields and nominal yields.

8. 1981–1982 (High-interest rates and recession)

-

Inflation premium: Approx. 4–5%.

-

This was another period of very high inflation, with the Fed’s aggressive policy driving interest rates to record highs.

9. 2011–2012 (Post-financial crisis recovery)

-

Inflation premium: Approx. 3–4%.

-

Inflation remained somewhat subdued after the financial crisis, but economic recovery fears and QE policies kept inflation expectations elevated.

10. 2021–2022 (Post-COVID economic recovery and supply chain disruptions)

-

Inflation premium: Approx. 3–4%.

-

The economic recovery from the pandemic led to supply chain issues and rising inflation expectations, creating a notable inflation premium in the bond market.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat