A full-blown trade and currency war

Outlook:

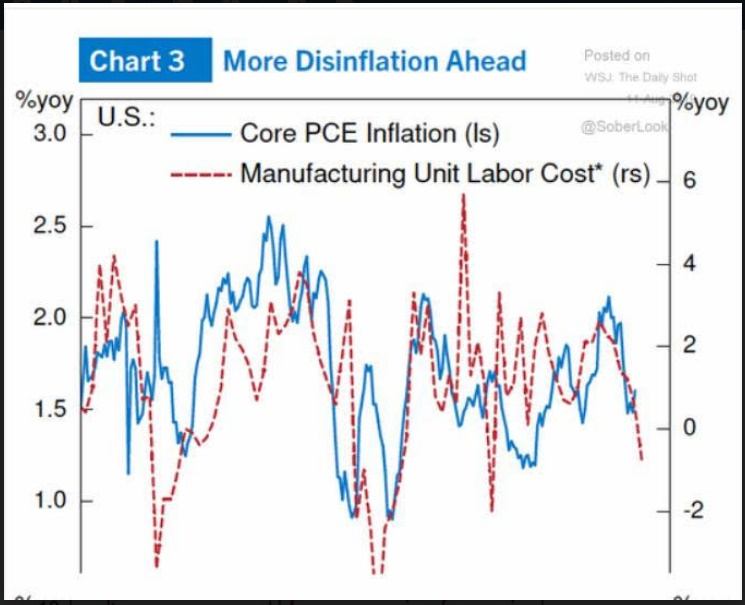

In economic news, the big release today is US CPI, likely the same or a small dip. But clouds are forming. A chart from something named Alpine Macro reproduced in the Daily Shot shows a distinct trend to the downside. Notice that in the top chart, inflation lags unit labor costs by 6 months and in the bottom chart, PPI lags the oil price by 6 months. It’s an interesting comparison. We’d like to see the same charts for PPI and CPI against some other data, like import prices, about to go up substantially on Sept 1.

The weekend Goldman report is getting a wide reception: the US and China are not getting a trade deal before the 2020 presidential election. Reuters summarizes: “Uncertainty about U.S. trade policy could lead state-side companies to reduce their capital expenditures, hire fewer workers and produce less. ‘… greater exposure to sales to China has been associated with slower capex growth as the trade war has intensified. We estimate a total uncertainty and sentiment drag on GDP of 0.1-0.2%.’” Gosh, that sounds small. If we take the Atlanta Fed’s Q2 number of 1.9%, the reduction is only to 1.7%, and the Atlanta Fed earlier in the spring had a lousy 1.3%.

Here's the funny part—we are in a full-blown trade and currency war, with a strong likelihood of FX market intervention and the environment deteriorating daily—and yet we can’t forecast the dollar falling, at least not by any substantial amount or for very long. We don’t even need to dig too deep, because the prevalence of zero and negative rates tells the whole story. Relative yield advantage waxes and wanes as the ruling factor in FX and right now it’s in weak phase, which we deduce because with the German Bund yielding -0.606%, the euro should definitely be lower if we had a one-for-one relationship. But the absence of a strong correlation doesn’t mean the concept is wrong. The US has positive returns and hardly anyone else with a decent-sized market does. The Fed can cut until the cows come home and the US still has a yield advantage. It would be helpful for the Fed to be able to justify cuts by referring to global crosscurrents or whatever euphemism Mr. Powell can adduce, rather than raw read-meat political interference, but in the end, if you are a global fund manager, positive is better than negative.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a free trial, please write to [email protected] and you will be added to the mailing list..

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat