Tech rout and trade truce, markets digest AI spending fears and US

Thursday witnessed US equity markets take a leg lower, with the S&P 500 dropping 1.0% to 6,822, the Nasdaq Composite falling 1.6% to 23,581, and the Dow Jones Industrial Average slipping 0.2% to 47,522. For those who follow technicals, you will acknowledge the clear daily bearish evening star candle patterns on both the Nasdaq Composite and the Nasdaq 100.

Share prices of Meta (META) and Microsoft (MSFT) took sizable hits in recent trading amid concerns about substantially higher capital expenses driven by AI investments, with META down around 11.0% and MSFT erasing approximately 3.0%.

Temporary truce between the US and China

On the trade front, following the Trump-Xi showdown on Thursday, their first encounter in six years yielded a ‘temporary truce’, rather than a comprehensive long-term trade deal. The interim arrangement includes China resuming US soybean purchases and suspending rare earth export controls for a year, while Trump reduced tariffs on Chinese goods from 57% to 47%. Both sides also suspended certain port fees and export controls.

While this modest de-escalation buys some time, the lack of a long-term framework leaves global trade dynamics uncertain.

ECB maintains steady course

Following the BoJ’s lead, the ECB held all three key rates unchanged for a third consecutive meeting yesterday – as expected – leaving the deposit rate at 2.00%. The decision should not have raised many eyebrows and reflects the central bank’s view that monetary policy remains in a ‘good place’. As you would have expected, guidance was pretty limited; the accompanying rate statement reiterated that the central bank remains on a ‘data-dependent and meeting-by-meeting approach’.

In her press conference, ECB President Christine Lagarde highlighted the economy’s growth despite headwinds, although she acknowledged geopolitical tensions, trade negotiations, as well as France’s budget crisis and Germany’s delayed fiscal stimulus.

As I am sure you are aware, eurozone inflation continues to meander around the central bank’s 2.0% target – we have September’s print landing later today – with Q3 economic activity growing by 0.2% (surpassing expectations of 0.1%), according to preliminary flash estimates, and unemployment remaining near historic lows.

The market reaction to the ECB announcement was muted, though should the EUR continue to rally, this could eventually lead to another rate reduction, particularly if it threatens economic recovery. A stronger EUR increases export costs while reducing import prices, potentially compressing export revenues and dampening inflationary pressures. In terms of future policy cuts, most analysts I have spoken with believe the central bank is done and dusted with rate cuts, though money-market expectations suggest a potential 25-bp cut later next year. The focus now shifts to December’s meeting, which will offer updated quarterly economic projections.

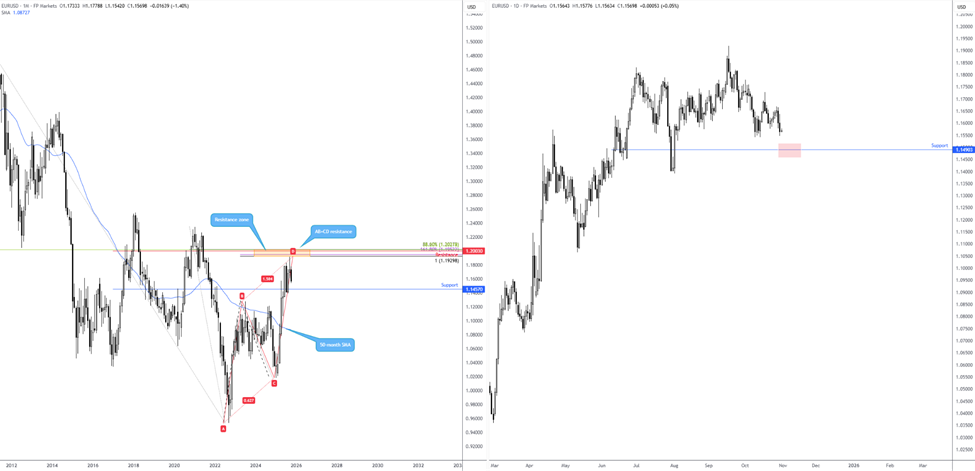

As for the technicals I am watching on the EUR/USD right now, we can see that long-term flow recently rejected monthly resistance between US$1.2028 and US$1.1930, with scope to continue pressing south until monthly support as far south as US$1.1457. With that in mind, a break below US$1.1540ish on the daily chart opens the door for a run on sell-stops to test support from US$1.1490. Given this support, and the monthly support positioned below at US$1.1457, this area could be a location EUR/USD longs make a show from.

Day ahead

Overnight, the October Chinese manufacturing PMI came in lower than expected at 49.0 (versus 49.6 consensus), dropping to its lowest level in six months.

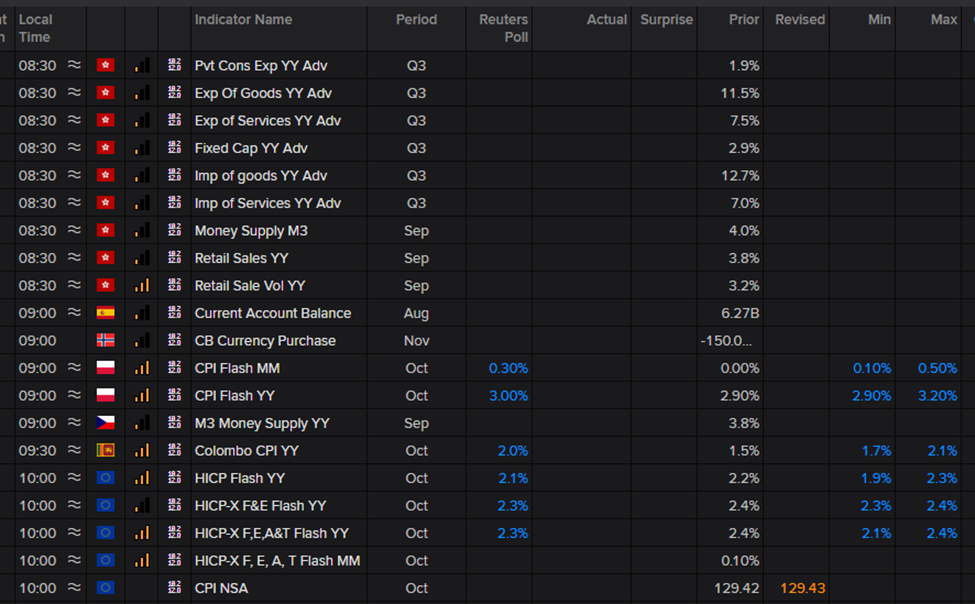

Later today at 10:00 am GMT, September eurozone CPI inflation will be released, and, according to economists’ expectations, headline and core YY measures are expected to moderate slightly. Overall, unless we see a marked deviation from consensus today, I am not expecting much volatility in the markets from this report. As shown in the LSEG economic calendar below, the headline print is expected to ease to 2.1% (from 2.2% in August), with both core measures forecast to slow to 2.3% (from 2.4%). September projections from the ECB suggest inflation will average 2.1% this year, with 2026 expected to ease to 1.7%.

Charts created by TradingView

Author

Aaron Hill

FP Markets

After completing his Bachelor’s degree in English and Creative Writing in the UK, and subsequently spending a handful of years teaching English as a foreign language teacher around Asia, Aaron was introduced to financial trading,