WTI balances physical flows as softer inflation reshapes demand expectations

Key takeaways

- WTI trades above the $80.00 participation pivot as softer US inflation eases pressure on Treasury yields and supports broader commodity participation.

- Physical crude flows regain prominence as shipping conditions and export routing gradually normalize following recent geopolitical disruptions.

- OPEC's latest demand outlook and inventory dynamics reinforce a market increasingly driven by logistics, freight efficiency and regional supply distribution.

- The Renko structure remains constructive, with price holding above the EMA 9 and EMA 21 while participation transitions from expansion toward balance.

WTI returns to its physical identity

WTI enters Wednesday's session in a market where macroeconomic conditions and physical oil logistics are beginning to rebalance after several weeks dominated by geopolitical headlines and monetary policy repricing.

The softer-than-expected US Consumer Price Index released on Tuesday reduced inflation concerns across financial markets. Headline CPI slowed to 3.5% year over year, while Core CPI eased to 2.6%, reinforcing expectations that price pressures continue to moderate. Treasury yields moved lower following the release and the US Dollar softened as investors reassessed the path of future Federal Reserve policy.

For crude oil, however, lower inflation represents only the first layer of the pricing mechanism.

Once monetary volatility begins to fade, the market naturally redirects its attention toward the efficiency of the physical oil system. The availability of barrels remains important, yet the way those barrels move across shipping lanes, storage hubs and refining systems increasingly determines regional pricing.

That transition is becoming visible once again.

Rather than focusing exclusively on monetary policy, market participants are returning to the operational structure of global crude flows.

Softer inflation reshapes demand expectations

Inflation moderation carries important implications for energy markets because it influences financing conditions, business investment and consumer demand simultaneously.

Lower inflation eases upward pressure on real yields while reducing the probability of additional policy tightening. Financial conditions become less restrictive, allowing investors to reassess expectations for industrial activity and fuel consumption over the second half of the year.

Demand expectations therefore improve gradually rather than abruptly.

This distinction matters for crude oil.

Energy consumption rarely responds immediately to individual macroeconomic releases. Instead, demand evolves through transportation activity, manufacturing output, freight volumes and refinery utilization. Softer inflation contributes to a more supportive macro backdrop, although physical demand ultimately determines whether additional barrels are required.

Markets therefore continue evaluating incoming inflation data alongside broader indicators of economic resilience.

Attention now shifts toward Wednesday's Producer Price Index, which may offer further evidence regarding pipeline inflation and production costs across the industrial economy.

Physical flows regain influence

While inflation shapes financial conditions, logistics continue shaping oil prices.

Recent reporting from Reuters indicates that shipping activity through the Strait of Hormuz has gradually recovered following the recent geopolitical disruptions, although vessel movements continue adapting to elevated security risks and revised navigation procedures. Regional freight costs remain above longer-term averages, while shipping companies continue adjusting routes according to operational risk assessments.

At the same time, OPEC's latest Monthly Oil Market Report maintained expectations for continued global demand growth during 2026, although the organization modestly reduced its forecast to reflect a slower pace of economic expansion. Demand is still expected to strengthen into 2027, supported by transportation fuels and petrochemical activity across emerging economies.

The International Energy Agency also notes that global inventories and maritime crude movements are gradually normalizing as export systems recover from previous disruptions. Floating inventories have increased in some regions while onshore inventories remain relatively contained, illustrating that the logistics network continues redistributing crude rather than simply accumulating supply.

These developments reinforce an important point.

WTI is increasingly behaving like a logistics market rather than a purely macro market.

Freight availability.

Export routing.

Inventory allocation.

Refinery access.

Shipping efficiency.

Each component contributes to regional price formation because physical oil must move through an increasingly complex transportation network before reaching final demand.

This is where the current market finds its equilibrium.

Price formation increasingly depends on logistics

The recent geopolitical tensions demonstrated that oil prices respond to much more than production volumes.

Temporary disruptions across strategic shipping corridors rapidly altered freight premiums, insurance costs and vessel deployment. Even when production remained largely intact, uncertainty surrounding delivery conditions created significant pricing adjustments across physical markets.

As those disruptions gradually fade, the market begins measuring how efficiently the system can restore normal flows.

This process is particularly important because inventories alone no longer provide a complete picture of supply conditions.

Where inventories are located often matters as much as how large they become.

A barrel stored near export infrastructure carries different economic value from one located deep inside an inland storage hub.

Similarly, transportation capacity increasingly influences regional balances between producers, refiners and final consumers.

These logistical considerations explain why crude markets frequently stabilize before traditional supply-demand statistics fully adjust.

Price formation increasingly reflects accessibility rather than simple availability.

That evolution aligns closely with the current macro backdrop.

Softer inflation reduces financial stress.

Physical logistics determine whether improving demand expectations can translate into actual crude movements.

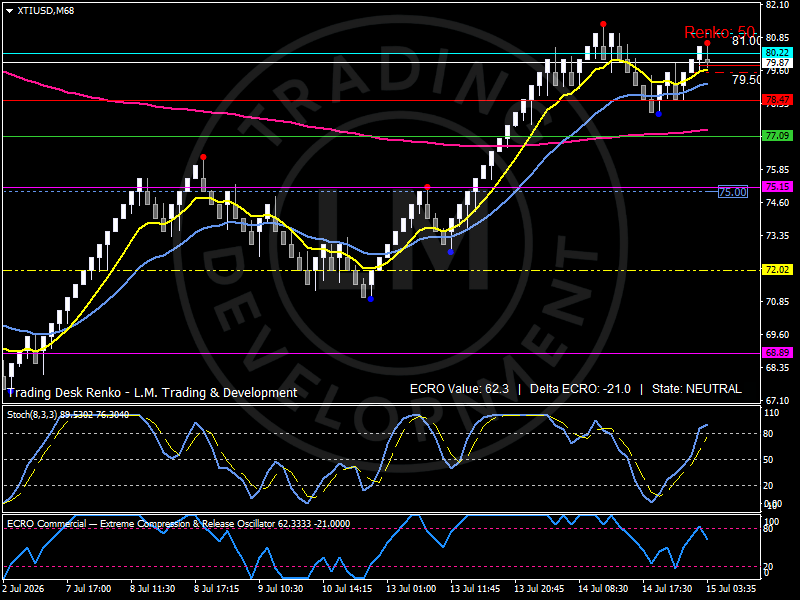

Technical structure: Participation remains constructive above $80

The Renko chart continues describing a healthy medium-term structure despite the recent consolidation.

WTI remains comfortably above both the EMA 9 and the EMA 21, confirming that buyers continue controlling short-term participation. Meanwhile, the EMA 200 continues trending upward below current prices, reinforcing the broader bullish structure that has developed throughout July.

The market has transitioned from directional expansion into a more balanced participation regime.

Current price action revolves around the $80.00 participation pivot, where buyers continue absorbing profit-taking following the recent advance.

Immediate resistance develops between $80.20 and $80.80. A sustained move above this area would reinforce continuation toward higher participation zones.

Initial support is located around $79.50, while the EMA 21 reinforces dynamic support near $78.50.

The ECRO oscillator remains positive near 62, confirming that participation continues supporting the prevailing structure even as momentum moderates.

Delta ECRO has turned negative, suggesting that the previous expansion phase is gradually transitioning into consolidation rather than signaling deterioration in underlying participation.

The stochastic oscillator has recovered into higher territory, indicating renewed buying interest while remaining consistent with a market consolidating inside an established uptrend.

Overall, the technical structure remains constructive.

The market appears to be redistributing participation rather than reversing trend.

Bird's eye view

WTI is gradually transitioning from a macro-driven repricing phase toward a logistics-driven pricing environment.

Inflation moderation supports financial conditions.

Treasury stabilization reduces macro volatility.

Demand expectations improve incrementally.

Physical flows, freight efficiency and inventory distribution increasingly shape regional price formation.

Technically, the market continues holding above the $80.00 participation pivot, supported by positive participation metrics and a constructive EMA structure.

Outlook

WTI enters the second half of the week with attention increasingly shifting away from inflation surprises and toward the operational efficiency of the global crude market.

As macro volatility eases, investors are likely to focus more closely on shipping conditions, inventory distribution, refining activity and the resilience of physical demand.

The next directional phase will likely emerge from the interaction between improving financial conditions and the ability of global logistics networks to sustain efficient crude flows across an increasingly interconnected energy system.

Author

Luca Mattei

LM Trading & Development

Luca Mattei is a market analyst focusing on FX, metals, and macroeconomic trends. He develops trading tools for retail and professional traders, coding indicators and EAs for MT4/MT5 and strategies in Pine Script for TradingView.