The boom daily: Soft CPI buys time as AI hits the power wall and Oil rewires around Hormuz

Rates market daily: Soft CPI lets the Fed kick the hike can down the road

For markets, this was probably the cleanest outcome available. Inflation cooled enough to puncture the urgency around an imminent Federal Reserve hike, but not so dramatically that the market was forced to price in an economic accident. The Fed can keep its hawkish language polished for public consumption, traders can step back from the edge of a July move, and risk assets are handed something they have been craving for weeks: time. More importantly, time for the Middle East fracas to come off the boil.

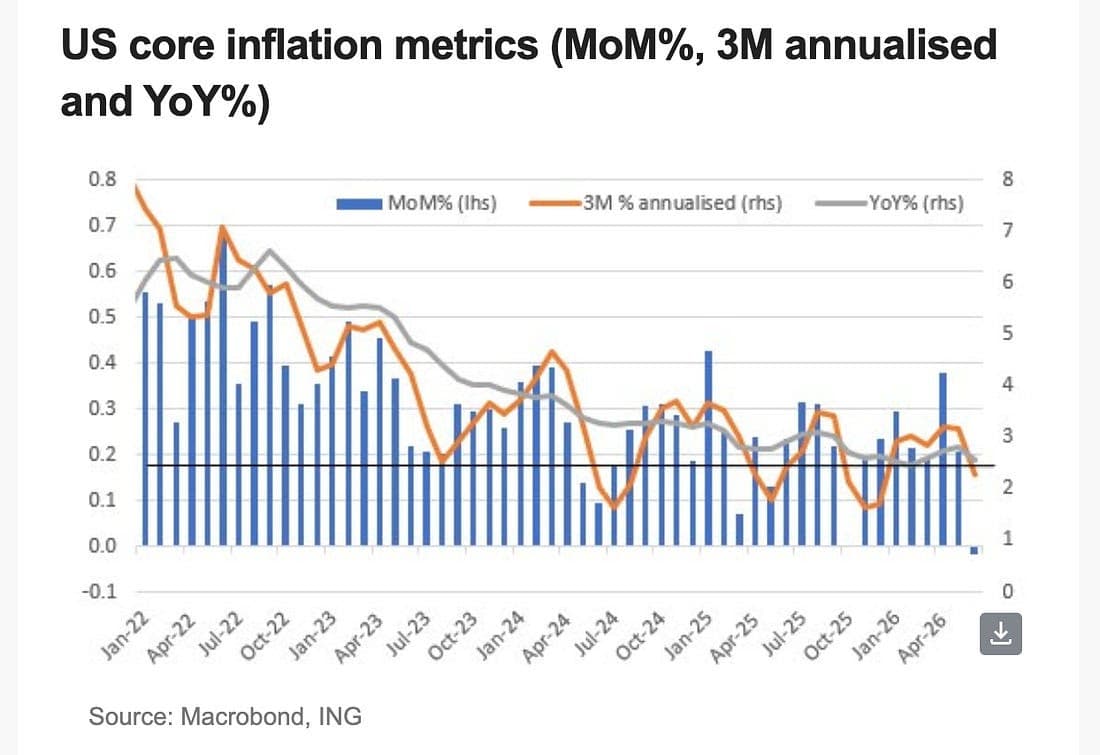

The June CPI report came in considerably softer than expected. Headline prices fell 0.4% month-on-month against forecasts for a 0.1% decline, while core inflation was effectively flat versus expectations for a 0.2% increase. To three decimal places, core CPI actually printed at -0.017%. That pulled annual headline inflation down to 3.5% from 4.2%, while core inflation slowed to 2.6% from 2.9%.

Gasoline prices did much of the heavy lifting, falling 9.7% on the month, but this was not a report built on one collapsing component while the rest of the inflation house kept burning. The softness had breadth. Education and communication costs fell 0.8%, apparel dropped 0.6%, used-car prices slipped 0.2%, medical care declined 0.1%, and shelter rose just 0.1%. Recreation was the only meaningful pocket of strength, perhaps carrying some World Cup-related noise, but the broader message was difficult to argue with: inflation did not merely miss; it softened across enough categories to make the miss credible.

That is why the rates market moved with such conviction. Two-year Treasury yields fell around 10 basis points, and the 10-year yield dropped roughly six basis points after the release. A July hike that had briefly been treated as a coin toss was quickly reduced to less than four basis points of tightening. Markets also trimmed the amount of cumulative tightening expected into next year.

The Fed’s hike door is not locked, but CPI has pushed the furniture back against it.

Kevin Warsh’s semi-annual testimony offered little reason to force it open again. The Fed chair repeated the familiar language about vigilance, price stability and having no tolerance for persistently high inflation. But there was very little forward guidance beneath the armour. Warsh can continue telling Congress that the inflation surge of the past five years must be buried, while privately recognising that one of the broadest soft inflation reports in months has bought the central bank room to wait.

That waiting game matters because the inflation path may continue to soften even with oil and gas prices elevated by the conflict around the Strait of Hormuz. ING points to housing as the heavier structural force. Shelter carries roughly 35% of the CPI basket, yet home-price growth has slowed sharply and rents are falling outright in a growing number of states. If shelter inflation keeps grinding lower, it can act like an anchor dragging the broader index toward target.

The labour market is also doing less inflationary damage. The days of two vacancies for every unemployed worker are gone, the quits rate has collapsed, and companies no longer need to pay whatever it takes to retain staff. Wage growth near 3% is far more consistent with 2% inflation than the overheated conditions of 2022.

Tariffs may prove another fading ember. ING argues that their impact is increasingly a one-off step change rather than a permanent inflation engine, particularly as exemptions widen and refunds from the abandoned IEEPA tariff regime flow back to corporate America.

The market’s mistake was assuming the Fed needed to react to every oil spike with another turn of the screw. This CPI report offers a different path. Warsh can keep the threat of hikes alive, preserve institutional credibility and wait for more evidence without tightening into an economy already carrying pressure through housing, energy and financing costs.

The can has not disappeared. The Fed has simply kicked it far enough down the road for markets to breathe again.

Tech supply chain daily: The AI boom has reached the wall socket

The AI trade has spent the past three years racing up the stack, from chips to models, from models to data centres, and from data centres to the promise of an economy rebuilt around machine intelligence. But somewhere between the earnings deck and the server rack, the market forgot one small detail: all of it has to be plugged in.

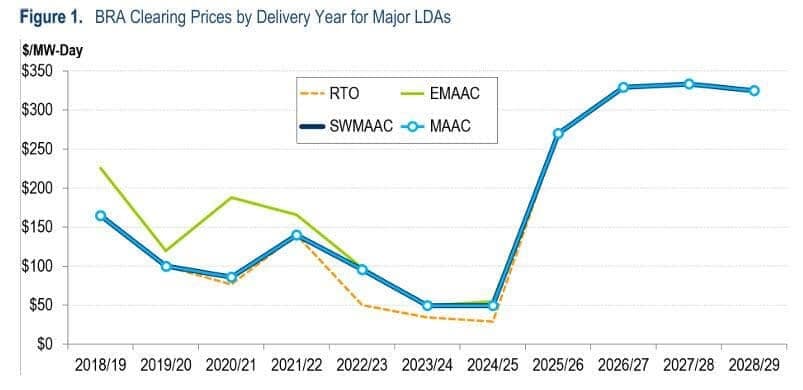

PJM Interconnection, the largest US power grid, has now failed for a third consecutive year to secure enough future capacity to guarantee reliability. Its latest auction for the year beginning in June 2028 came up 6.8 gigawatts short, roughly the dependable output of several large nuclear reactors. That is not a technical footnote. It is the sound of the AI buildout running headfirst into the physical limits of the American grid.

PJM covers 13 states, Washington, DC, and more than 67 million customers. More importantly for the AI trade, it sits beneath northern Virginia’s Data Center Alley, the largest concentration of data centres in the US. The same region being asked to carry the next industrial revolution is now struggling to prove it can keep the lights on when demand peaks.

The imbalance is simple. Data centres can be announced faster than power plants can be built. Capital can be raised in weeks, permits can take years, and transmission lines move at the speed of public hearings rather than silicon. The AI economy is sprinting in trainers while the grid is still tying its boots.

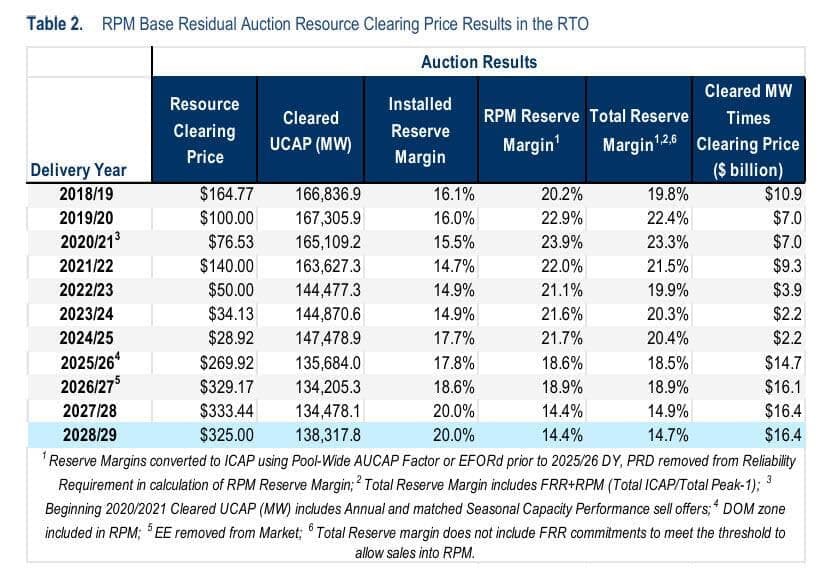

PJM secured 138,318 megawatts of generation and demand-response capacity in the auction. Even after including self-supplied resources, the system remained 6,831 megawatts below its reliability requirement. The previous auction was already short by roughly 6,500 megawatts, making this less a surprise than a warning siren that nobody has yet found the switch to silence.

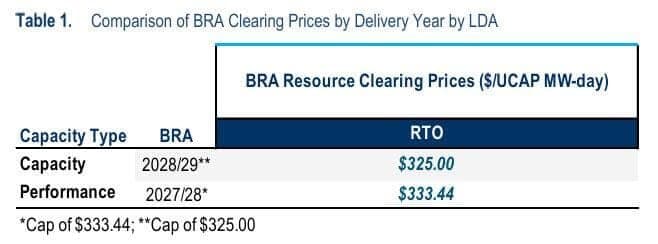

The price signal is equally uncomfortable. Capacity cleared at the regulatory ceiling of $325 per megawatt-day. Without the cap, PJM estimates that most of the grid would have cleared near $554.72, while the ComEd region would have reached $776.69. In other words, the market price of scarcity was roughly 70% higher than consumers were allowed to see.

That may soften the immediate blow to household bills, but it also dulls the signal that is supposed to summon new generation. Regulators are trying to protect consumers from the cost of scarcity while asking producers to invest billions to solve it. The market is being told to build more power, but not to expect scarcity prices for doing so.

This is where the next fault line in the AI trade begins to open. Hyperscalers want firm electricity now. Utilities need years to add capacity. Consumers do not want to subsidise data-centre demand through higher monthly bills. Generators want confidence that the returns will justify the capital. Everyone wants the boom, but nobody wants the invoice.

PJM is now preparing a backstop procurement process for September, with growing pressure to make hyperscalers carry more of the burden. That could mean dedicated generation, curtailment commitments, financial guarantees or a much clearer requirement that data centres arrive with power solutions attached. The days of treating electricity as an unlimited utility input may be ending.

For traders, the implication is broader than utilities. The next stage of the AI supply chain may be won not only by chipmakers and cloud platforms, but by turbine makers, nuclear developers, transformer manufacturers, gas infrastructure firms and transmission equipment suppliers. The bottleneck is moving downstream, and markets usually pay handsomely for whoever owns the narrowest bridge.

The AI boom is not running out of ambition. It is discovering that digital dreams still require analogue power.

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.