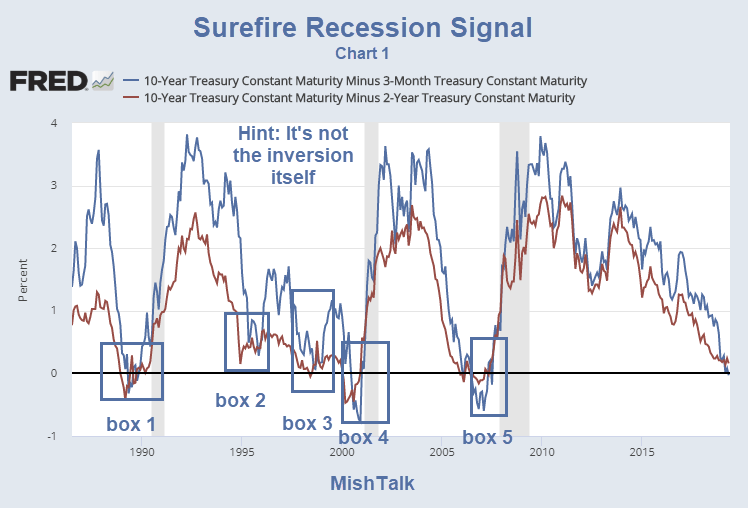

Surefire Recession Signal in Pictures

The strength of inversions widened today. That's a strong recession warning, but it is not the actual recession signal.

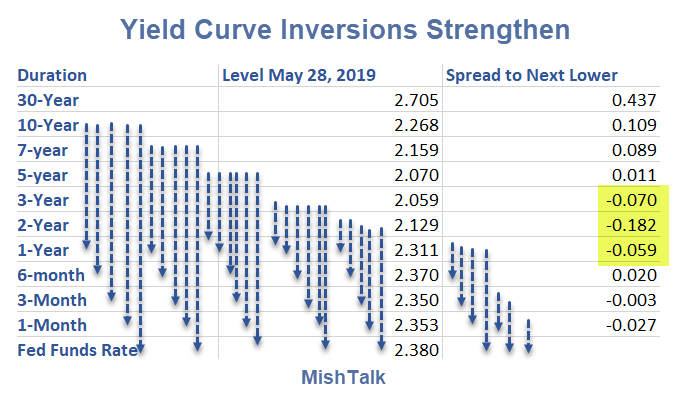

Inversions Widen

Today's bond market action is a strong follow-through on Friday's action.

Imminent Signal

The recession imminent signal is not the inversion but a sudden steepening of the curve following a period of inversion.

A comparison of the strength of the inversions today vs 2007 will show what I mean.

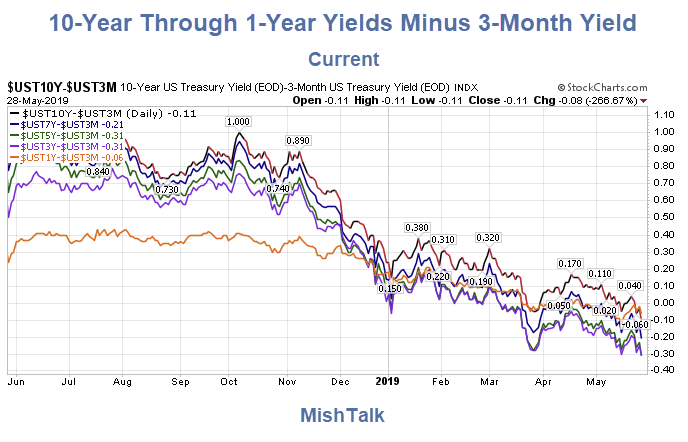

Inversions With the 3-Month Note Today

The 10-year, 7-year, 5-year, 3-year, and 1-year notes are inverted with the 3-month T-Bill. The inversion isn't the signal. A sudden steepening of the yield curve following inversion is the "recession imminent" signal.

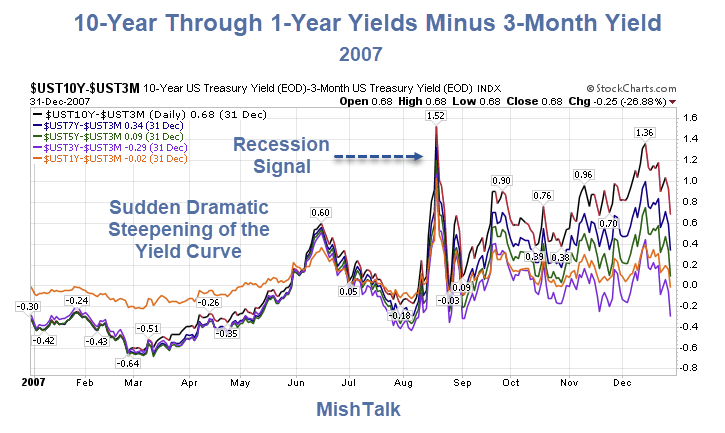

Inversions With the 3-Month Note 2007

Chart 1 Repeated for Ease in Reading

Signal Discussion

-

Box 1, Box 4, and Box 5 all have the same thing in common: A sudden steepening of the 3-Month to 10-Year curve following inversion.

-

Box 2 had no inversions

-

Box 2 and Box 3 show a steepening of the 2-year to 10-year spread but not the 3-month to 10-year spread.

Some are waiting for a 2-10 inversion. Perhaps it does not happen. But even if it does, that will not be the signal.

Watch for a sudden steepening of the curve.

How? Why?

That's easy. The Fed will either cut or signal it is about to cut.

Too Late

On August 17, the Fed Cut the Discount Rate by 50 Basis Points

Fed Statement: Financial market conditions have deteriorated, and tighter credit conditions and increased uncertainty have the potential to restrain economic growth going forward. In these circumstances, although recent data suggest that the economy has continued to expand at a moderate pace, the Federal Open Market Committee judges that the downside risks to growth have increased appreciably. The Committee is monitoring the situation and is prepared to act as needed to mitigate the adverse effects on the economy arising from the disruptions in financial markets.

Flashback September 18, 2007

Inquiring minds are investigating the Minutes of the August 7, 2007 FOMC meeting released September 18, 2007.

Amazingly Wrong Points

-

At its August meeting, the FOMC decided to maintain its target for the federal funds rate at 5-1/4 percent. In the statement, the Committee acknowledged that financial markets had been volatile in recent weeks, credit conditions had become tighter for some households and businesses, and the housing correction was ongoing. The Committee reiterated its view that the economy seemed likely to continue to expand at a moderate pace over coming quarters, supported by solid growth in employment and incomes and a robust global economy.

-

Conditions in corporate credit markets were mixed. Investment- and speculative-grade corporate bond spreads edged up; they were near their highest levels in four years, although they remained far below the peaks seen in mid-2002

-

In preparation for this meeting, the staff continued to estimate that real GDP increased at a moderate rate in the third quarter. However, the staff marked down the fourth-quarter forecast, reflecting a judgment that the recent financial turbulence would impose restraint on economic activity in coming months, particularly in the housing sector. The staff also trimmed its forecast of real GDP growth in 2008 and anticipated a modest increase in unemployment.

-

With credit markets expected to largely recover over coming quarters, growth of real GDP was projected to firm in 2009 to a pace a bit above the rate of growth of its potential.

-

Participants thought that the most likely prospect was for consumer expenditures to continue to expand at a moderate pace on average over coming quarters, supported by growth in employment and income.

-

In the Committee's discussion of policy for the intermeeting period, all members favored an easing of the stance of monetary policy. The Committee agreed that the statement to be released after the meeting should indicate that the outlook for economic growth had shifted appreciably since the Committee's last regular meeting but that the 50 basis point easing in policy should help to promote moderate growth over time.

Yield Curve Reaction

The Fed did not reduce the Fed's fund rate. So, why did the yield curve react?

The Fed did slash the discount rate by 50 basis points. The yield curve reacted sharply.

If you think the Fed has a handle on stopping the next recession think again. As in 2007, they will not even see it. Nor would they admit it if they did.

Watch for Steepening

Watch for a sudden steeping of the 3-Month to 10-Year spread. Don't expect a long warning period, and don't pay attention to the Fed or president Trump yapping about the strong economy when it happens.

I expect the delay this time may be negative, the recession will already have started.

Miracles Not Coming

The Fed blew another magnificent bubble.

Don't expect miracles. The next recession is baked in the cake.

Author

Mike “Mish” Shedlock's

Sitka Pacific Capital Management,Llc