Sugar injection ahead of key inflation data

Yesterday was marked by a pause in the tech sell-off and further rotation toward non-tech European indices. The CAC 40 led gains, the Stoxx 600 posted a modest advance, while the German DAX underperformed due to a nearly 19% plunge in Rheinmetall after reports that the German government changed its plans to buy six large warships — a contract Rheinmetall had been expected to win. TKMS, a domestic rival, rallied 16% on expectations that it would instead supply four smaller warships to the German government. But aside from that news, the macroeconomic backdrop remained favourable for European stock markets. The benchmark European 10-year yield fell to 2.86%, the lowest since 10 March, as oil prices continued to decline, softening European Central Bank (ECB) expectations.

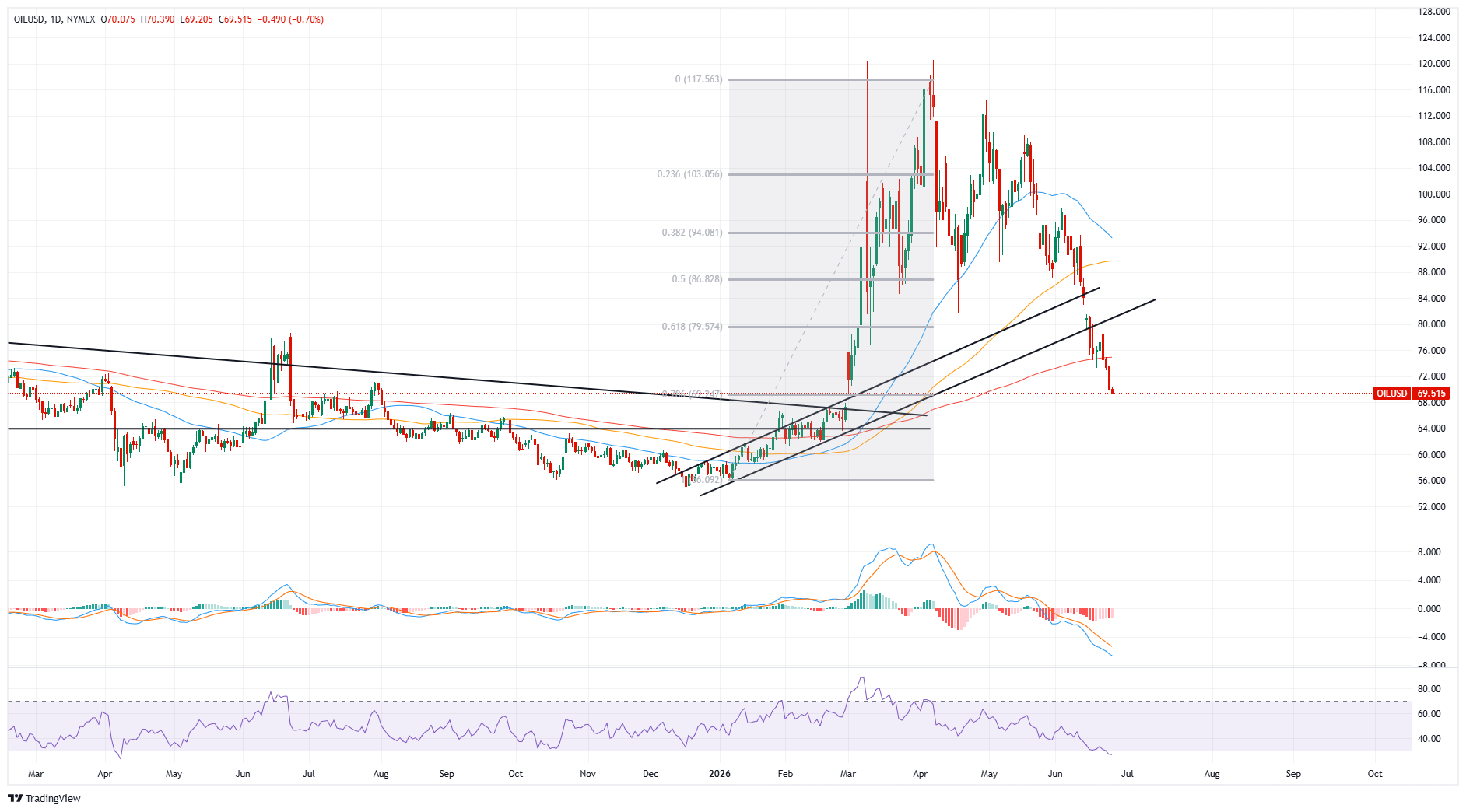

US crude slipped below the $70pb mark on news that vessels are now transiting the Strait of Hormuz with their satellite signals switched on — and not only. A combination of strategic inventory releases, a collapse in demand from top buyer China and a substantial number of tankers quietly leaving the Persian Gulf "dark" had contributed to a small oversupply in some key markets, according to traders interviewed by Bloomberg. That's in line with my earlier forecast that oil prices will likely swing between $60-80pb in the coming weeks. Geopolitical risks remain, as the Middle East is rarely a calm sea, China will start tapping into the oil market as tensions ease, and countries will begin replenishing their strategic reserves, absorbing part of the additional supply. But over the medium term, the IEA has also warned that once Middle East tensions fade and markets return to normal, demand will continue to slow while supply remains ample — pointing to further declines in oil prices toward $50pb. That's my forecast for the next twelve months.

All of that is good news for the cyclical European indices that have been grappling with higher energy prices, which also contributed to the ECB's rate hike earlier this month.

Read the full article here.

Author

Ipek Ozkardeskaya

ipekScope

Ipek Ozkardeskaya began her financial career in 2010 in the structured products desk of the Swiss Banque Cantonale Vaudoise. She worked in HSBC Private Bank in Geneva in relation to high and ultra-high-net-worth clients.