Stock markets continue to strengthen as economies reopen

Stock markets continued to strengthen as economies re-open but have yet to retest last Thursday’s highs. The unrest in the US is not likely to have a material impact on equity markets in the near term, largely because of the large-cap weighting, but we should caution that it has the potential to delay the economic recovery in the US. People who would have been going back to work, spending in restaurants and bars, reopening their stores, will not in this febrile environment. President Trump is doubling down on using force to combat the unrest.

There was news on Remdesivir from Gilead – shares fell as the company reported indications that the drug has some positive impact, but it’s a long way from a slam dunk Covid-beater. Shares fell more than 3%.

So far, the situation with Hong Kong and simmering US-China tensions are being shrugged off. News that China was reducing soy imports from the US temporarily dented risk appetite yesterday. Today China’s foreign ministry said there was no information on any soy bean halt. Could be a load of rumours, but we should be very attuned to further developments on this front.

On the whole investors continue to see the glass half full even though the real extent of the economic damage is yet to be really felt. Furlough schemes and government bailouts may insulate people and companies from the shock, but these only delay the pain.

The FTSE 100 had a look at 6200 again this morning having moved added 90pts to 6,166 on Monday. Thursday’s peak at 6,234 remains the bull’s target for the cash market. The DAX moved to 11,900 with bulls eyeing the 200-day moving average at 12,100.

US stocks climbed by around a third of one per cent despite the civil unrest dragging on and drawing some attention. The S&P 500 finished at 3,055, above its 200-day moving average and making a high at 3,062 in the process, just short of last week’s peak at 3,068. The Dow is trading around the 25,500 level with the 200-day SMA in sight at 26,360.

It’s a very light day for data but overnight the RBA left rates on hold at 0.25% and signalled a more optimistic view of growth. ‘It is possible that the depth of the downturn will be less than earlier expected,’ Governor Philip Lowe said. AUDUSD is stronger, moving back to 0.68 and its best level since January. News this week will be crucial – US services ISM on Wednesday and the nonfarm payrolls on Friday – for getting more of a handle on how much damage has been done and how quickly businesses are recovering.

Crude oil continues to hold the break on hopes that OPEC+ will agree to further extending the deepest production cuts. OPEC is set to meet June 4th now, with market participants expecting the cartel and Russia to rollover the May-Jun level of cuts for another 1-3 months. Having brought the meeting forward it looks like OPEC+ will extend the most aggressive cuts of 9.7m bpd through to the end of the summer, though an extension for the rest of 2020 looks off the table. As noted yesterday, with compliance at just 75% last month, all else being equal, OPEC will need more time to rebalance the market as it wishes.

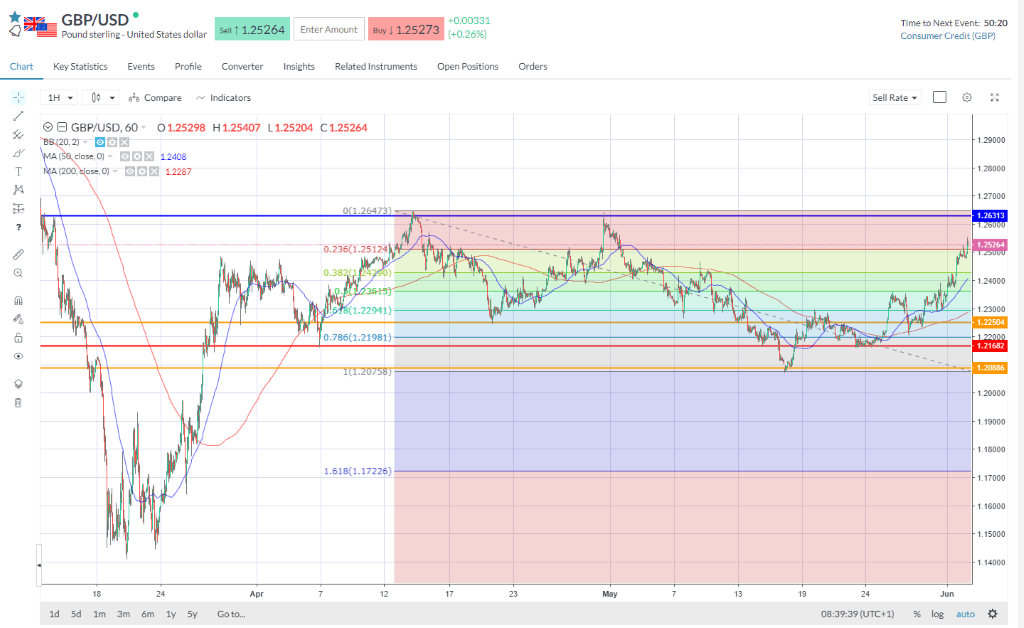

In FX, sterling has made a nice move higher, with GBPUSD breaking north above $1.25, after there was talk of a Brexit compromise ahead of the next round of talks this week. According to reports, the UK is making the first move to compromise – let's see if the EU can be flexible enough to get a deal done. GBPUSD pushed through the 23.6% retracement around 1.251, potentially opening up a move back to the Apr double top above 1.26. Removing a no-deal risk at this time would be a significant boost to the pound right now and may well take cable back above 1.30.

Author

Neil Wilson

Markets.com

Neil is the chief market analyst for Markets.com, covering a broad range of topics across FX, equities and commodities. He joined in 2018 after two years working as senior market analyst for ETX Capital.