Sticky inflation and rising Jobless Claims push the Fed towards tough decisions, and how S&P 500 reacts

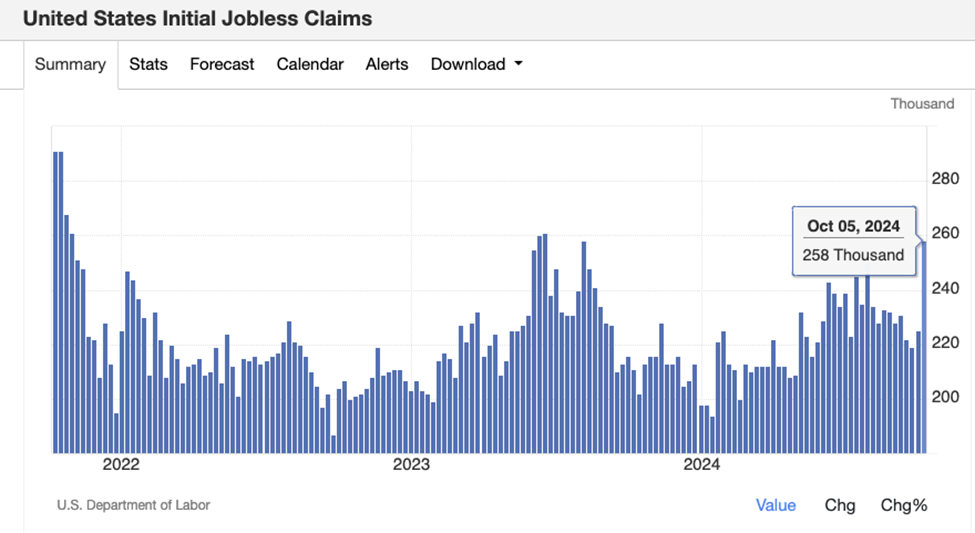

Last week, the US Consumer Price Index (CPI) rose by 0.2%, bringing annual inflation to 2.4%, both 0.1 percentage points higher than expected. Initial unemployment claims also unexpectedly increased to 258,000, the highest since August, attributed to Hurricane Helene and the Boeing strike. Now Boeing announced 17,000 job cuts, or 10% of its workforce, moving temporary job loss to prolonged ones. (Source: Reuters) As hurricane-affected businesses may take months to recover, monitoring unemployment claims is crucial as they serve as a leading indicator of future unemployment rates. If claims continue rising, the unemployment rate could increase in the coming months, potentially putting pressure on the Federal Reserve to cut interest rates. Chairman Powell indicated the Fed may prioritise unemployment over inflation, based on recent reports.

Source: Tradingeconomics

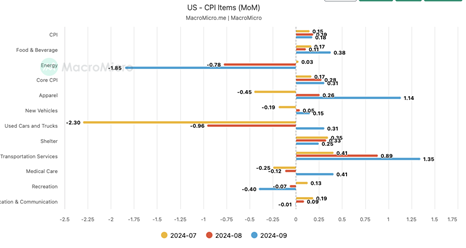

To conduct an effective analysis of the Consumer Price Index (CPI), it's essential to consider the weight assigned to its various components. One significant factor is the medical care category, which accounts for 8% of the overall CPI calculation. Recently, this category has shifted from being a negative contributor to a positive one, highlighting its growing impact on inflation. (Source: CNBC)

Source: MacroMicro

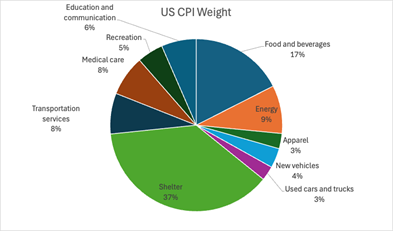

Souce: US Bureau of Labor Statistics

The medical care component of the CPI captures changes in both out-of-pocket expenses for consumers as well as payments made by insurers to healthcare providers and pharmacies. The index is structured to reflect the evolving cost structures faced by consumers, incorporating payments at the time of care and health insurance premiums into its calculation.

Transportation services have also driven inflation, with the consumer price index for airline tickets increasing by 25% over the past year, including an 18.6% spike in April alone.

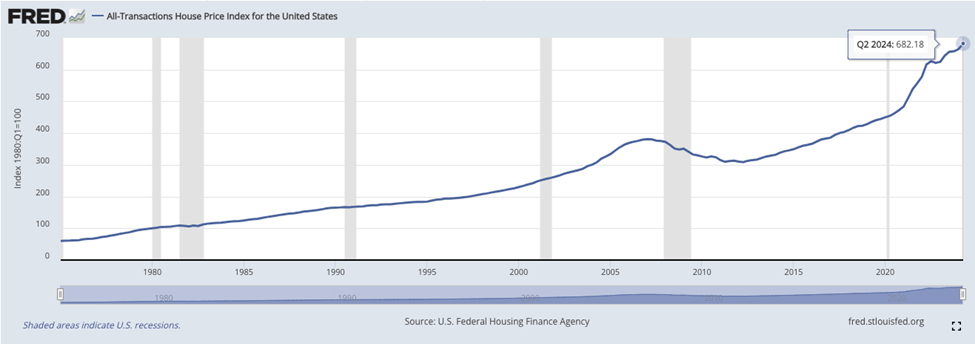

Shelter, which constitutes 37% of the CPI, remains the largest contributor. While 40% of U.S. households have mortgages, only 8% have adjustable rates, so rising interest rates have slowed new home construction and constrained supply, keeping home prices elevated and inflation becoming sticky.

Source: FRED

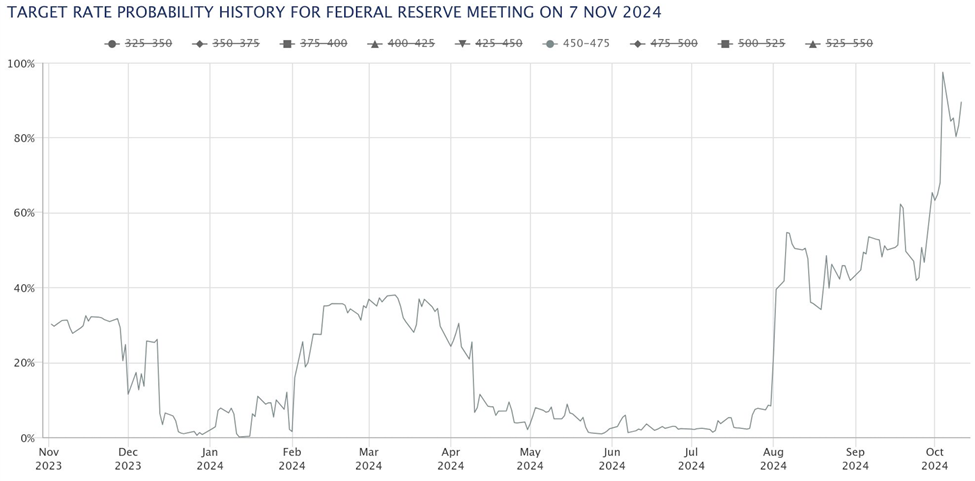

After the release of CPI and jobless data, market expectations shifted, with participants anticipating a possible 25-basis-point rate cut in November up to 94%. Broader factors, such as the US debt ceiling, Basel III implementation, and global economic slowdown, could pressure the Fed to continue cutting rates.

Source: CME group

Technical analysis

Source: Deriv X

The S&P 500 is in overbought territory, with resistance between 6018 and 6100. The next peak is expected between late October and early November, aligning with the US election, employment data, and the FOMC meeting.

Source: multpl

The chart shows the S&P 500 price-to-earnings ratio, which is historically high. Combined with a prolonged period of the manufacturing PMI below 50, it suggests the Federal Reserve will likely aim to manage market liquidity by cutting interest rates further.

Conclusion

As inflation stays elevated and unemployment claims climb, the Federal Reserve is likely to face increasing pressure to act more decisively, perhaps by cutting interest rates sooner rather than later.

Author

Prakash Bhudia

Deriv

Prakash Bhudia, HOD – Product & Growth at Deriv, provides strategic leadership across crucial trading functions, including operations, risk management, and main marketing channels.