Sterling Jumps As Brexit Debate Continues In Uk Parliament

The sterling jumped today as the debate on Theresa May’s Brexit proposal continued for the third day in the house of commons. The members are under pressure from large businesses who want to avoid a no-deal Brexit. Other members are also under pressure from their constituents not to pass the deal negotiated by May. Yesterday, two influential conservatives sent a strongly-worded letter warning of the deal. Sir Richard Dearlove and Lord Guthrie who served as the leaders of intelligence and defense respectively said that the deal will ‘threaten the national security of the country in fundamental ways.’ Therefore, there is a likelihood that the bill will be defeated on Tuesday when the members vote.

Meanwhile, economic data released today from the UK was mixed. In December, the country’s GDP expanded by 0.2%, which was higher than the consensus estimates of 0.1%. Construction output rose by 0.6%, which was higher than the estimated 0.2%. On an annual basis, the output increased by 3.0%, which was higher than the expected 2.5%. On the negative side, industrial production contracted by 1.5%, which was a bigger decline than the expected 0.7%. Manufacturing production for November also declined by minus 0.3%, which was lower than the expected 0.4% gain. In addition, the trade deficit widened by 12.02 billion pounds. This was higher than consensus estimates of 11.40 billion pounds.

In the United States, the inflation numbers for December met forecasts. The headline CPI rose by an annual rate of 1.9% while the core CPI rose by 2.2%. These numbers, which are closer to the Fed’s target of 2.0% means that the bank is likely to leave rates unchanged until the second or third quarter. This week, Fed chair, Jerome Powell maintained the earlier guidance that officials will be ready to adjust the forward guidance based on the data.

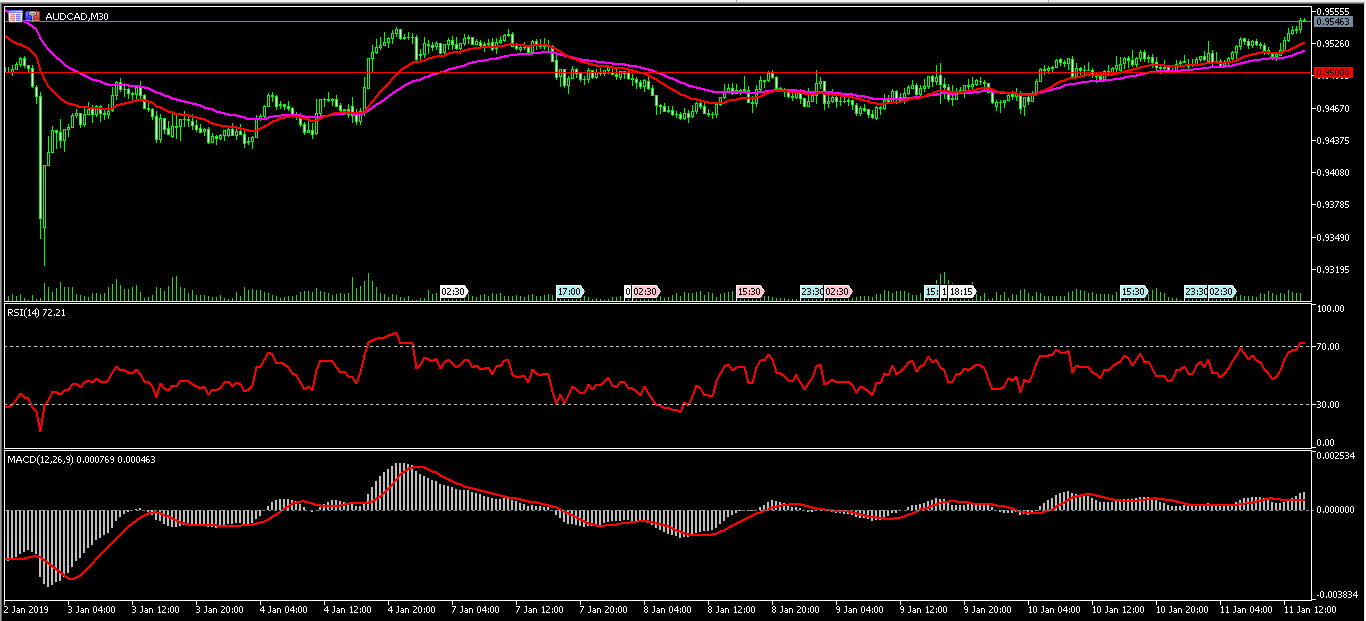

AUD/CAD

The AUD/CAD pair continued the upward trend and reached a high of 0.9545. This was the highest level this year. On the 30-minute chart below, the pair is above the 42-day and 21-day moving averages. The RSI has moved above the overbought level of 70 while the MACD remains slightly above the neutral line. The upward trend could continue. However, based on the volumes shown below, the pair could resume the downward trend. If it does, it will reach the important support of 0.9500.

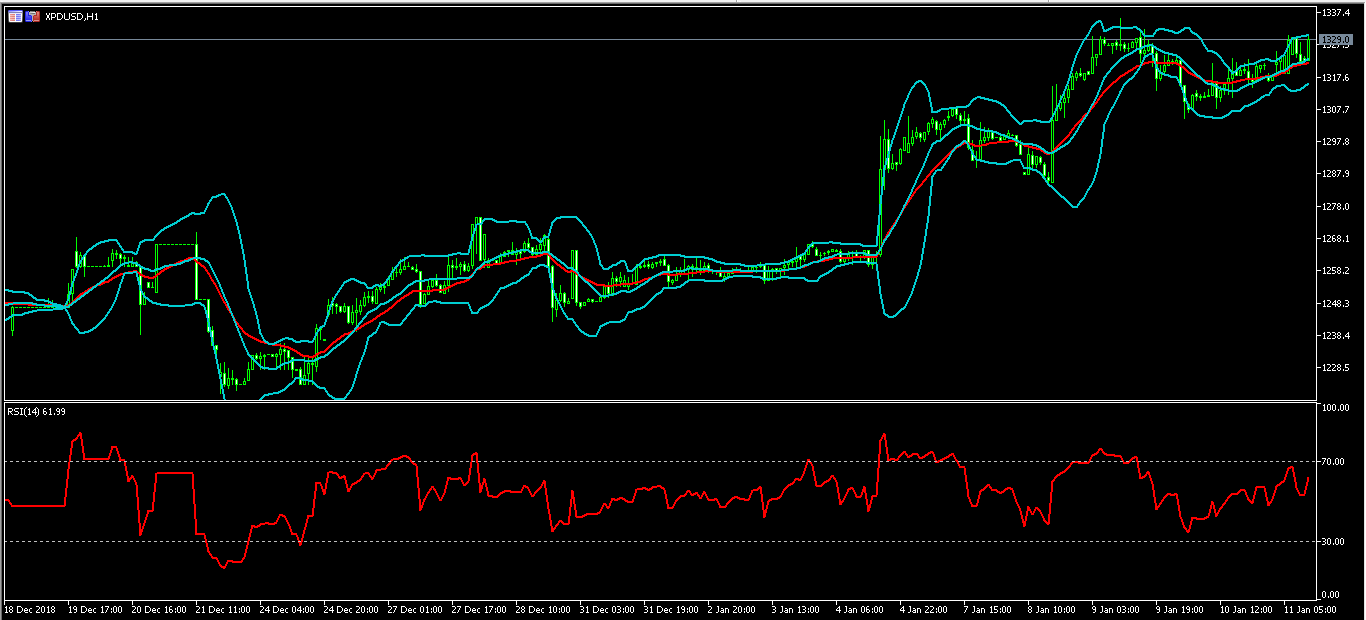

XPD/USD

In December, palladium became more expensive than gold, something that has not happened since 2002. Since then, the price of the metal has been going up and this week, it reached another record of $1344. The current prices are above all the short and long-term averages while the RSI on the hourly chart is not yet at the overbought level. The fundamentals of the metal are strong, which means that the price could continue to move up, even overshadowing the predictions from the technical indicators.

The EUR/USD pair rose today from an intraday low of 1.1485 and reached a high of 1.1540. On the hourly chart, the pair’s price is between the middle and upper band of the Bollinger Bands while the RSI remains below the overbought level. At the same time, the pair remains above the important 100 level. This means that the pair could maintain the upward momentum, and possibly test the important resistance level of 1.1600.

Author

OctaFx Analyst Team

OctaFX

OctaFX is a market-leading forex broker, providing personalised forex brokerage services to customers in over 100 countries worldwide.