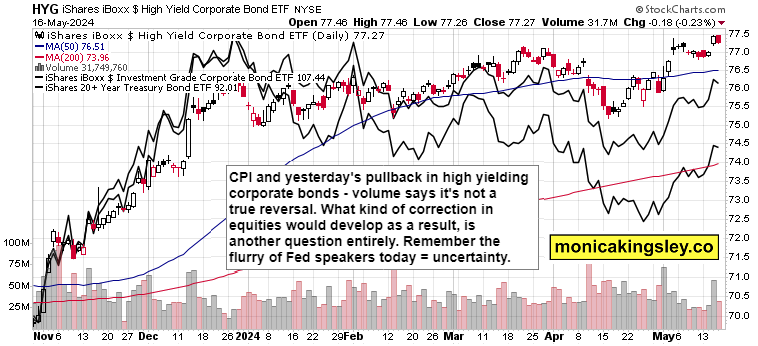

S&P 500 extended CPI advance, but was met with rejection

S&P 500 extended CPI advance, but was met with rejection – how serious is that? Too early to say whether that‘s the beginning of a protracted correction, but the procession of Fed speakers yesterday and today, must be taken into account.

Together with 10y and 2y yields together with the dollar defending 200-day moving average, this bond market chart reigns supreme.

Friday is data light, next week is again full of Fed speakers set to deliver intraday volatility, with services and manufacturing PMI data as the most important US ones apart from existing home sales.

Would these radically change rate cut perceptions of the moment, with Sep the baseline for first cut, with one more following (Jun odds are still clinging to 9%)?

That‘s the key point I‘m seeking to find the answer for clients in the below section (together with the protracted correction hypothesis), diving into sectoral S&P 500 insights as well.

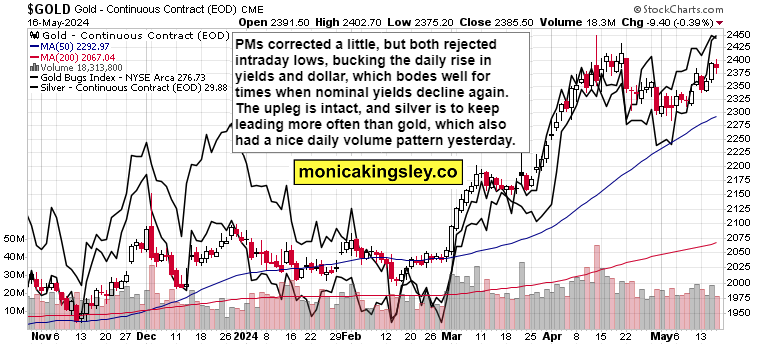

Gold, Silver and Miners

Gold and silver have merely paused while showing how well they are bid – silver $30 is within spitting distance, and odds are that even by today‘s close it would be overcome – and if not, there is early next week to take care of that. Alternatively, basing sideways would only give more power to the resulting upswing, and fresh push lower in yields is what would usher that similarly clearly to Wednesday, and in both precious metals.

Yes, I‘m still bullish since gold‘s failure to even reach the $2,275 support – same for silver.

Author

Monica Kingsley

Monicakingsley

Monica Kingsley is a trader and financial analyst serving countless investors and traders since Feb 2020.