Soybeans, cooking Oil and other threats to national security

After taking some time off over the Summer from spiking volatility to multi-year highs the President came out on Friday to issue a fresh salvo towards China, this time threatening to tariff certain Chinese made software parts 100%. The Chinese, naturally, responded in a mature and stately manor, with a CCP official emerging on Saturday to promise they would “fight to the death”.

Since then, President Trump has upped the ante further to explain in a Truth Social post: “China is purposefully not buying our soybeans… an economically hostile act”. He went on to explain that in response, the US would consider “terminating business” with regards to cooking oil and other elements of trade.

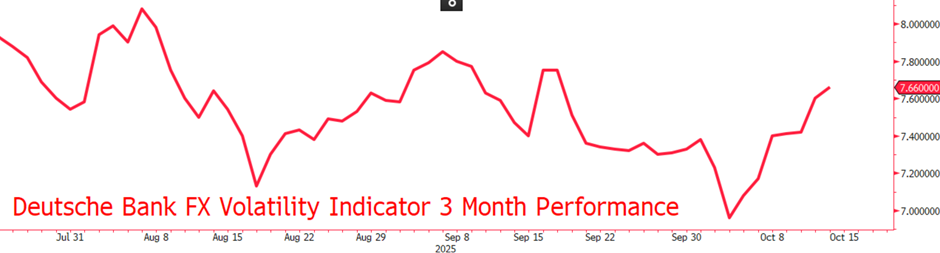

Despite traders’ insistence that they stay true to the TACO (Trump always chickens out) principle, some clearly broke ranks and contributed to the spike in FX volatility to its highest since mid-September.

Exactly what the President is thinking is eclectic as always (to put it nicely), with the US exporting nearly 11x the value of Soybeans to the Chinese than the Chinese sell Cooking Oil to the US ($1.2bln per annum of Chinese Cooking Oil imported to the US vs $12.8 bln per annum of US Soybeans exported to China a year).

But what does it mean for markets? Well, firstly, as touched upon, the upwards lurch in FX volatility and the accompanying drop in USD suggests that traders are not simply ignoring the President. In fact, a fair number still seem to be buying him and shorting USD whenever he makes a vague threat, “we’re considering” is a byword for “will sit on our hands” in Trump’s Whitehouse.

Much of this is part of the Great Rare Earths Game, that collection of minerals that when subjected to intense industrial processes are used to produce the chips that are not just key to the modern consumer in cars and computers, but even national defense with the latest military hardware being a key consideration within the Rare Earths Sphere.

However, the Dollar’s recent loss of strength still seems likely to be ephemeral, with Trump simply rattling his familiar old Sabre. USD’s outlook is refocusing more and more on the monetary side of the equation, with Powell’s speech last night regarding winding down the Fed’s Quantitative Tightening campaign over the next few months and his sharp focus on the labour market making traders more confident than ever of two more Fed cuts this year.

Gains against the Euro may become increasingly difficult as the French political crisis subsides and even the Yen is starting to show a fightback after being wrongfooted by the ascent of Sanae Takaichi close to the premiership. GBP is likely a softer candidate as concerns continue to mount regarding the Nov. 26th budget, concerns that are likely to reach fever pitch the week prior to the budget.

Author

David Stritch

Caxton

Working as an FX Analyst at London-based payments provider Caxton since 2022, David has deftly guided clients through the immediate post-Liz Truss volatility, the 2020 and 2024 US elections and innumerable other crises and events.